The goal of owning a home is one of the most important financial goals for many Australians, and a mortgage is essential to achieving this goal.

Homeownership through a mortgage is a strategic move for long-term financial stability, similar to managing a well-thought-out investment portfolio.

At My Money Sorted, we recognise that owning a home goes beyond mere property acquisition—it can be a smart investment for the future.

Mortgages and homeownership are closely related in financial planning. They are a cornerstone that reflects sound money management and forward-thinking strategies.

In this article, we’ll help you understand the challenges of owning a home or investment property. We’ll be touching on mortgages, interest rates, and property taxes to help you create a plan that meets your specific financial goals.

Jump straight to…

Overview: Definition of a Mortgage

A mortgage is a contract that is signed by a borrower and a lender – usually a bank or other financial institution – under which the borrower receives funding to buy a property.

The actual property is used as home loan collateral. The borrower agrees to make consistent home loan repayments to the lender over a predetermined period of time in order to repay the loan amount plus interest.

Types of Mortgages

There are three major types of mortgages available in Australia: fixed rate, variable rate, and split rate mortgages.

![Types of Mortgages Offered in Australia]](https://lh7-us.googleusercontent.com/zLtosHbuGBgceXpDHYguPQvczoCWiy8cZlQODPsqNZyhMDjwp-zmmcXAOQSdnmxxcarx9F6cXnqWrvq3Ebg1AP0RqZWAsstLjjPi30fIOZvKyQVORSDuobR1xic_PmW7pXqvJ6JQXG94Lms0WNqVKn8)

Fixed Rate Mortgage

A fixed rate mortgage is a type of loan in which the interest rate on home loan repayments remains the same for a set period of time, usually between 1-5 years. A fixed rate mortgage, is a popular choice for homeowners due to their predictable and stable interest rates.

However, fixed rate mortgages typically do not offer as much flexibility or features as variable rate home loans. Fixed rate mortgages may have higher exit and fees and charges, if borrowers decide to end the fixed period, reverting to the standard variable interest rates. Furthermore, a fixed rate mortgage typically limits the amount of additional repayments you can make – meaning that you will be unable to repay the loan faster than the agreed term to reduce your interest owed.

Variable Rate Mortgage

A variable rate mortgage is a type of home loan where the interest rates change over time based on changes to the official cash rate set by the Reserve Bank of Australia (RBA), as well as other factors affecting the mortgage lender.

This means that the borrower’s home loan repayments can also change, either increasing or decreasing, depending on the interest rate changes.

Variable rate mortgages are a popular choice in Australia, as at different times in the economic cycle they will have lower interest rates than fixed rate mortgages. They can also offer more flexibility in repayment amounts, allowing borrowers to make extra repayments and pay off their loan quicker.

However, variable rate mortgages may not be suitable for those who prefer a predictable repayment schedule or who are concerned about interest rate rises.

Split Rate Mortgage

A split rate mortgage is a type of home loan that allows borrowers to divide their loan into two parts, with one part on a fixed interest rate and the other on a variable interest rate.

Borrowers can choose how to split their loan, giving them the flexibility to structure their loan to suit their lifestyle.

This type of loan offers the benefits of both fixed and variable rate loans, providing borrowers with the security of fixed rate loans and the flexibility of variable rate loans.

The fixed portion of the loan provides certainty of always knowing what a portion of the repayment will be, while the variable portion allows for unlimited additional repayments and competitive interest rates.

However, split rate mortgages may have limited additional payment options on the fixed portion of the loan, and repayments on the variable portion may rise with rate rises.

It is important for borrowers to compare mortgage rate options and consider their individual needs and personal circumstances before deciding on a mortgage.

Mortgage Payments & Average Mortgage Rates

Mortgage rates and payments can vary based on various factors, including economic conditions, housing prices, lender requirements, and individual borrower profiles.

Keep in mind that mortgage rates can fluctuate over time, and economic conditions, including inflation, interest rate policies, and the overall housing market, can influence these rates.

Therefore, it’s crucial to access the most recent and relevant data when considering mortgage options.

Average Mortgage Rates

As of November 2023, the average interest rates on home loans in Australia vary depending on the type of loan and the lender.

According to Canstar, the average interest rates for owner-occupier home loans with principal and interest repayments range from 6.47% to 7.79% for fixed-rate loans and from 6.93% to 7.52% for variable-rate loans.

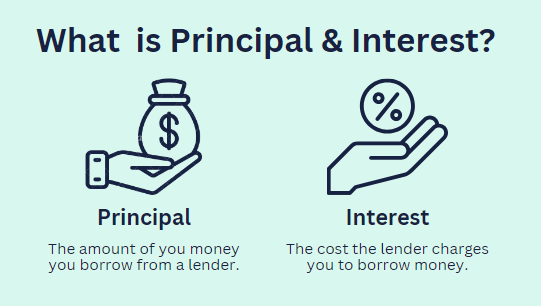

When it comes to mortgage repayment options, there are two primary options available: principal and interest loans and interest-only loans.

Principal and Interest Loans

Most home loans in Australia are principal and interest loans, where borrowers repay both the principal and interest over the length of the loan.

This type of loan is generally cheaper in the long run compared to interest-only loans, as it allows borrowers to pay off the loan principal over an agreed period of time, typically 30 years, in turn reducing the interest payable.

Interest Only Loans

With interest only loans, borrowers only pay the interest on the principal amount for a specified period, after which they will need to start repaying the principal as well.

This type of loan with interest only payments can result in lower initial repayments but may lead to higher repayments when the interest only period ends.

Interest only loans are typically more popular with property investors.

How Long is a Mortgage?

The average mortgage duration in Australia is between 25 and 30 years. The precise length, however, may differ depending on personal preferences, financial situation, and agreements between lenders and borrowers. A small number of lenders even offer 40 year loan terms.

To pay off their loans faster and pay less interest overall, some people choose to have shorter mortgage terms – such as 15 or 20 years. While lengthier periods may result in a lower monthly mortgage payment for some borrowers, they will ultimately incur higher interest costs over the course of the loan.

Note that mortgage terms are subject to negotiation between lenders and borrowers. As such, individuals should carefully assess their financial objectives and capacity before deciding on the length of their mortgage.

Furthermore, borrowers might be able to refinance their mortgages or make additional repayments, which can impact the overall duration of the loan.

What’s the Difference Between a Home Loan & a Mortgage?

A mortgage is the specific legal document that acts as security for a home loan, whereas a home loan is the more general financial arrangement that involves borrowing money to buy a home.

Although the terms are frequently used synonymously, it’s crucial to recognize the differences in specific situations, particularly when talking about the financial and legal ramifications of property ownership.

Getting a Mortgage

Getting a mortgage in Australia involves a systematic process. The following steps provide an overview:

1. Financial Evaluation:

It is advisable for potential borrowers to thoroughly evaluate their financial circumstances. Examining income, spending, and credit history is part of this. Make adjustments where necessary to make your financial position more favourable.

2. Pre-Approval:

To find out how much you can afford to borrow and your borrowing capacity, get pre-approval from a lender. Having pre-approval makes it easier to select a property within your realistic price range. A mortgage broker can help you obtain pre-approval from a lender if you need assistance in shopping around for the most competitive loan.

3. Choice of Property:

Select a home that fits the allocated spending limit and your purchasing criteria. Make in-depth investigations into the location, market, and property values.

4. Application for Loan:

Make a formal loan application to the lender of your choice. The application contains information about the your finances, the property, and the loan amount. A mortgage broker can also help you complete and lodge your formal home loan application and liaise with the lender on your behalf to make the process easier.

5. Assessment and Acceptance:

Prior to approving the loan, the lender evaluates the borrower’s financial stability and the value of the property. A credit check and a property valuation might be required for this.

6. Contract Exchange:

Once the loan is approved, the borrower and the seller exchange contracts, and the borrower pays a deposit.

7. Settlement:

The final step involves the settlement, where the property ownership is transferred to the borrower, and the mortgage funds are released.

First Mortgage vs Second Mortgage

A first mortgage is a primary claim on a property that secures the mortgage, providing the lender with priority over all other claims in the event of default. In contrast, a second mortgage is a subordinate mortgage taken out against a property that already has a first mortgage.

A first mortgage is the primary loan taken out by a borrower to purchase a property.

It holds the first position in terms of priority of repayment in case of default. This means that if the borrower fails to make mortgage payments and the property is sold to repay the debt, the first mortgage lender is the first to be paid from the proceeds of the sale.

Because first mortgages have the primary claim on the property, they are generally considered lower risk for financial institutions. As a result, first mortgages typically have lower interest rates compared to second mortgages.

First mortgages are frequently used to fund the acquisition of real estate, such as homes. A deposit is frequently made by borrowers, who then borrow the remaining sum to complete the purchase of the property.

A second mortgage is a loan obtained in addition to the first mortgage and backed by the same asset.

It is in a secondary or subordinate position to the primary mortgage. If there is a default, the first mortgage lender must be satisfied before the second mortgage lender is paid back.

Second mortgage loan interest rates are usually higher than those of first mortgages because second mortgages pose a greater risk to lenders. The risk is increased if the property must be sold to pay off outstanding debts, as the second mortgage lender might not get their entire investment back.

Second mortgages can be funded for a range of objectives, including debt consolidation, home remodelling, and other significant expenses. Homeowners who have gradually increased the equity in their property frequently seek them out as investment loans.

Is it Difficult to Get a Mortgage in Australia?

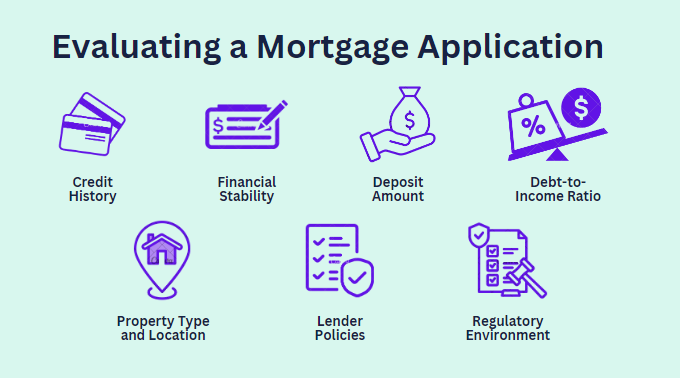

In Australia, a number of factors may come into play when applying for a mortgage, and the complexity of the process varies based on the specifics of each case.

The following variables may affect how tough it is to obtain a mortgage in Australia:

1. Credit History: In order to evaluate your creditworthiness, lenders usually look at your credit history. Getting approved for a mortgage may be simpler if you have good credit.

2. Income and Employment Stability: When determining your ability to repay a mortgage, lenders frequently take your income and work history into account. Having a reliable source of income and work can improve your eligibility.

3. Deposit Amount: Your mortgage application may be impacted by the amount of deposit you are able to make. A bigger deposit could result in better loan terms and increase your chances of approval.

4. Debt-to-Income Ratio: Lenders assess your ability to make mortgage payments by looking at your debt-to-income ratio. It might be difficult for you to get a loan if you have a lot of debt already.

5. Property Type and Location: The lender’s choice may be influenced by the kind of property you wish to buy and its location. The process of getting a mortgage approved may be impacted by properties that are deemed to be higher risk.

6. Lender Policies: The standards and regulations of various lenders differ. Some might have stricter guidelines, while others might have more latitude.

7. Regulatory Environment: Modifications to the law may have an effect on the terms of mortgage lending. Both the state of the economy and governmental regulations can have an impact on the whole mortgage market.

To increase your chances of being approved for a mortgage, you must investigate and compare various lenders, comprehend their qualifying requirements, and work to optimise your financial profile.

Can Foreigners Get Mortgages in Australia?

In general, foreign nationals can obtain a mortgage in Australia, but they must meet a few requirements. For non-resident borrowers, Australian banks and lenders may have particular requirements, and financial institutions may have different requirements.

Here are some important considerations for foreigners applying for a mortgage:

Status of Residency: Non-residents and those with temporary visas may be qualified for a mortgage; however, the particular requirements will vary based on the kind of visa and the lender’s guidelines.

Deposit Requirements: Compared to Australian citizens or permanent residents, foreigners may be asked to provide a larger deposit. Usually, the deposit is stated as a percentage of the total cost of the property.

Income and Employment: The borrower’s income, employment security, and capacity to repay the loan may all be scrutinised to a higher degree by lenders. There may be specific income requirements set by some lenders.

Currency of Income: Borrowers with income in Australian dollars or a significant foreign currency may be preferred by lenders. Certain currencies may be prohibited from being accepted by certain lenders.

Loan Amount: Depending on the lender, there may be a cap on the total amount a home loan that a foreign national can take out. One important consideration when deciding on the loan amount is the loan-to-value ratio, or LVR.

Legal Advice: In order to fully comprehend Australian property laws and regulations, foreign borrowers should consult a lawyer. In Australia, they might also need to designate a legal representative.

Approval from the Foreign Investment Review Board (FIRB): In certain circumstances, non-resident borrowers may require FIRB approval in order to buy Australian residential real estate.

Lender’s Policies: With regard to foreign borrowers, each lender has its own set of rules and guidelines. It’s critical to investigate and evaluate several lenders to select one that best suits your unique circumstances.

Benefits of a Mortgage

There are many benefits to having a mortgage, including the ability to build equity, and the potential for long-term financial gains.

Having a home: The ability to own a home is the main advantage of getting a mortgage. In addition to potential long-term financial gains as property values increase, this provides stability and a sense of community.

Appreciation of Property: Australia has a history of increasing property values over time. This implies that when the value of their property rises, homeowners may be able to accumulate equity.

Creating a Credit History: On time mortgage payments enhance a person’s credit score by positively affecting their credit history. For upcoming financial transactions, having a high credit score may prove advantageous.

Variability in Loan Categories: Australian borrowers have a range of mortgage options to select from, giving them flexibility to match their risk tolerance and financial objectives. Borrowers can choose between a variable rate loan for possible cost savings or a fixed-rate loan for stability.

Is a Mortgage Considered a Debt?

A mortgage is regarded as a type of debt. A mortgage is a type of loan that a bank or other financial institution offers to people or businesses to assist them in buying real estate.

In essence, taking out a mortgage is borrowing money to purchase a property, and you have to pay that loan back over a predetermined amount of time, typically with regular instalments.

Since you have borrowed money that you must repay over the course of the loan, usually with interest, the mortgage itself is a representation of a debt obligation.

Your mortgage is shown as a liability on your financial statements until it is entirely paid off, and you may face foreclosure if you are unable to make the required payments.

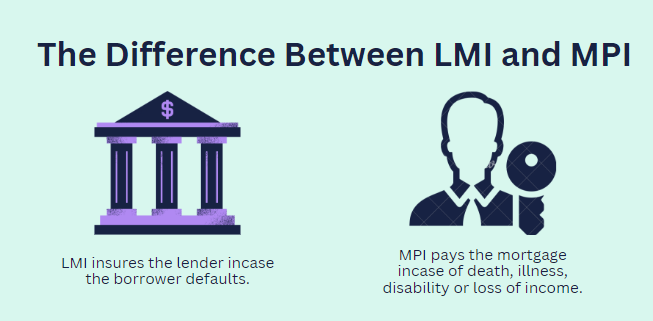

Do You Need Mortgage Insurance?

In Australia, mortgage insurance is an essential part of the home-buying process because it protects both lenders and borrowers.

If the deposit made by the borrower is less than twenty percent of the property’s value, Australian lenders usually demand mortgage insurance.

Lender’s Mortgage Insurance (LMI) and Borrower’s Mortgage Insurance (BMI) are the two primary categories of mortgage insurance in Australia.

Lender’s Mortgage Insurance (LMI): If the borrower defaults on the loan and the remaining amount is not paid off through the sale of the property, LMI safeguards the lender. This insurance broadens the pool of potential homeowners by enabling borrowers to enter the real estate market with smaller deposits.

Mortgage Protection Insurance (MPI): Mortgage protection insurance, aka home loan insurance, is a life insurance that safeguards borrowers in case they cannot repay their home loan due to unforeseen events like death, illness, or involuntary employment loss. It covers mortgage repayments, ensuring the borrower’s beneficiaries can retain their home.

Because it helps to reduce risk for both parties to a mortgage transaction, mortgage insurance is important. For lenders, it offers a safety net in case of unforeseen circumstances, and for borrowers, it allows entry into the real estate market with a smaller deposit.

How Much Can I Borrow?

The amount that a person can borrow for a mortgage in Australia is determined by a number of factors, and lenders evaluate a borrower’s ability to borrow money based on predetermined standards. Among the crucial elements are:

Income and Expenses: To ascertain the borrower’s ability to make mortgage repayments, lenders consider their income as well as their current debts.

Credit History: A borrower’s credit history is a crucial aspect of the loan application process. A positive credit history increases the likelihood of loan approval, while a poor credit history may limit borrowing options.

Size of Deposit: The amount that can be borrowed depends largely on the size of the deposit. A higher deposit lowers the loan-to-value ratio (LVR), which lessens the lender’s risk.

Interest Rates: The ability to borrow money is impacted by current interest rates. The amount that a borrower can afford is impacted by higher interest rates because they lead to higher repayments.

Loan Duration: The amount that can be borrowed depends on the loan term’s duration. While monthly repayments for loans with shorter terms may be higher, the total cost of interest may be less.

Additional Debts: Borrowing capacity is impacted by current financial obligations, such as credit card debt or personal loans. The borrower’s capacity to handle additional financial obligations is taken into account by lenders.

Workplace Stability: Lenders evaluate the borrower’s work stability. A reliable and steady source of income is advantageous for loan approval.

Situation of the Market: Lending standards are susceptible to changes in the economy and real estate market trends. Lenders may become more conservative in their lending practices during uncertain economic times.

In order to increase their ability to borrow money, borrowers must be aware of these factors and take steps to improve their financial situation. Acquiring expert financial guidance from a mortgage broker can aid in managing the intricacies of the loan application procedure.

In summary, mortgages are essential to making homeownership a reality and helping people fulfil their aspirations of becoming homeowners.

Careful financial planning, the selection of a property, and adherence to both financial and legal obligations are all necessary steps in the mortgage application process. For many Australians, mortgages are an alluring option because of the advantages of homeownership, which include possible property value appreciation.

Check Your Borrowing Power with MMS Mortgage Calculator

Make informed decisions and embark on a path towards your dream home by gaining insights into your borrowing capacity.

Take the first step towards your homeownership goals – Check Your Borrowing Power with the MMS Mortgage Calculator today.

Knowing your borrowing power is just the first step. A mortgage is a big investment of both time and money, which is why it’s often best to receive guidance from a financial expert like a mortgage broker.

Speak with a Money Guru Today

Your future home may be waiting just around the corner. Our team of financial experts is ready to assist you in navigating the complex world of mortgages, interest rates, and borrowing power.

Don’t hesitate to reach out and schedule a consultation with one of our Money Gurus today. Together, we can create a tailored financial plan to help you achieve your homeownership goals. Your dream home is within reach, and we’re here to guide you every step of the way.