When planning for retirement, the question most people ask is:

“How much do I need to retire?”

And with good reason.

Jump straight to…

One of the biggest lifestyle changes a person will experience in life is retirement.

And when it comes to reaching retirement age, the things that concern most people is running out of money and access to health care.

Although Medicare covers Australians after retirement, the following questions still keep some people awake at night:

Will Medicare be enough when I retire?

If it’s not enough, do I have to dip into my savings?

Will I end up selling my home just to cover my retirement?

Let’s try to allay those fears as we discuss:

- Where retirement income comes from

- What’s a good monthly retirement income

- How much retirement savings is needed to retire comfortably in Australia

- Retirement planning

Retirement Income

Retirement is a stage in life when a person decides to leave the workforce permanently. In Australia and most other developed countries, the traditional age of retirement is 65.

Today, the typical person can expect to live well into their 80s. This means if you retire at 65, you’ll require retirement income for at least 20 years.

Before we estimate how much regular income you’ll eventually need after leaving the workforce, let’s first look into the different sources of retirement income available to you.

Where does retirement income come from?

Government benefits and Superannuation are the two essential elements that make up Australia’s retirement system, but you can support your retirement lifestyle from a number of different sources.

| The 4 Sources of Retirement Income |

| 1. Government Benefits |

| 2. Superannuation |

| 3. Your Savings and Investments |

| 4. Your Home (if you consider downsizing) |

Source #1

Government Benefits

The Government Age Pension (GAP) is managed by Services Australia. It is a means-tested government payout that provides a basic income, and about three quarters of retirees qualify for it.

To be eligible for an Age Pension today, you must:

- be an Australian citizen

- be at least 67 years old

- pass both the assets and income tests

*Your expected pension income rate will be based on these tests.

There are two additional Australian government benefits that you may be eligible for if you reach the Age Pension eligibility age:

- the Commonwealth Seniors Health Card (CSHC), which entitles holders to affordable health care under Services Australia, and

- the Seniors and Pensioners Tax Offset (SAPTO), which lowers or in certain circumstances eliminates your tax due to the Australian Taxation Office (ATO)

Australian Defense Force retirees may also be able to access a Service Pension, which is managed by the Department of Veterans’ Affairs. The qualifying age for a service pension is 60 for both men and women.

Source #2

Superannuation

Superannuation is a mandated savings account that requires employer contributions of at least 10.5 per cent of an employee’s salary, and the employee chooses which superannuation funds to invest in until the employee retires.

Money doesn’t grow on trees, the same is true with your super funds. Your superannuation is your money and it’s up to you to ensure you maximise it’s growth over time.

Take care of your superannuation by:

- Selecting a fund with lower fees

- Comparing your fund’s performance with other funds

- Combining your super funds if you have multiple accounts

- Double checking your insurance before you change your super fund

- Understanding what’s involved before deciding on a self-managed super fund (SMSF)

- Knowing that withdrawing your superannuation early has risks

You can do any of these three options or a combination of these when you reach preservation age (between 55 and 60).

Preservation age is the earliest age at which you can access and withdraw your super, but you need not withdraw your super fund at this age if you wish to continue building on it until your age of retirement.

1. Account-based Pension

An account-based pension (or allocated pension) provides consistent, flexible, and tax-efficient income from your superannuation.

You can set up payments to be made monthly, quarterly, semi-annually, or annually.

What determines the life of your account-based pension?

- The amount of super that you transfer to your retirement account

- How much money you withdraw each year

- How much your super earns in investment returns

- How much you have to pay in fees

Your allocated pension lasts as long as your super balance, but it is not a lifetime income.

2. Annuity

Also known as a lifetime of fixed-term income, an annuity provides you a fixed income for a number of years, or the rest of your life.

When you purchase an annuity from a super fund or life insurance company, you choose the payment amount based on a specific number of years or your life expectancy.

Your annuity income can be increased by a fixed percentage or indexed to inflation each year to maintain its purchasing power. And you can be paid monthly, quarterly, half-yearly, or annually.

Although an annuity is less flexible than an account-based pension, you can be certain of your future income.

3. Lump Sum

When you retire, you may be able to take your superannuation as a lump sum payment.

You can withdraw your super account as a single payment or several payments depending on the rules of your fund. This is usually tax-free from the age of 60.

Source #3

Savings and Investments

Investment planning is an important part of managing your retirement income.

You will no longer have a steady income after retirement, so you must manage your money wisely and make long-term investment decisions.

The two main investment strategies are:

- Defensive

- Growth

Defensive Investing

This provides less room for growth, but it is a more stable and secure way to invest your money.

A term deposit is an example of a defensive asset because you earn a fixed interest rate while receiving your original deposit back at the end of the term.

Growth Investing

This aims for capital growth, which has a high potential for larger long-term investment returns. It may also require a high risk tolerance from you.

The goal of investment is to keep your money growing even after your retirement.

Source #4

Your Home

Consider downsizing your home as part of your retirement planning. It’s a sound way to put more money in your pocket and can even help you worry less about home loan repayments.

If you’re reading this because you’d like to avoid financial hardship when it’s time for you to retire, you might be thinking:

Will all these retirement income options give me $1 million dollars upon reaching retirement?

If you are already finding these details overwhelming, you can speak to a qualified financial planner who can give you personalised advice by considering your financial situation and financial goals.

Many people may be unaware of this…but just like you, 41% of Aussies have said they intend to get personal financial advice, according to an Australian Securities and Investments Commission (ASIC) report.

Find the right Finance Expert for you with the help of My Money Sorted.

Or you can keep on reading to learn more about…

How much should the average person have when they retire?

You may have heard that retiring requires having a million dollars. It’s the figure that’s frequently mentioned as the ideal financial retirement amount.

The reality is that most people entering retirement will not have anything close to a seven-figure sum.

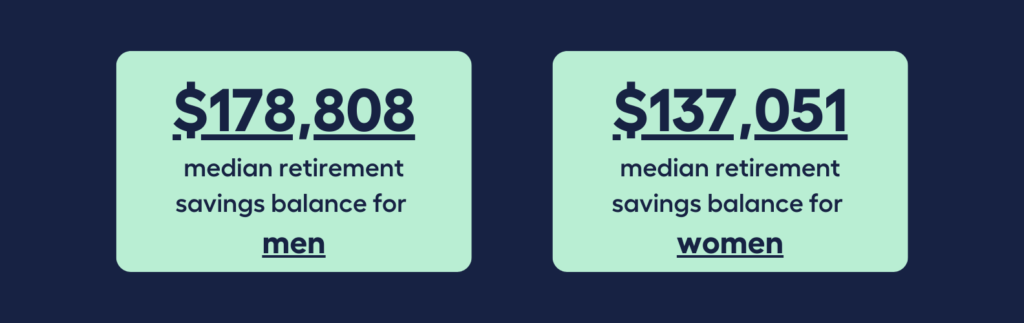

According to the Association of Superannuation Funds of Australia Limited (ASFA), men have a median retirement savings balance of $178,808 and women have a median balance of $137,051.

Having an amount in mind, even a million dollars, is a good way to start your retirement planning as part of an overall financial plan.

However, what is more important is that you have a good understanding of what a “comfortable retirement” means to you. Once you’ve determined that, you can estimate how much money you’ll need for your retirement income goals.

1. Lifestyle After Retirement

The type of lifestyle you want to lead after retirement is an important factor in determining how much money you need for retirement.

If you want to live with the same level of comfort as you did during your working life, you should calculate how much you need to cover those expenses – minus any work-related costs.

Or, if you plan to live more modestly after retirement, you may not require as much.

2. Daily Expenses

How much income you need after retirement will be determined largely by your lifestyle and daily expenses.

What to consider when calculating your daily expenses:

- How much do you spend on groceries and other necessities?

- How frequently do you eat at a restaurant or cafe?

- How many local, national, or international holidays do you take each year?

- Is your home in need of improvements or ongoing repairs?

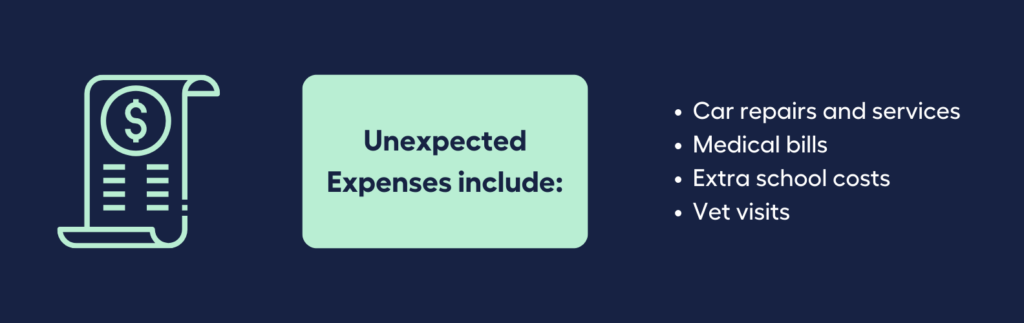

Aside from your regular expenses and the occasional splurge, you should also budget for unexpected costs.

If you are one of the 60 per cent of Australian homeowners who are still paying off their home loan, you must also budget for any outstanding debts like mortgage repayments.

3. Life Expectancy

Australians are living longer lives as a result of improved nutrition, public health, and medical advances.

Women over 65, for example, are expected to live to be 88 years old, while men over 65 are expected to live to be at least 85 years old.

Because of rising life expectancy, you may need to plan for a longer retirement or think about the option of transitioning into retirement.

4. Government Age Pension (GAP) Eligibility

The Government Age Pension is a “safety net” for people who meet certain age and residency requirements.

Approximately 62 per cent of Australians over the age of 65 receive a full or partial government pension.

The amount you receive is determined by a number of factors, such as:

- your assets

- the amount of super you have, and

- any other income you may receive in retirement, like rental returns from investment properties.

5. Transition to Retirement (TTR)

For some people, completely ceasing work once they reach the age of retirement can be a huge shock in terms of lifestyle, self-worth, and financial security.

Instead, you might want to consider retiring gradually.

This is where a transition to retirement (TTR) strategy comes into play. It allows you to access your super while continuing to work.

A TTR strategy may be an option if you are concerned about not having enough super savings for your ideal retirement.

What is a good monthly retirement income?

A good monthly income could mean a “comfortable” or “modest” retirement for different people, which is why having a standard to compare against can be useful.

For a good monthly retirement income, let’s compare the Association of Superannuation Funds of Australia (ASFA) Retirement Standard for a modest living against that of the Government Age Pension.

| ASFA Modest Income Standard vs the Government Age Pension Retirement Income | ||

|---|---|---|

| ASFA Modest Retirement(annual) | Age Pension Retirement (annual) | |

| Single household budget (aged 65 to 84) | $30,063 | $23,420 (maximum basic rate*) |

| Couple household budget (aged 65 to 84) | $43,250 | $35,308(maximum basic rate*) |

| What can it afford? | Occasional recreational activities | Inexpensive recreational activities |

| Limited takeaway orders, few home deliveries, and cheap restaurant dining | Cheap takeaway or special meals at local club | |

| Own a simple vehicle | Small budget for car ownership, maintenance, and repairs | |

| Plan ahead for minor house repairs | Having no money for home repairs | |

| One domestic holiday every year or a couple of brief getaways | Very brief vacations in your local area | |

| Basic insurance for private health care | Absence of private health insurance |

Remember:

For a good or modest lifestyle after retirement, defensive investment options that give fixed interest rates plus your original deposit at the end of term may be enough, especially if you have a low risk tolerance.

How much money do you need to retire comfortably in Australia?

To see how much more income you need for a comfortable retirement, let’s now compare the same ASFA Retirement Standard for a comfortable lifestyle against a modest living.

| ASFA Comfortable Income Standard vs ASFA Modest Income Standard | ||

| ASFA Comfortable Retirement(annual) | ASFA Modest Retirement(annual) | |

| Single household budget (aged 65 to 84) | $47,383 | $30,063 |

| Couple household budget (aged 65 to 84) | $66,725 | $43,250 |

| What can it afford? | Regular recreational pursuits | Occasional recreational activities |

| Occasional dining out, home delivery, and take-away coffee | Limited take-away orders, few home deliveries, and cheap restaurant dining | |

| Own a dependable vehicle | Own a simple vehicle | |

| Budget for home renovations | Plan ahead for minor house repairs | |

| Both domestic and sometimes international travel | One domestic holiday every year or a couple of brief getaways | |

| Private health insurance at a premium | Basic insurance for private health care |

Remember:

For a comfortable lifestyle after retirement, a growth investment with a high potential for larger long-term investment returns may be in order to secure your financial future.

Planning Your Retirement Income

Retirement planning may not be the most interesting aspect of financial planning, but it is unquestionably one of the most crucial.

When reaching the age of retirement seems like a distant dream at your current age, it’s easy to put off thinking about retirement, but as each year passes, it becomes more and more of a reality.

How do I begin to plan for my retirement?

If thinking about retirement planning makes you nervous or anxious, you don’t have to feel that way. You’re not alone, many feel the same way.

You can simplify the process by starting with these four items and preparing a retirement plan before you make investment decisions.

1. Retirement Age

Your retirement income strategy depends more on having a clear idea when to start your retirement than having a money goal.

Set a specific age when to start your retirement and the amount you’ll need will become clearer.

However, knowing when to start retirement is just half of the preparation.

2. Life Expectancy

Estimating how long you’ll live after retirement is a tougher part of the retirement planning process.

With a healthy lifestyle and better healthcare, more Australians are expected to live into their 80s if living conditions in this decade remain the same.

However, if living conditions improve, you may very well live into your 90s. When planning for retirement, overestimating is preferable to coming up short.

3. Retirement Goals

Identifying your retirement goals is a crucial part of retirement planning. Ask yourself the following questions as you start your retirement planning process:

What is my dream retirement?

What are the things I want to do after retirement?

How much will they cost me?

Can I afford to maintain them?

4. Personal Circumstances

Every person is unique, thus you require a unique and comprehensive retirement plan.

Are you single?

Are you a couple?

Are you living separately from your partner?

These three varying circumstances are treated differently by Services Australia.

Additionally, how you wish to withdraw your superannuation be it lump sum, annuity, or account-based pension has varying tax implications.

Creating a clearer retirement plan tailored to your needs is reliant on knowing your personal circumstances.

Earlier I mentioned that you don’t have to feel nervous or anxious with retirement planning because you’re not alone.

Many people may be unaware of this…but 51 per cent of Aussies have sought retirement planning advice, and like you, 38 per cent intend to get retirement planning advice soon, according to an Australian Securities and Investments Commission (ASIC) report.

What if you could tap into the wisdom of an experienced financial adviser instead of taking the all too common ‘hit-and-hope’ approach?

Many people may be unaware of this…but just like you, 41% of Aussies intend to get financial advice rather than going it alone, according to an Australian Securities and Investments Commission (ASIC) report.

Find the right Finance Expert for you with the help of My Money Sorted.

When you book a call with My Money Sorted, you’ll:

✓ get a better understanding of your money matters

✓ have an idea of your money goals to help you save more

✓ be matched with the right finance expert who can help simplify your family’s journey to financial wellness

My Money Sorted is your stress-free pathway to getting ahead with your money.

Here’s what your journey will look like:

Step 1: Start off with a quick money matters session with My Money Sorted

Step 2: Get matched with a Finance Expert that’s right for your money situation

Step 3: Take the first step towards your money goals with a clear and sound roadmap prepared by a Finance Expert

It’s that easy!

Get Your Money Sorted with a Finance Expert by booking a call with My Money Sorted today!