Have you ever found yourself staring at your phone, knowing you need to make that phone call about something really important but daunted by the process that lies ahead?

Understandably, that first call, that first step can be nerve wracking for most people.

But with a little guidance, your first meeting with a financial advisor shouldn’t feel that way.

You are, after all, the customer, and customers should always be happy with the service they receive, especially from the financial services industry.

To help shed light on the unknown side of a financial meeting, we curated 10 questions to ask a financial advisor on your first meeting.

These 10 questions can become your very own cheat sheet and will help get all the information you need before making a decision and selecting an adviser to work with. Questions that could make that first meeting less daunting.

Jump straight to…

Preparing for a Financial Meeting with an Advisor

Financial advisors are to your financial health what doctors are to your physical and mental well-being.

How do you prepare for a doctor’s appointment?

Understand your condition, get ready for any questions the doctor could have, check that all of your test results and medical history records are in order, etc.

In the same way, even before you visit a financial planner, preparation is essential.

What Information Do You Need to Prepare?

Before you step out the door and meet financial advisors, prepare information about your financial situation so that you’re ready to receive holistic financial advice from the financial advisor you choose.

Some information a financial advisor needs from you are:

- personal information,

- assets,

- debts,

- income,

- expenses,

- insurance policies,

- and your lawyer (if you have one) and accountant.

Double check to make sure the information you give is updated and accurate.

1. Personal Situation

Financial advisors will need personal details like your

- age,

- place of employment,

- and marital status.

This information helps financial advisers identify what stage in life you’re currently in and how it can affect your financial timeline.

2. Assets

Your possessions that have value to you now or in the future are referred to as assets. Assets include your home, car, savings, superannuation fund, shares and other investments.

Your assets form part of your net worth, and knowing your assets helps you see which are easy to convert to cash (liquidity), which appreciates (increases) and depreciates (decreases) in value over time.

This helps you create a balanced asset allocation using the different asset classes.

3. Debts

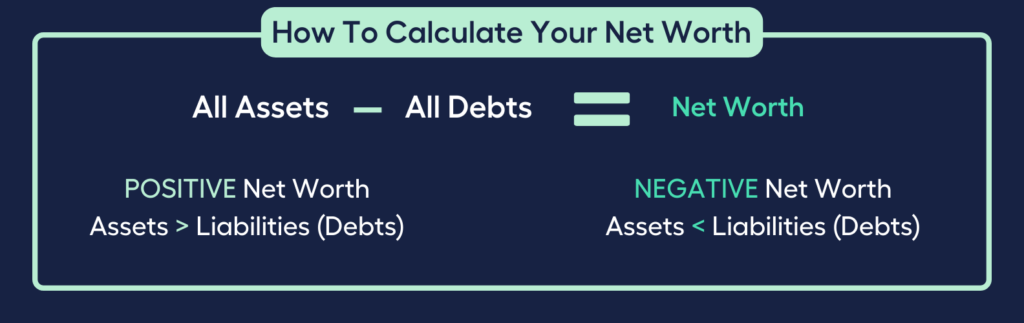

Your home loan on an owner-occupied residential home or investment property, personal loans, and credit card debt make up all your debts. Your debts form the other half of your net worth.

Your net worth is the difference between the value of your assets and debts (liabilities).

If your assets are greater than your liabilities, your net worth is positive. In contrast, you have a negative net worth if your liabilities exceed your assets.

Knowing your assets, debts, and net worth shows whether your financial standing is healthy or not, and will enable a financial advisor to devise a financial plan to reduce debt.

4. Income

To determine how much income you earn, make a list of all your income sources such as your

- annual salary,

- investment assets,

- and government benefits.

Understanding your income before taxes has the potential to have positive tax implications as a financial advisor will be able to work hand in hand with your accountant to explore tax saving opportunities.

5. Expenses

A list of your weekly and monthly expenses along with your income will help create a picture of your cash flow. This determines a suitable budget plan for you to create savings and increase your net worth.

6. Insurance Policies

Knowing the type of insurance you have and how much you’re insured for helps your financial planner understand how financially secure you and your family are should an accident or death occur.

7. Estate Plans

A proper estate plan can ensure that your desires are met, safeguard your family and close relationships, and minimise taxation on asset transfers.

8. Lawyer and Accountant

Having a personal lawyer and an accountant will make it easier for you to understand your financial options. A lawyer, accountant, and financial planner working for you makes a formidable team for your financial goals.

What Happens at the First Meeting with a Financial Advisor?

During your initial encounter, you and the financial advisor have the opportunity to lay the groundwork for your prospective partnership.

Painting your financial picture

Before giving any personal financial advice, financial advisors will conduct a “get to know you” session during your initial meeting. This will allow them to better understand your financial situation and personal circumstances.

Your needs, wants, and investment goals will be ascertained, as well as your risk tolerance.

- For example, are you interested in a particular advice such as advice related to your super fund or life insurance?

Or are you looking for a more comprehensive financial plan?

In any case, because several areas of your finances are frequently connected, most advisers will consider your entire financial picture and may ask about your assets and their values, information about any liabilities, and information about your income and expenses.

A two-way street

As a customer, you also need to know more about your financial planner and the company they represent before making a decision to take up their service.

Asking questions and getting details will help you arrive at informed decisions on whether your partnership with a financial planner will flourish or not.

What Questions Should I Ask a Financial Advisor?

Referrals from friends, googling, checking phone directories, and advertisements are normal ways to find a financial planner, but you may still need to shop around for someone who’s going to do the best job of looking out for number one — you.

To find someone who will prioritise your needs, has collaborated with others in similar financial circumstances as you, and is a fit with you personally rather than providing you with an “off-the-shelf” strategy, you may need to do some comparison shopping.

It is far better to shop around before seeking advice and to ask even the most uncomfortable questions at the outset. This is better than dealing with negative results later.

We prepared 10 questions you can ask financial planners to help you narrow down your choices and decide which one is most compatible with you.

Who do you usually advise?

When evaluating financial planners, it’s important to understand the types of clients they typically serve in order to ensure they have experience and expertise relevant to your situation.

Consider these questions to find out the typical clients the financial adviser services:

- How old are your clients?

- Are they investors or retirees?

- Are they receiving government assistance or are they self-funded?

- Are they employees or business owners?

If you’re just beginning to accumulate wealth, an advisor who primarily serves people in retirement age may not be the best match for you.

You may also want to look for financial advisors who focus on clients in specific professions. A small business owner or a medical doctor will want to work with an advisor who specialises in everything from insurance to taxes.

How long have you been giving financial advice to people in my position?

You also need to check the experience of the financial adviser who services clients in the same situation as you.

The more knowledgeable the adviser, the better. Your financial future after all is on the line.

If the answer is less than two years of experience, enquire whether anyone else in the company with more experience will double-check the advice.

What are your primary financial services?

Budgeting, cash flow management, a savings plan, superannuation, tax planning, home loan repayments, debt management and reduction, insurance, investments, and retirement planning (including items related to the government age pension) are all areas where a financial planner can assist you.

The scope of financial planning is so broad that financial advisors and planners need to specialise in order to serve their clients’ best interests.

Some tough questions you need to ask are:

- What is your area of specialty?

- How do you keep up to date with the financial planning products available, market movements, industry changes, etc.?

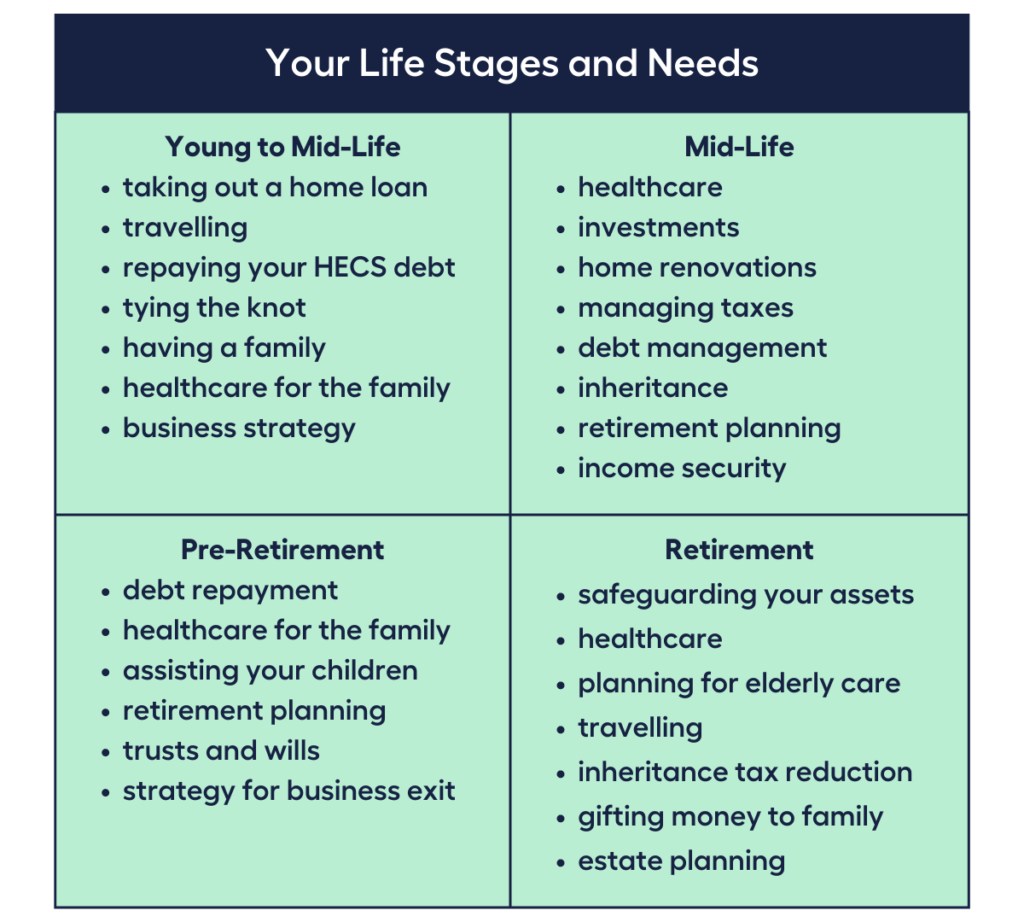

Meanwhile, you need to identify the stage of life you’re in by using the Financial Planning Association guide.

- Are you in the cohort of young to midlife Aussies who are establishing and building their careers and possibly starting a family?

- Are you a mid-life Aussie looking to achieve a comfortable lifestyle while also thinking about your long-term future?

- Are you nearing retirement? With 20 years or more of retirement ahead of you, your priorities will be determined by how well you’ve planned.

- Are you a retiree? This is the time to indulge in hobbies or travel, spend time with family, and plan for the transfer of your wealth.

No matter what life stage you’re in, there’s sure to be a financial planner out there who will match your financial needs.

Who owns your business?

A financial advisor is a self-employed or employed professional who acts in a fiduciary capacity. By law, a financial advisor needs to put the best interests of their clients before their own, regardless of the situation.

There are instances where some financial advisors may be constrained by their agreements with licensees and financial institutions, which dictate how their remuneration is structured.

Hence, it would be wise to ask:

- Are you incentivised by the licensees or financial institutions you work with?

- Are you self-licenced, or are you an Authorised Representative of a licensee?

Their reply, whether they’re independent or not, should make you feel comfortable to move on with the discussion.

A reputable financial advisor works on your behalf rather than serving the interests of a financial institution by maximising sales of specific products or capitalising on sales commissions.

How are financial advice or financial planning fees structured?

A financial advisor needs to give you a copy of their Financial Services Guide when you first meet with them.

The Financial Services Guide describes their rates, the services they provide, and the complaints process. This guide is a useful tool for comparing the costs of various advisors when considering which financial advisor to select.

Don’t be shy to ask direct questions if you need clarification. After all, a good relationship with a financial advisor hinges on transparency.

Ask:

- How do you price your services?

- How are “fees for services performed” determined?

- What will it cost for you to create a comprehensive financial plan for me?

Are there any conflicts of interest I should know about?

Hypothetically, the way in which financial advisers are paid can influence the advice they give you.

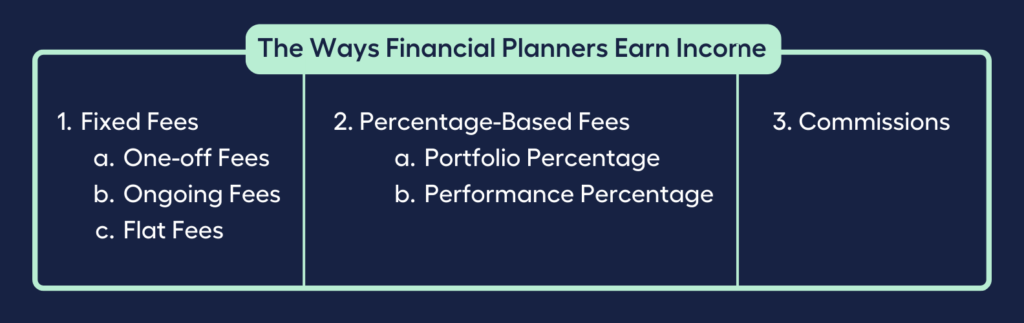

There are three typical ways financial planners earn income:

- fixed fees,

- percentage-based fees,

- and commissions.

1. Fixed fees can constitute one-off fees for specific services, ongoing fees for continuous services, and flat fees for administrative services.

2. Percentage-based fees can either be a percentage based on the size of your investment portfolio under management, or performance percentage based on investments under management.

3. Commissions are typically a percentage of the price of a financial product you purchase, such as insurance.

What is your investment philosophy?

Beware a financial advisor with no investment philosophy. This would not be unlike a ship without a rudder.

If your advisor lacks a convincing, evidence-based set of beliefs about markets and how to invest in them, you run the risk of working with someone whose investment strategy is based purely on hope and speculation.

Inconsistent investment strategies are a common cause of financial loss.

An investment philosophy is reflected in an advisor’s portfolio decisions. It’s critical that you not only understand and agree with their values and ideals, but that you can see evidence of a logical basis for making wealth and investment decisions.

If your advisor recommends an investment strategy that does not align with your values, it is not the right strategy for you.

Along with having the same values and investment philosophy as you, your financial planner must also understand your risk tolerance.

Ask:

- Is the risk of the particular investment or financial product you are recommending low, like bank term deposits?

- Or high, as in shares with a volatility factor or property development?

If the investment is in high-yielding fixed-income securities, you should ask these additional questions:

- How liquid is this investment?

- Who is borrowing the money, and for what purpose?

- If the money is being used for construction purposes, has the construction begun, or is it still in the planning and approval stages?

- How much of the development cost is covered by money from investors like me, and where do I stand in the creditor queue if the project fails?

The answers to these questions should also align with your investment values and risk tolerance.

Who provides your licence to operate?

There is value and security in knowing that you’re dealing with a certified financial adviser.

The Australian Securities and Investments Commission (ASIC) issues licences to financial planners and advisors. An Australian Financial Services (AFS) licence is required to conduct a financial services business.

An AFS licence allows licensees to administer registered schemes, deal in financial products, create markets for financial products, provide custodial or depository services, and perform the typical functions of trustee companies.

You could also ask your financial planner additional questions such as:

- Do you have an AFS License?

- Are you a member of a professional body?

- If so, is it the Financial Planning Association (FPA)?

The FPA has 12,000 members and has been working with financial advisors on their professional development since 1992. A certified financial advisor licensed by ASIC and who is also an FPA member gives an added boost of confidence in the quality of the organisation and the financial planning process you will go through.

You may also ask to see if the financial planners you meet are listed in the Financial Advisers Register. The Register is a list of financial advisors who are licensed to give clients personalised advice on sophisticated financial products.

Or you can do your own due diligence, visit the site and verify whether a financial advisor is qualified and licensed to give financial advice, and get information about the financial advisor before seeking financial assistance.

How do you communicate?

Communication is key in any relationship. It would be nice to have a financial planner who is able to meet with you, either digitally or in person, on a recurring basis.

Especially if changes in your personal life and financial affairs are forthcoming or when financial markets are uncertain and financial decisions need to be made.

Get a sense of their availability outside of scheduled meetings if you can. Find out how soon they usually respond to emails and phone calls.

Let’s Review

While there are many financial advisors available, selecting the best financial advisor for you can be difficult. It’s crucial to interview potential advisors in the same way you would interview a new employee for a job you have advertised.

Make sure you are aware of how they are paid and whether they are qualified, licensed and experienced to develop a strategy that is tailored to your unique financial demands and situation.

Or you can get your foot in the door and test what you learned by talking to My Money Sorted

Many people may be unaware of this…but just like you, 41% of Aussies intend to get financial advice rather than going it alone, according to an Australian Securities and Investments Commission (ASIC) report.

Find the right Financial Planner for you with the help of My Money Sorted.

When you book a call with My Money Sorted, you’ll:

✓ get a better understanding of your financial options

✓ have an idea of the experts you can call on to help you reach your goals

✓ be matched with the right financial advisor who can help simplify your family’s journey to financial wellness

My Money Sorted is your stress-free pathway to getting ahead with your money.

Here’s what your journey will look like:

Step 1: Start off with a quick financial assessment session with My Money Sorted

Step 2: Get matched with a licensed Finance Advisor that’s right for your money situation

Step 3: Take the first step towards your money goals with a clear and sound roadmap prepared by an experienced Financial Advisor.

It’s that easy!

Speak with My Money Sorted Today About Your Retirement Planning Needs and Get Your Money Sorted Today