Wouldn’t it be awesome if homeownership were more affordable so you could allocate more funds for retirement, investing, or paying off other debts?

It isn’t impossible to get a lower interest rate on mortgage repayments.

Jump straight to…

- What You’ll Need:

- Follow The Steps

- 1. Do Your Research

- 2. Make Sure You’re a High-Value Borrower

- 3. Prepare Your Approach

- FAQs from our MMS Community Members

- Talk to our team today to understand your best loan options for less stress, and more money success! Book a FREE 15 min Call or Send Us Your Questions!

Scripts to Negotiate Lower Interest Rates With Your Lender

A lower home loan interest rate equates to lower monthly home loan repayments, which will be easier on your budget. In addition, you can save money in interest throughout the course of the loan.

To do this, you’ll have to ask for a home loan rate decrease with your current bank or another lender.

In this article, we’ll discuss how to negotiate a lower interest rate, what to do if your lender won’t budge, as well as provide some scripts to help you negotiate a lower interest rate on your mortgage.

What You’ll Need:

You may be in a position to bargain for a lower mortgage rate or ask for fee waivers if you have a solid credit history, consistent income, a favourable LVR, and are able to manage debt.

- Gather information about your current mortgage, such as the interest rate, loan term, outstanding balance, and any additional fees or charges associated with the loan.

- Get your credit score from Experian, illion, or Equifax

- Calculate your Loan-to-Value Ratio (LVR), which is the loan amount as a percentage of the property’s value.

- Demonstrate financial stability by holding a steady job and having a consistent income history.

- Have genuine savings, typically accumulated over a minimum of three months.

- Have a low Debt-to-Income Ratio to comfortably manage mortgage repayments alongside existing debts.

Follow The Steps

Before diving into the negotiation process, it’s crucial to equip yourself with the right knowledge and strategies to increase your chances of success. Here are the essential steps to follow before engaging in negotiations.

- Step 1. Do Your Research. Knowledge is power, and in the realm of home loan negotiations, this phrase couldn’t be more accurate.

- Step 2. Make Sure You’re a High-Value Borrower. Lenders love borrowers who represent low risk and demonstrate their ability to repay their loans consistently.

- Step 3. Prepare Your Approach. The art of negotiation lies in preparation. In this final step, we’ll guide you through the process of formulating a well-crafted approach to discuss your desired lower home loan rate.

1. Do Your Research

Doing thorough research before negotiating a lower home loan rate is vital for understanding the market, assessing your own circumstances, identifying competitive offers, and building a strong case for your negotiation.

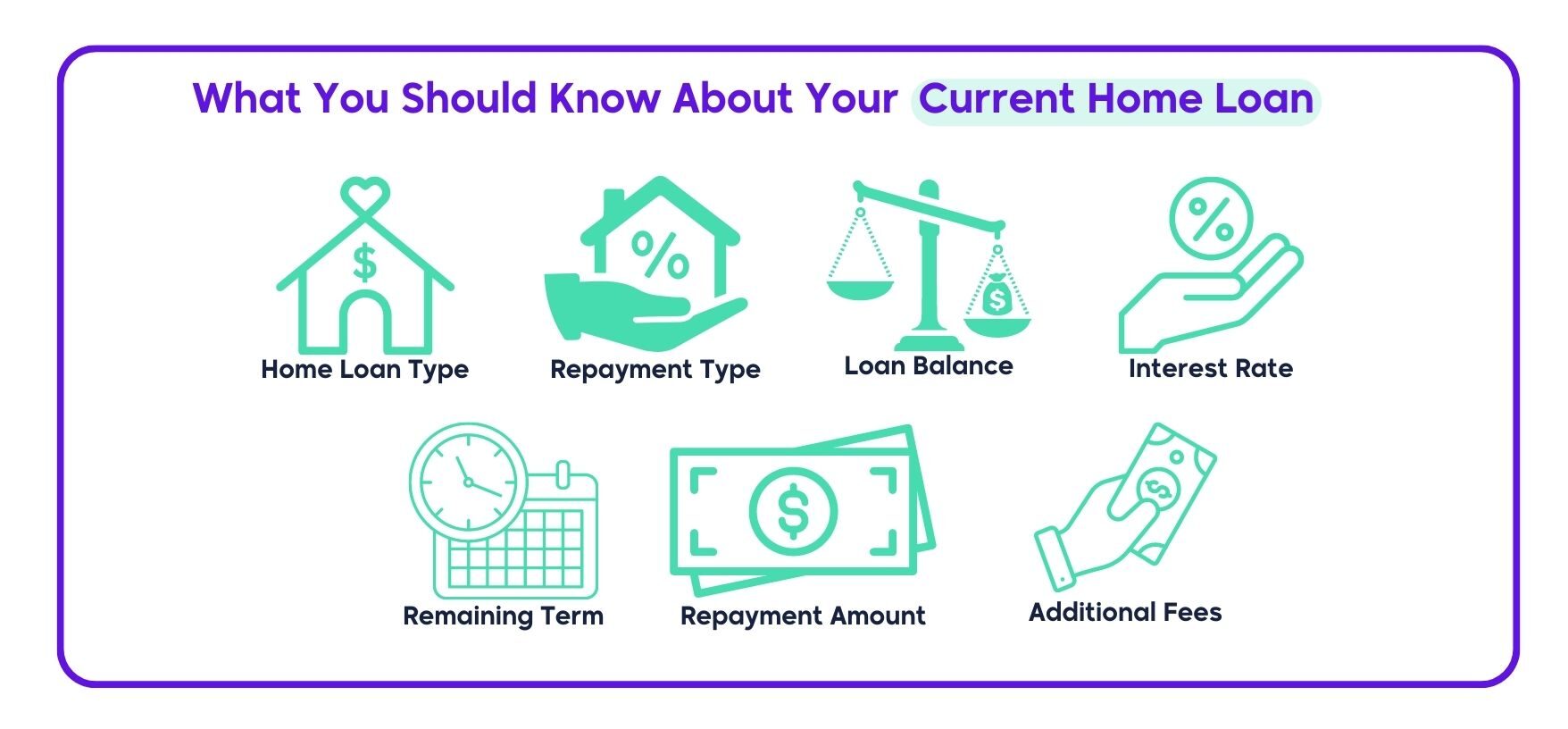

Your current loan details

To get specific information about your home loan, you should contact your loan provider directly or refer to the loan documents you received when you initially obtained the loan. Here are some key details you should be aware of:

Home Loan Type: Home loans are generally classified into two types: an owner-occupier loan and an investment loan. An owner-occupier home loan is taken by individuals who intend to live in the property they are purchasing. While an investment home loan is for individuals buying a property with the aim of generating rental income or capital growth, rather than living in it.

Repayment Type: Home loans are also classified based on the repayment structure, which are principal and interest and interest-only loans. A principal and interest loan is a repayment type in which the borrower pays both the principal (the original loan amount) and the interest on the outstanding debt. Whereas an interest-only loan is a repayment plan in which the borrower only pays the loan’s interest for a set period of time, often between one and five years.

Home Loan Amount: The Home Loan Amount is the initial loan balance borrowed from a lender to buy or refinance a property.

Outstanding Loan Balance: The outstanding loan balance is the remaining amount of the original home loan that still needs to be repaid to the lender.

Current Interest Rate and Type: Know the current interest rate that applies to your home loan. Also, identify if it has a fixed or variable interest rate. A fixed rate remains the same over a fixed rate period, while a variable rate may fluctuate based on market conditions.

Home Loan Term and Time Remaining: Home loan terms in Australia typically run from 25 to 30 years, but they can vary depending on personal preferences and financial circumstances. A home loan’s remaining term is determined by the loan’s origination date, the initial term, and the number of repayments made. To find out how much time is left on your home loan, contact your lender or check your loan documents.

Repayment Amount and Frequency: The repayment amount refers to the sum you regularly pay back to the lender. It is typically calculated based on the loan term, interest rate, and type of interest (fixed or variable). Repayment frequency refers to how often the borrower needs to make repayments on their mortgage whether monthly, weekly, or fortnightly.

Additional Fees: Check your home loan for any additional fees or charges, such as annual fees or early repayment fees.

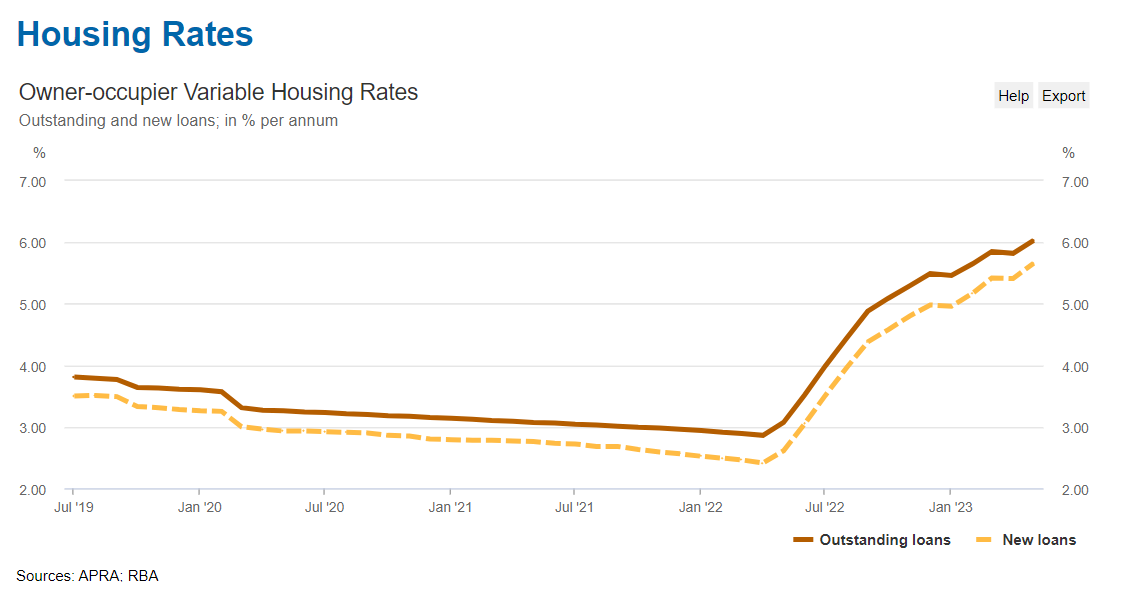

Your lender’s best interest rates currently: Before you ask your lender for a lower rate, it would be wise to find out what rates they’re offering to new borrowers. As reported by the Reserve Bank of Australia (RBA), home loan lenders typically reserve their most competitive rates for new customers to attract them.

If your current interest rate is already lower than the rate offered to new customers, it’s unlikely your lender will lower your rate. However, if you haven’t refinanced in a while and have been with your lender for some time, you may not have the most competitive rate.

This is especially true if you were on a fixed-rate home loan that reverted to your lender’s standard variable rate home loan at the end of your fixed term.

Knowing that as a loyal customer, you’re unlikely to receive lower interest rates, the initiative to negotiate must come from you. Having knowledge of your lender’s interest rates will make you feel more confident when negotiating.

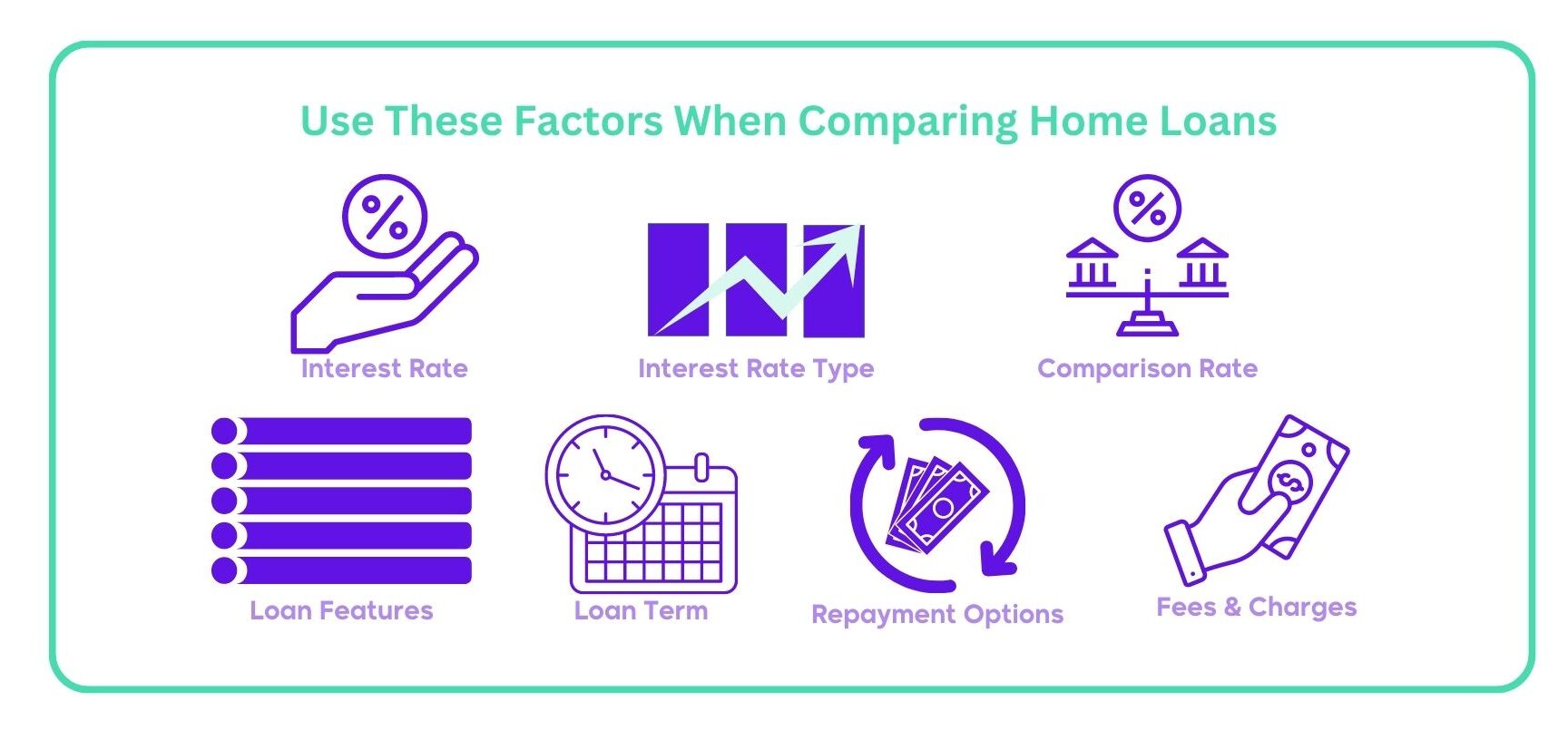

Comparison loan information and competitor rates

Before you speak with your lender, it’s a good idea to do some competitor research. Using websites that compare home loans, you can determine if a better rate is available out there.

Sometimes your lender can be reluctant to lower your rate to match new customer rates, which is why it’s worth seeking a competitive rate. You may find it easier to negotiate a lower interest rate if you can persuade your lender that you are paying more than if you switched lenders.

Just make sure you’re comparing the same factors such as interest rate, loan term, repayment options, loan features, fees and charges, and fixed rate or variable interest rate. Checking the comparison rate can assist you in determining the true cost of a loan while comparing loans and services offered by banks and mortgage providers. Do take note that comparison rates have limitations.

Home buyers can get advice from mortgage brokers to ensure that they’re not comparing apples and oranges. Especially when switching home loans with an offset account or checking which option has fewer fees.

2. Make Sure You’re a High-Value Borrower

Spend time carefully examining your financial situation before asking for a lower rate on your existing loan. You’ll be better equipped to present a compelling case to lenders, demonstrating that you’re an ideal borrower who deserves a lower interest rate.

A high-value customer has a low loan-to-value ratio (LVR), typically below 80%. To decrease the LVR, aim to save for a larger deposit, as this will reduce the loan amount and improve your overall financial position.

Demonstrate financial stability with steady employment. If possible, avoid making significant changes in your employment status during the mortgage application process.

Build genuine savings to show your ability to save and manage your finances responsibly.

Maintain a good credit score by paying your bills on time, managing your debts responsibly, and avoiding defaults or bankruptcy.

Improve your debt-to-income ratio by reducing your overall debt or increasing your income. It assures lenders that you can comfortably manage mortgage repayments alongside your existing debts.

Increase your home equity or the portion of a property’s value that you own outright. Having more equity in your home is advantageous, as it lowers the loan-to-value ratio.

![How is equity calculated]](https://mymoneysorted.com.au/wp-content/uploads/2023/07/2-e1690528098929.jpg)

3. Prepare Your Approach

As a savvy homeowner, you have a lot of leverage to secure a better home loan deal and can confidently negotiate for improved terms because:

- You’re an ideal borrower

- You know the pricing differences between loyal and new customers, and

- You are aware of competitive rates in the market

Be ready with specific examples of better deals on the market when you talk to your lender. Make a list of the individual services offered by rivals, highlighting the terms and features that most interest you. The fact that you are prepared with these examples will show that you have done the research and are sincerely looking for a better price.

Confidently communicate that you are not hesitant to explore other options during your discussion with your lender. Explain that while you value loyalty, you also want to get a better deal for yourself. By emphasising that you are open to considering several lenders, you send a message that competitors are actively vying for your business, which motivates them to present a compelling counteroffer.

Make sure your lender promptly sends the amended conditions in writing or via email if they agree to a better deal during the negotiation process. This written confirmation serves as a tangible record of the agreed-upon terms and safeguards against any misunderstandings later on.

Scripts for an Existing Borrower

Create a well-structured script that begins with a polite introduction, expresses appreciation for the lender, states your purpose of seeking a lower mortgage rate, and emphasises your commitment to a long-term relationship.

Also, practice your script and role-play the conversation with someone you trust to gain confidence and refine your delivery. Here are some sample scripts you can follow when creating your own.

Lower Rate Promotion for New Customers

In this scenario, you discover that new customers receive a lower interest rate than you. You contact the bank (or lender) to request a rate matching what new customers get.

You: Good morning. Thanks for talking with me. I’ve been a loyal customer of this lender for (x) years and paid my mortgage on time. However, I’ve noticed that similar loans given to new customers have lower interest rates.

Bank Representative: I understand your concern, but our current interest rates are based on various factors, including market conditions. As an existing customer, you secured your loan at a different time with the prevailing rates back then.

You: I understand that fully, but as a longtime customer, I was hoping to get a better rate.

BR: I understand how important this is to you, and we truly value your business. Let me check if there’s any room for adjustment on your current interest rate. Just give me a moment.

[The Bank Representative checks your loan details and reviews your payment history.]

BR: After reviewing your payment history and considering you’re a valued customer, I can offer you a reduced interest rate of 5.8%.

You: I appreciate the effort, but I’m afraid the rate isn’t competitive enough compared to the 5.7% rate offered to new consumers. I’ve seen similar rates offered by other lenders. I’ll need to refinance my mortgage. Can you give me a mortgage discharge form so that I can begin the process?

BR: Let me confer with my manager to see if we can make an exception for you. I’ll be right back.

[The Bank Representative leaves the room briefly to speak with their manager.]

BR: I spoke with my manager, and after much consideration, we can offer you the same interest rate as new customers. You’ll get an email soon confirming your revised rate, which will go into effect next week.

You: Thank you so much! I really appreciate your efforts in securing this rate for me. It means a lot to me to continue our relationship with this bank.

Better Rate at a Competing Lender

In this scenario, we assume you have the best deal from your current lender. But you find a more competitive interest rate with another lender for the same type of home loan. You’ll stay with your lender if they can give you a rate close to what competitors offer.

You: Thank you for taking the time to talk with me. I believe it’s time we discuss my mortgage rate.

BR: Of course. I understand your concern. Our standard rate of 6% for owner-occupier loans is competitive.

You: I appreciate that, but I’ve done some research. I found that other lenders offer lower rates for the same type of loan I have with you.

BR: I see. Well, we value your business. Let me check your account and see if there’s anything we can do.

[BR reviews your mortgage details and compares them with the offer from another bank.]

BR: You’re right. Although we don’t usually adjust rates mid-term, I can make an exception for a valued customer like you. However, lowering the rate to 5.7% would be a substantial reduction. We’ll need to reevaluate your financial situation and credit history.

You: Sure, I can do that. But I want to make it clear that if we can’t reach an agreement, I will consider moving my mortgage to another lender.

BR: I respect your decision. Our priority is to find a solution that works for us both. Let me process your updated documents, and I’ll see what we can offer.

[BR reviews your updated financial documents and runs the numbers.]

BR: After reviewing your information, I’m pleased to say we can offer you a revised interest rate of 5.85%.

You: That’s a step in the right direction. But considering other bank offers, can we get closer to 5.7%?

BR: I understand your request, but I’ll need to consult with my manager about this exceptional case. Give me a moment, and I’ll see what we can do.

[BR leaves briefly to speak with his manager.]

BR: I spoke with my manager, and we’ve decided to meet you halfway. We can offer you a new interest rate of 5.75%.

You: That’s much better. I appreciate your effort in making this happen. Thank you for understanding my perspective. I’m glad we were able to work this out together.

BR: You’re welcome. We value your loyalty and we’re pleased to have reached an agreement that satisfies us both. Let me get the documents for you to sign.

Script for New Borrower

In this scenario, you’re a new borrower trying to get a better deal than what the bank offers to new customers.

Bank Manager: Your credit score is good, but I’m afraid the current mortgage rate is non-negotiable.

You: I understand, but I’d like to discuss why I believe I could be a high-value borrower for your bank. I have a stable job with a consistent income. I’ve been saving diligently for years, and I have a significant down payment of 30% of the property’s value.

BM: That’s commendable, but the current rate is for everyone, regardless of their financial standing.

You: I understand, but I believe with my financial stability and responsible money management, I am a low-risk borrower. Offering me a more competitive rate would benefit both of us.

BM: I hear you, but it’s not a decision I can make alone. Let me see what I can do.

[The manager makes a phone call to the bank’s underwriter.]

Underwriter: You say you’re a low-risk borrower. Can you back that up with any additional financial information?

You: These are my latest bank statements, proof of additional investments, and my consistent payment history on previous loans.

Underwriter: Impressive. I can see you’re serious about this. Let me run some numbers.

[The underwriter leaves and returns.]

Underwriter: I’ve recalculated everything, and I can offer you a lower rate. It’s not as low as we’d give our VIP clients, but it’s better than the standard rate.

You: Thank you. That’s a step in the right direction.

BM: Indeed. We value responsible borrowers like yourself, and we’re pleased to reach a better deal.

FAQs from our MMS Community Members

We know mortgages can be confusing. That’s why we’re here to simplify things for you.

How much can you save by negotiating a better rate?

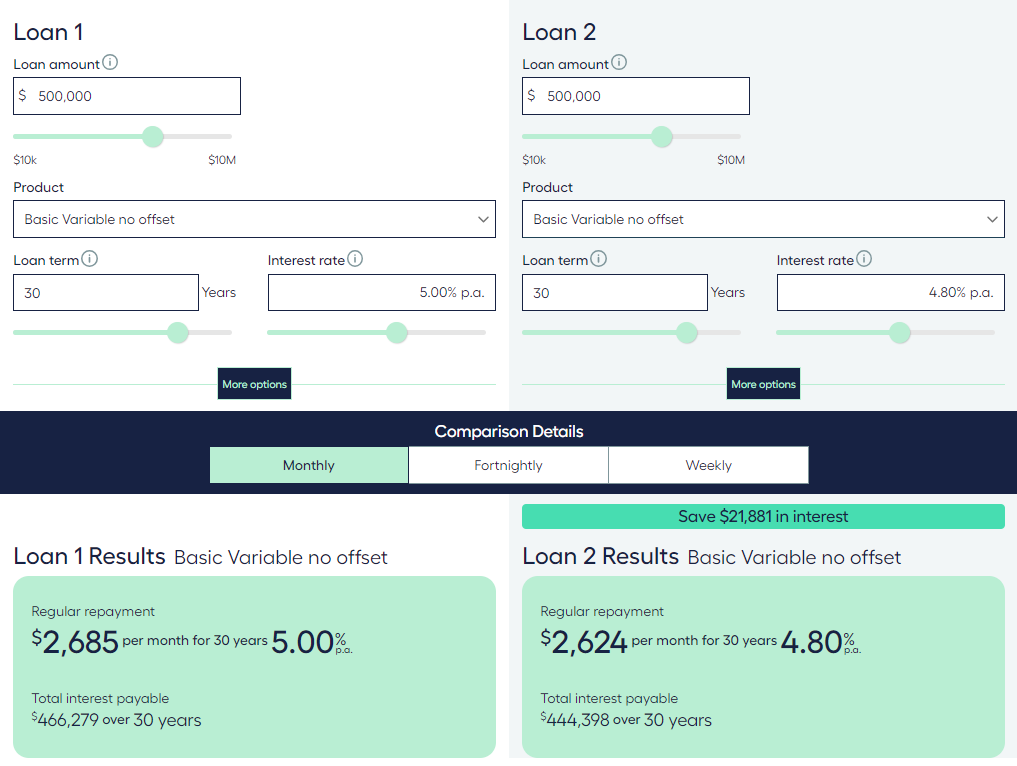

Negotiating a better deal can save you a lot of money over the duration of your home loan. Let’s have a hypothetical example to illustrate how even a small discount on a cheaper home loan helps you save on your repayments.

Let’s say you get a $500,000 loan with a 30-year term and a 5% mortgage interest rate. Using our loan comparison calculator, you have monthly repayments of $2,685. However, you find out that your lender is now providing a more enticing rate of 4.80%, so you negotiate and manage to secure a better rate.

Your monthly repayments drop to $2,624 as a result of the home loan interest rate reduction, resulting in a $61 monthly savings that total $732 in annual savings.

Does it hurt your credit to ask for a lower interest rate?

Asking for a lower home loan rate doesn’t hurt your credit score. However, making an excessive number of credit applications chasing a lower home loan rate can affect your credit score.

A credit enquiry is a record left on your credit report indicating that you have applied for a loan. Your report will reflect these enquiries for five years. If you shop around for credit and apply to many credit providers in a short period of time, your credit score will suffer.

Instead of making frequent enquiries, you can use home loan comparison tools to see how your interest rate and home loan compare to the market every 6 to 12 months.

How often can you ask for a lower interest rate?

Technically, you can ask as often as you like. However, it is wise to do your research every 3 months to check: if there are any great deals that you are missing out on, whether your property has increased in value, or if your lender has lifted interest rates higher than other lenders for comparable loans.

What are the 3 factors in getting a lower interest rate?

Aside from being a high-value borrower with a good credit score the Reserve Bank of Australia (RBA) identified these 3 factors in getting a competitive rate: loan type, loan size, and loan-to-valuation ratio.

Owner-occupier home loans with principal-and-interest payments are the most common type of loan in Australia. These loans entail regular principal-interest payments from the borrower and are seen by many, including credit rating companies, as a less risky type of loan.

On the other hand, an interest-only loan is viewed as more risky than a loan that also requires principal repayments. As a result, interest rates on principal-and-interest loans are often lower than those on interest-only loans. And if you’re a property investor, note that the interest rates paid on investment loans are typically higher than owner-occupied loans.

Larger loans receive more competitive rates. For instance, a borrower with a $1,000,000 loan approval would expect a 0.12% bigger discount than a $400,000. Larger loan applicants may have more leverage to lower interest rates. Given the fixed costs of writing loans, lenders may offer larger loans better interest rates.

The loan-to-valuation ratio (LVR) is a crucial factor indicating the risk associated with a loan. Higher LVRs are riskier due to less equity cushioning against property value declines. Borrowers with an LVR exceeding 80% usually need to purchase lenders’ mortgage insurance (LMI). The study found that loans with LVRs below 80% receive much lower interest rates.

Is 1% less interest worth refinancing?

Depending on your current loan rate and the size of your home loan, a 1% rate reduction could mean savings of up to tens of thousands of dollars for the remainder of your loan term.

Using the MMS loan comparison calculator we have this table below showing the difference in monthly repayments on a number of loan balances between a rate of 6.50% and 5.50%, which is around the current variable rate average.

| Amount | Monthly Repayments | ||

|---|---|---|---|

| 6.5% | 5.5% | Difference | |

| $400,000 | $2,399 | $2,148 | $251 |

| $500,000 | $2,998 | $2,685 | $313 |

| $600,000 | $3,598 | $3,221 | $377 |

| $700,000 | $4,197 | $3,758 | $439 |

| $800,000 | $4,797 | $4,295 | $502 |

Negotiating a better rate on your home loan is a financially savvy move that can save you substantial amounts over time.

Additionally, you can also seek advice from a mortgage broker to discover competitive rates from various lenders and receive multiple options. By consulting with a mortgage broker, you can gain insights to make an informed decision on your home loan journey.