John and Sarah, a married couple in their early 40 who have two minor children, have been too busy to start estate planning. During a routine check-up, John discovers that he has a serious health condition that requires ongoing treatment.

This unexpected diagnosis has made them realise the importance of ensuring the smooth transfer of assets and safeguarding their loved one’s future.

How about you?

Estate planning is a crucial aspect of financial planning that often gets overlooked or delayed. However, creating a well-thought-out estate plan is vital to ensure the management and distribution of your assets and personal matters in the event you pass away or lose capacity.

In this article, we present an essential estate planning checklist that can be a valuable starting point for your estate planning journey.

Jump straight to…

What is the Estate Planning Process?

Alright, let’s break it down.

The estate planning process where choosing who will inherit your assets when you die may not be as exciting as planning a vacation, but without estate planning, you cannot choose who receives all you have worked so hard for.

Estate planning isn’t just for the rich. Even if you don’t have a pricey property, significant superannuation, or possessions to pass on, settling your affairs after you die could have a long-lasting (and costly) impact on your loved ones if you don’t have an estate plan in place.

The estate planning process involves careful consideration of various legal and financial aspects to ensure the smooth transition of assets and the realisation of your wishes. You can minimise potential conflicts, ensure peace of mind, and provide financial security for your loved ones by creating a comprehensive estate plan.

Key Elements in Estate Planning

Estate plans allow you to dictate what you want to happen to your possessions and business affairs after your death. Having a backup plan for who would handle your affairs in the event that you lose mental capacity and are unable to make medical and lifestyle decisions is also important.

Estate

When someone dies, their assets and liabilities are referred to as the estate or deceased estate.

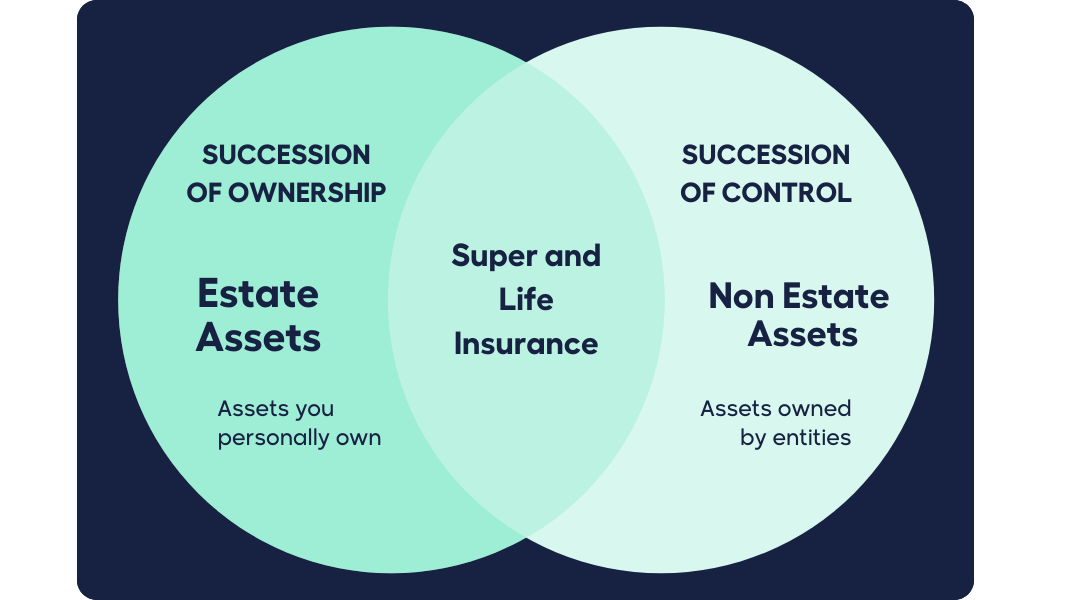

Estate Assets are valuable items you own. Real estate, cars, shares and other investments, superannuation, life insurance policies, and personal property (such as jewellery and furniture) can all be considered probate assets. Liabilities include mortgages, credit card debt, and personal loans. Typically, liabilities are paid out of estate assets before they are given to beneficiaries.

Note that not all your assets form part of your estate assets because usually, only personal assets form part of your Will. Assets that need not be included in your Will are called non-estate assets.

Non-estate assets or non-probate assets typically consist of:

- assets owned as joint tenants

- assets held in a discretionary family trust or private firm in which you have stock

- superannuation

- reversionary pensions or annuities, and

- some insurance policies where any proceeds are not paid to your executor or estate

Jointly owned assets, such as real estate or bank accounts, may not be part of your estate asset. Joint tenancy usually includes the right of survivorship, so the assets pass to the surviving joint owner immediately.

Since discretionary family trusts and private companies are separate legal entities with their own rules and regulations in distributing assets and business succession planning, their assets may not be part of your estate.

Superannuation, aka retirement savings accounts, are another important non-estate asset because they have their own distribution rules. Lodge a binding death benefit nomination with your superannuation fund to ensure your superannuation benefits are distributed as you intend.

Reversionary pensions or annuities usually pay a beneficiary after the original recipient dies and may not be considered part of your estate. To ensure they meet your estate planning goals, check the terms and conditions of these assets.

Certain insurance policies, like life insurance or income protection, may have direct distribution of proceeds to nominated beneficiaries, avoiding executor or estate payments.

Beneficiaries

A beneficiary is a person (or entity) named to receive the benefits of property that belongs to you. These benefits are frequently given to beneficiaries as a part of an inheritance.

Documents pertaining to a life insurance policy, retirement account, brokerage account, bank account, and other financial instruments may name a beneficiary.

Your financial assets should have beneficiaries designated so that they can be distributed in accordance with your preferences after your passing.

Goals and Intentions

The estate planning process requires you to be clear with your intentions whether identifying your intended beneficiaries, creating a tax-effective way to pass assets, safeguarding inheritance, protecting beneficiaries, and keeping yourself safe.

One of the main goals of estate planning is to take care of your loved ones. By clearly stating your intentions, you can ensure that your wealth is passed on to your intended beneficiaries rather than unintended ones.

Another important part of estate planning is minimising or avoiding death taxes. If you don’t plan ahead, your estate could have to pay a lot of taxes, which could hurt the financial security of your loved ones.

Additionally, estate planning is essential for safeguarding your beneficiaries’ inheritance from unforeseen events like divorce or bankruptcy. You may protect their inheritances from such events and ensure they are not jeopardised by including the proper legal structures and procedures in your estate plan.

Furthermore, estate planning enables you to protect your beneficiaries’ inheritances from their own weaknesses, such as addiction, gambling problems, mental health issues, or careless financial practices. You can safeguard your beneficiaries’ inheritances and give them stability, guidance, and support by forming trusts, setting constraints, or designating trustworthy stewards.

Last but not least, having an estate plan can keep you safe if your health deteriorates. With the proper legal document, you can choose a trustworthy individual or individuals to handle important health and financial decisions on your behalf.

People You Trust

Choosing the right person to carry out your wishes after you pass away or make lifestyle decisions on your behalf if you become incapacitated is crucial.

The executor and trustee will be your legal representative who will carry out your instructions after your death, thus they should be carefully chosen.

If you die, your children’s surviving parent normally becomes their legal guardian. In the event that both parents die, it is critical that both parents name the same people as guardians in their Wills.

Another big concern that commonly arises in estate planning for young families is who will look after the funds earmarked for minor children.

The person in charge of the children’s estate finances does not have to be the same as the guardian. In fact, separating these two duties reduces the likelihood of guardians misappropriating estate funds.

Lastly, in the event that you are incapacitated, you may need a person to manage your financial, legal, and/or personal affairs for a defined or ongoing period and to make health-related decisions.

Legal Documents

In order to put your intentions into action, you need legal documents to enforce your intentions.

You’ll need a Last Will & Testament outlining your final wishes about how your estate will be distributed after your death.

You may also need other legal documents, depending on other considerations, to authorise someone to make decisions on your behalf relating to legal, financial and personal matters in the event that you lose capacity to make decisions on your own.

Most Important Documents for an Estate Plan

Estate planning is considerably more than simply creating a Will. An estate plan can also include documents such as superannuation death benefit nominations (binding and non-binding), testamentary trusts (aka ‘Will Trusts’ or ‘Trusts Under Will’), life insurance, powers of attorney, power of guardianship (if applicable), and an advance care directive. All these would ensure that your wishes are followed.

A Valid Will

A Will is a legal document that specifies how your assets, such as your home, cash, and possessions, should be divided after your death. Your assets will be preserved and dispersed in accordance with your instructions if your Will is clear, legally valid, and updated.

A Will informs your loved ones of the beneficiaries you intended, which helps avoid complications when it comes to distributing your estate. Your beneficiaries and your lawyer would then know who you intended to be your executor, the person or institution in charge of administering your estate after you die. Furthermore, it will provide for the care of any minor children in your custody at the time of your death.

As your personal situation changes over your lifetime, such as the addition of children, grandchildren, or spouses, your Will must be amended to reflect your new wishes. Updating your Will is critical if you want to avoid confusion about how you want your estate distributed after your death. This can be especially important if you own a business, have been married more than once or have a blended family.

In each Australian state and territory, there are different government bodies that ensure your wishes are carried out by handling Will contests or managing your estate if you pass away without creating a Will. These state-based groups, generally called “Public Trustee,” may have slightly different legal powers and requirements. Find the state body that you need here:

- Australian Capital Territory

- New South Wales

- Victoria

- Queensland

- South Australia

- Western Australia

- Tasmania

- Northern Territory

You can either hire legal counsel or ask your Public Trustee for assistance in creating a Will. Either option can be pricey, ranging from a few hundred dollars for simple Wills to thousands of dollars for more complex estates.

Note that if you die without a Will, your estate will be distributed in accordance with state law. However, by establishing a trust fund, you can direct how your assets are transferred after your death.

Trusts

Several trust types are commonly used in estate planning. These trusts help you manage and distribute your estate according to your wishes. They can also help you save money on taxes and protect your assets.

Testamentary Trusts are a type of trust that is specified in your Will. It goes into effect upon your death, and it is administered by a trustee, whom you typically name in your Will.

The trustee takes care of your assets until they can be given to your beneficiaries. This is written in your Will and happens when a child turns a certain age or when a beneficiary meets a certain goal, like getting married or getting a certain qualification.

You might want to set up a trust for your beneficiaries if they are minors, have mental problems, or may not be able to manage their inheritance well.

A testamentary trust can either be a discretionary or fixed trust and can help keep family assets from being split up in a divorce or bankruptcy negotiations.

A Fixed Trust is one in which beneficiaries have set entitlements to the trust’s whole income and capital at all times throughout the income year. In other words, as specified in the trust deed, the trustee is required to make a distribution to the beneficiaries in a fixed or predetermined manner.

A Testamentary Discretionary Trust is often used by families where the trustee decides voluntarily to establish a trust for the benefit of another family member and for tax planning purposes. It functions very similarly to a discretionary family trust in many aspects.

A Family Discretionary Trust (also known as a discretionary trust or family trust) is an arrangement where one or more people (or a company) hold assets with the intention of transferring their benefit to other specified individuals on the terms outlined in the trust deed.

Family Trusts offer you a powerful tool for asset protection, tax efficiency, control over your assets, and effective estate planning.

Assets are protected since creditors of beneficiaries generally cannot access trust assets to settle beneficiaries’ debts.

Tax efficiency can be achieved when the trustee distributes trust income among beneficiaries by directing funds to individuals with lower marginal tax rates and allowing beneficiaries to be taxed on the income received from the trust.

A family discretionary trust can ensure your assets are managed by responsible family members who possess good financial management skills.

You can have some influence on the management of your trust after you die by making a memorandum of wishes where you indicate to future trustees of the trust what is to happen to the income and capital of the trust.

Powers of Attorney

Powers of attorney allow you to name a representative to act on your behalf if you are ill, disabled, or otherwise unable to do so. The enduring power of attorney and the medical power of attorney are the two forms of powers of attorney frequently used in estate planning in Australia.

Both types of powers of attorney must be made when the principal has the mental or legal capacity to comprehend the nature and implications of appointing an attorney or guardian.

An Enduring Power of Attorney (EPA) enables you to designate a person you want to handle financial and legal matters on your behalf. The attorney’s power may be invoked immediately or in response to a specific occurrence, such as when you lose mental capacity.

A general power of attorney, on the other hand, confines the attorney’s authority to a specific time and a certain range of issues. A general power of attorney becomes invalid if you become unable to make choices for yourself; thus it’s not advisable for estate planning.

A Medical Power of Attorney (MPA) empowers you to designate someone to make personal, lifestyle, and medical decisions on your behalf if you become incapacitated. This may involve choosing your living arrangements, healthcare, and other personal considerations. An EPG, like an EPA, may go into action immediately or become active after a specific event.

Be aware that powers of attorney in each state and territory may have slightly varying laws and requirements.

Guardianship Decisions

As a parent, naming a testamentary guardian for your minor children (under 18) may be the most important choice you make. Knowing who will take care of your children in the event of your death can help reduce uncertainty.

A testamentary guardian is an adult you name in your Will to make decisions about your child or children’s long-term care, welfare, and development until they are 18 years old. This includes decisions about their education, health, living situation, visits with family, participation in extracurricular activities, and religion.

If you don’t appoint a testamentary guardian in your Will, anyone with “sufficient interest” can apply for guardianship of your child. The Family Court of Australia will then decide who becomes the legal guardian based on the child’s best interests, not necessarily your choice. To ensure your child is cared for by the right person if something happens to you before they turn 18, it is important to appoint a testamentary guardian while you’re alive.

Advance Care Directive

An Advance Care Directive (ACD) is a legal document that allows individuals to make decisions regarding their medical treatment and future care. It is also known as an Advance Care Plan, a Living Will, or an Advance Health Directive. Individuals who are unable to communicate or make decisions might use ACDs to indicate their preferences and instructions for treatments and interventions.

Note that ACDs are governed by state and territory legislation, and compliance with each jurisdiction’s specific standards is crucial. ACDs are legally binding if they comply with the legal criteria and include explicit instructions to healthcare providers and family members.

Review and update your ACD on a regular basis, and discuss it with healthcare practitioners, family members, and substitute decision-makers to ensure that everyone is aware of your choices.

Life Insurance

The primary purpose of purchasing life insurance policies is to provide financial security for one’s surviving family members. This requirement could be more pressing in some situations than others.

The primary purpose of purchasing life insurance policies is to provide financial security for one’s surviving family members. This requirement could be more pressing in some situations than others. For instance, you probably don’t need life insurance if you’re a single, debt-free person without dependent family members or children. Many life insurance policies may not be available to applicants after a particular age.

Superannuation Death Benefit Nominations

In most cases, your super fund provider pays the remaining super fund balance to your nominated beneficiary when you die. Super paid out after a person’s death is referred to as super death benefit.

If your super provider’s rules allow it, you can nominate a beneficiary for your super either as a non-binding or binding death benefit nomination.

If you have the option of making a binding death benefit nomination, you can name one or more dependants or your legal personal representative to collect your super. For the purposes of deciding who receives a death benefit, you’re a dependant of the deceased if at the time of their death, you were their spouse or de facto spouse, a child of the deceased (any age), or a person in an interdependency relationship with the deceased.

If you made a non-binding death nomination, the trustee of the super provider may:

- use their discretion to pay according to the non-binding nomination; or

- make a payment to the deceased’s legal personal representative (executor of the deceased estate) for distribution in accordance with the deceased’s Will.

In the absence of a binding death nomination, the trustee of the super provider may:

- use their discretion to determine which dependant or dependants receive the death benefit;

- or make a payment to the deceased’s legal personal representative (executor of the deceased estate) for distribution in accordance with the instructions in the deceased’s Will.

Funeral Arrangements

When planning your estate, it’s important to outline your funeral wishes to relieve your loved ones of the burden during an emotional time.

On average, funeral costs can vary from $4,000 to $15,000 and include various expenses. To protect your family from these costs, there are several options to consider. You can save for your funeral by setting up a separate account or using prepaid funeral plans offered by funeral directors.

Funeral bonds are another option where you make regular payments that grow with interest and can only be used for your funeral. Funeral insurance is available but can be costly. Superannuation and government bereavement payments are potential sources of assistance, and Veterans Affairs pension holders may also qualify for support.

Your Estate Planning Checklist

An estate planning checklist is a comprehensive guide that helps you organise and plan how your assets and affairs are handled after you die or are unable to do so. It is a helpful tool to ensure your wishes are followed and to reduce complications for your loved ones.

Personal Assets

A comprehensive inventory of assets is essential in estate planning and involves listing both physical and non-physical assets. These lists are crucial for managing and distributing the estate after death, serving as references for executors or attorneys, ensuring accurate accounting, and fulfilling wishes effectively.

Physical assets are tangible items, including real estate, vehicles, jewellery, artwork, and furniture, and other possessions of value. It is important to be thorough and include all items of significant worth. Start by identifying items of value in each room of your home and consider assets stored in off-site locations like storage units or safety deposit boxes.

Non-physical assets are typically intangible items that hold significant value, such as bank accounts, retirement savings, investments, digital assets, life insurance policies, annuities, and trusts. Unlike physical assets, non-physical assets often require specific instructions to ensure their proper distribution.

Non-physical assets, particularly digital assets, are often overlooked during estate planning. By documenting these assets, you can protect your family from possible losses or problems. Also, think about leaving clear instructions on how to access and handle these assets, since passwords and security measures may be challenging for your beneficiaries.

Know Yours Debts

Creating a comprehensive list of debts is crucial in estate planning as it facilitates effective estate administration. A debt list should include the creditor’s name, contact information, outstanding balance, and account numbers. Regularly update the list to reflect financial obligations and ensure accuracy.

A debt list helps executors understand the deceased’s financial obligations, ensuring no liabilities are overlooked during the probate process. Documenting each debt allows for accurate assessment and development of a suitable resolution strategy.

Accurate asset distribution is crucial for determining the net value of an estate. By identifying and documenting the outstanding liabilities, the executor can determine the net value of the estate and distribute it under the deceased’s wishes, as outlined in their Will.

Furthermore, the list of debts aids in assessing the solvency of the estate. If the debts outweigh the assets, the estate may be deemed insolvent. In such cases, specific procedures are followed to address the debts and distribute the remaining assets accordingly.

A comprehensive list of debts enables the executor to prioritise repayment, as different debts may have different priorities. Secured debts, like mortgages, often take precedence over unsecured ones like credit card liabilities. This categorization ensures efficient estate asset utilisation and compliance with legal requirements.

A comprehensive debt list is essential for notifying creditors promptly after an individual’s death. It helps the executor identify relevant creditors and initiates the notification process, ensuring transparency and preventing delays in resolving outstanding debts.

Understand the Tax Implications

Understanding how taxes work can help you develop effective estate planning strategies that give your beneficiaries the most benefits. While tax regulations may evolve over time, here’s an overview of the potential tax implications associated with estate planning in Australia.

Capital Gains Tax

Australia has no inheritance tax, unlike other countries. Generally speaking, beneficiaries do not immediately pay tax on their inheritance. However, they may have tax responsibilities when they receive income or capital gains from inherited assets. For instance, a beneficiary may be required to pay Capital Gains Tax on any gains realised if they sell an inherited property.

The impact of Capital Gains Tax (CGT) is a significant factor in estate planning. CGT is a tax on profits from disposing of assets like property, shares, and crypto. CGT is part of income tax and not a separate tax.

Assets transferred or sold as part of an estate plan in Australia may be subject to Capital Gains Tax. Pre-CGT assets, or those acquired prior to September 20, 1985, are often exempt from CGT. Post-CGT assets are those acquired after this date and may be subject to CGT upon transfer or sale.

Tax on Super Death Benefit

Tax treatment of superannuation death benefits can vary. If you’re a beneficiary, the amount of tax you pay on a death benefit depends on:

- the tax-free and taxable components of the super

- whether you’re a dependent for tax purposes

- whether you take the benefit as an income stream or a lump sum

Note that superannuation benefits are not automatically included in a person’s estate. Instead, superannuation funds typically provide for a nominated beneficiary or beneficiaries.

Testamentary Trusts

Testamentary trusts offer flexibility and potential tax benefits, as they allow for income splitting among beneficiaries and potentially lower tax rates. Importantly, income from testamentary trusts for children is taxed at adult rates rather than the penalty rates (up to 66%) that are applied to other forms of trusts. This also means that children can benefit from the ‘tax free threshold’ and receive payments from the trust up to $18,200 without having to pay taxes on them.

List Your Memberships and Organisations

It is important to clarify if you are part of any organisation or have any memberships, as these organisations may have accidental life insurance that beneficiaries may be eligible to claim.

Additionally, creating a list of recurring payments for memberships and subscriptions can help your executor stop deducting funds from your bank account after your passing. Common recurring payments include gym memberships, newspaper and magazine subscriptions, donations to charities, phone and internet accounts, paid apps on mobile devices, sporting team memberships, and streaming service subscriptions.

This list can also be helpful for family members who want to donate to a charitable organisation they supported during their lifetime. If there is a record of a charity you regularly supported, they can reach out to that charity to make a legacy donation in your name or request attendees at your funeral to donate in your memory.

Choose Your Beneficiaries

Beneficiaries in Australia can be anyone you choose, as long as they are legally eligible. It’s important to clearly identify these beneficiaries and ensure that their wishes are validly documented and legally enforceable. It’s important to remember that the definition of financial dependent is stricter under superannuation and they must meet a set of pre-determined guidelines.

Immediate family members, such as a spouse, children, or grandchildren are often the primary recipients of your assets, and it’s crucial to specify how you want your assets distributed among them.

Extended family members, such as siblings, nieces, nephews, or cousins, can also be considered beneficiaries.

Charitable organisations can be included to support a particular cause or charity, providing tax benefits for the estate.

Close friends can also be included as beneficiaries if they have been an integral part of the individual’s life.

Business partners or employees can be considered beneficiaries if they have been instrumental in the success of the business.

Guardians for minors should be appointed to care for their children in the event of your passing. Establishing a trust to manage their financial affairs until they come of age is also crucial.

Contingent beneficiaries are individuals or organisations who will receive assets if primary beneficiaries predecease you or are unable to inherit. These beneficiaries ensure that your assets are not left unallocated or end up in unintended hands.

Appoint Your Executor, Enduring Power of Attorney and Enduring Guardian

Appointing an executor, enduring power of attorney (EPA), and enduring guardian requires adherence to specific legal procedures. It is crucial for managing financial, legal, and personal affairs for individuals with limited capacity or anticipated future incapacity.

Appointing Your Executor

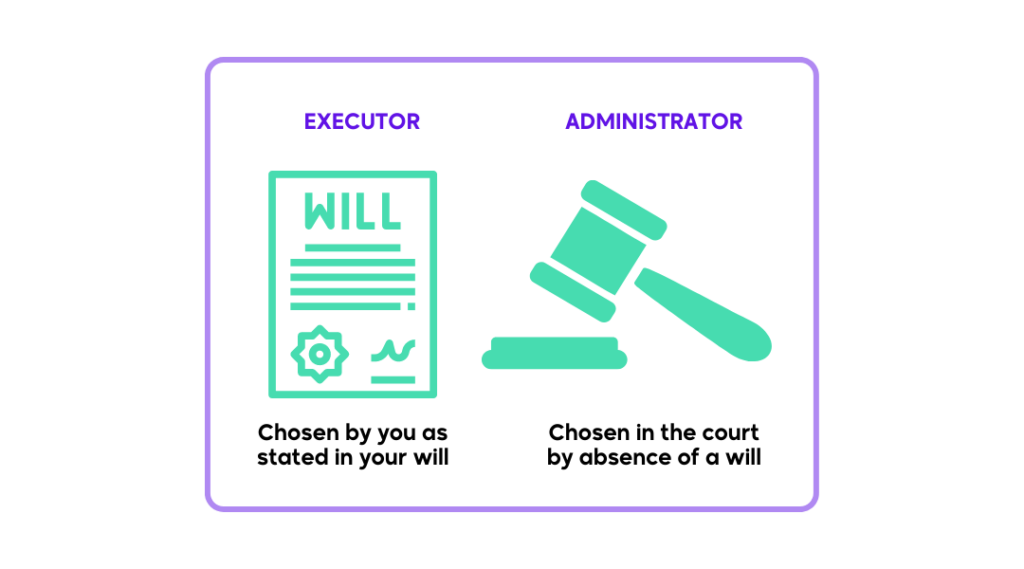

An Executor and an administrator are two distinct identities that play similar roles in estate planning. This involves the collection and distribution of assets, payment of debts and taxes, and ultimately distributing the remaining assets to the legal beneficiaries.

The primary distinction between an executor and an administrator is that an executor is chosen by the decedent in their Will, whereas an administrator is chosen by the court in the absence of a valid Will. The powers and duties of the executor are drawn from the Will, whereas the powers and duties of the administrator are derived from the court’s appointment.

An executor can be a family member, friend, lawyer, or a trustee company. Professional qualifications are not required, but complexities in a deceased estate may require assistance. If you don’t have a close relative or friend to choose from, or if you’re concerned about family disputes after reading your Will, choosing a professional executor can be advantageous.

Appointing Your Enduring Power of Attorney

An Enduring Power of Attorney (EPA) grants authority to an appointed attorney to act on your behalf in financial and legal matters, ensuring continuity and protection of your interests.

When choosing your attorney, consider the powers and scope you want to give your attorney over financial and property-related responsibilities during your incapacitation. Choose someone reliable and trustworthy to function as your attorney.

Seek advice from a qualified solicitor for estate planning and power of attorney matters. They Will provide personalised guidance and ensure compliance with local laws. Collaborate with the solicitor to draft an EPA document specifying wishes and powers, and outline the circumstances for EPA implementation, typically in cases of mental incapacity.

Once created, sign the EPA document with a qualified witness attesting to your signature and mental capacity. Check your state or territory’s registration requirements to ensure validity and acceptance by following necessary procedures. Inform family, friends, and financial institutions about your enduring power of attorney, ensuring they are aware of the appointed attorney and can support the decision if necessary.

Appointing Your Enduring Guardian

An Enduring Guardian ensures that your wishes and best interests are upheld when you lose decision-making capacity due to illness, injury, or other circumstances.

When choosing your enduring guardian, familiarise yourself with enduring guardianship legislation in your state or territory.

Have an eligibility criteria for choosing your guardian, such as being at least 18 years old, having decision-making capacity, and not being bankrupt. Once you’ve identified your guardian, discuss your values, preferences, and any specific instructions you want your enduring guardian to follow while making choices for you.

Create an enduring guardianship appointment using required forms or templates from the guardianship tribunal or government websites. Fill out the form accurately, ensuring it is signed and witnessed according to local requirements.

Be sure to provide personal details, enduring guardian information, and desired powers or limitations. Verify local requirements and complete the registration process accordingly and register the appointment with a specific authority or tribunal if necessary.

Write Your Will

Writing a legally binding Will is best left to experts like Wills and estate lawyers. Crafting a legally binding Will requires considering several factors, including legal considerations and legal requirements. Here are some tips to help.

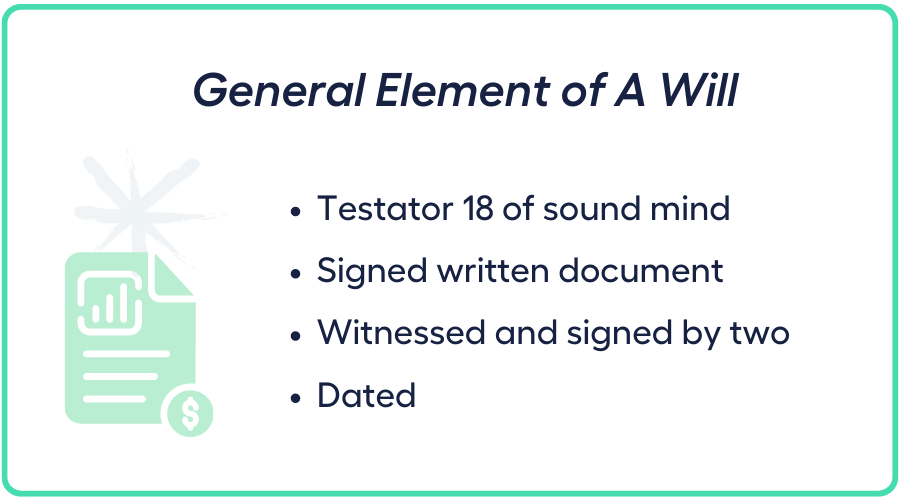

Ensure that the details are accurate and up-to-date. To make a Will a legal document, you must be 18 years or older. In limited cases, a person younger than 18 can make a Will, but this requires expert legal advice. Ensure your full name, current address, and identification details are accurate and up-to-date.

Express your mental state clearly. Make sure you indicate that you are of “sound mind” and cancelling all previous Wills that you may have executed. This is crucial if the Will is challenged. Know which version is current and legally binding if there are multiple versions.

Assign your executor and beneficiaries. When drafting a Will, keep in mind that you’ll need to name an executor and beneficiaries. It is crucial that you keep your Will and the beneficiaries of your estate updated when your relationships and circumstances change.

Have it signed properly by witnesses. Ensure that each page has a date and your signature, and that there are at least two witnesses ready to sign the document.

It is crucial to have your Will checked by a solicitor or Public Trustee to avoid invalidating your wishes and potentially having your estate go to tribunal. While writing your own Will may seem cost-effective, it is advisable to have it written with experienced lawyers to avoid disputes and ensure your wishes are carried out.

Make Copies of Your Estate Plan and Documents

Multiple copies of your estate plan and enable key individuals, such as executors, beneficiaries, and trusted advisors, to easily access the information. These copies provide a backup in case of loss, damage, or destruction. They also serve useful during your lifetime, allowing you to review and compare previous versions.

Additionally, having copies of your estate plan, including Wills, trusts, and powers of attorney, expedites the probate process, ensuring a smoother transfer of assets and implementation of your wishes. Regularly comparing your estate planning documents helps identify inconsistencies, outdated information, or necessary updates that may need to be addressed.

Store copies in a secure location, such as a fireproof safe or locked filing cabinet, or digitally on password-protected devices or secure cloud storage platforms. And ensure executors, beneficiaries, and trusted advisors are informed of the copies’ location and access details.

Expert advice is crucial for estate planning in Australia, as professionals provide specialised knowledge, tailor-made plans, and legal complexities to safeguard assets and ensure loved ones’ well-being.

Don’t leave the future to chance—consult with an estate planning lawyer or financial adviser today to secure your legacy.

Speak with a Money Guru Today to Discuss Your Estate Planning Needs

When you book a call with My Money Sorted, you’ll:

✓ get a better understanding of your financial options

✓ have an idea of the experts you can call on to help you reach your goals

✓ be matched with the right financial planner who can help simplify your family’s journey to financial wellness