Are you a freelancer, contractor, a casual employee, self-employed, or a small business owner trying to secure a home loan?

Chances are you’re at your wits’ end trying to meet the standard home loan proof of income requirements.

Don’t despair!

Low Doc Home Loans could be the golden ticket that could help you get on the property ladder sooner.

So, sit back, relax, and learn about the requirements for this kind of loan, its pros and cons, what makes it different from full doc home loans, and useful tips on how you can get approved when you lodge your loan application.

Jump straight to…

How Does a Low Doc Loan Work?

When you apply for a home loan, you normally have to prepare a mile long list of documents for the lenders. Well, that’s a bit of an exaggeration but that’s how it may actually feel for most borrowers.

Lenders typically assess your application based on:

- Your income

- Your ability to afford and repay the loan

- Your credit history

To help lenders in their assessment, you will be asked to disclose your income and other assets, provide basic identification credentials, and confirm your capacity to cover the deposit and other add-on fees associated with the purchase.

For borrowers like you who don’t fit the typical profile of a standard home loan applicant due to a lack of pay slips or other proof of regular income source, alternative documents will be required to prove your income.

Who are Low Doc Home Loans Ideal For?

If you do not work in a traditional employment set-up, it could mean that you do not receive monthly wages and, as a result, are unable to submit proof of income documentation (such as a pay slip) in accordance with conventional procedures.

What you may have, however, are evidence of your annual income and savings you have set aside that can cover for loan repayments.

Low Doc Home Loan Criteria

Now that you have your eyes set on a low doc home loan, let’s drill down into the details of how you can possibly obtain a loan for your dream home.

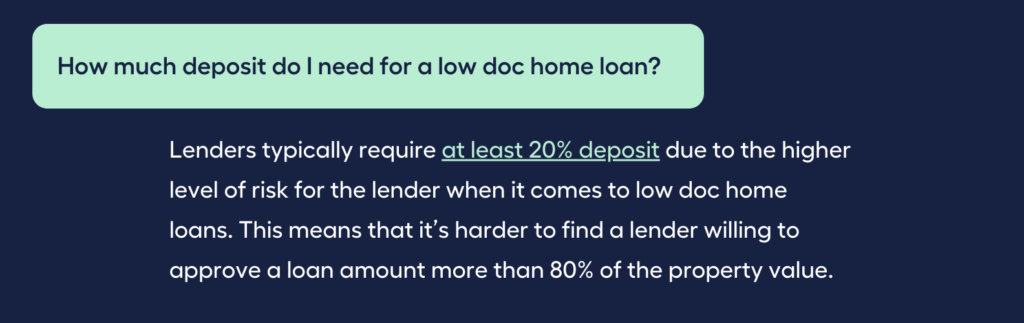

How much deposit do I need for a low doc home loan?

Lenders typically require at least 20% deposit due to the higher level of risk for the lender when it comes to low doc home loans. This means that it’s harder to find a lender willing to approve a loan amount more than 80% of the property value.

And so, even if you are ready to shell out the 20% deposit, you may still be required to pay for lender’s mortgage insurance (LMI) or be asked to pay a bigger deposit to compensate for the corresponding risk assumed by the lender.

For example:

If you borrow up to 60% of the property value, the loan package could come with standard home loan rates.

If you borrow up to 80% of the property value, the loan package could come with competitive interest rates and may have an add-on risk fee or LMI.

If you borrow up to 90% of the property value, the loan package could come with high interest rates and LMI. The steep interest rate will also depend on the type of verification or supporting paperwork you can provide to the lender.

What documents do you need for a low doc loan?

Although low doc loans require less paperwork from borrowers, there are still documentation requirements you need to fulfill as a borrower to prove your income and loan serviceability.

When it comes to required documents, each low doc home lender differs in criteria to a certain degree.

Documents needed for a low doc loan may include:

- Business Name and Australian Business Number (ABN) registration

- Business Activity Statements (BAS)

- Proof of GST registration

- Personal tax returns

- Bank Account Statements

- Profit and Loss Statements and/or

- Accountant’s letter verifying your financial position

The Accountant’s letter needs to confirm the following:

✓ Your Full Legal Name

✓ Your Business Trading Name

✓ Years of Service

✓ Gross Taxable Income (last 3 years)

✓ Deductions (like interest or depreciation)

Accountant Letter Format:

✓ Letterhead

✓ Contact Details

✓ Qualification Membership

✓ Industry Membership

The Pros & Cons of Low Doc Home Loan

If you’re looking for lower interest rates and you have enough supporting documentation, a full doc home loan may be the right fit for you.

If a low doc home loan is your only option, you can very well give it a shot as long as you take note of potential advantages and disadvantages before signing a mortgage agreement.

| Pros and Cons of Low Doc Home Loan | |

| Pros | Cons |

| ✓ Less PaperworkA low do home loan can be your ticket to get on the property ladder without the standard proof of income requirements | X Higher than average interest rate More expensive than a standard home loan because lenders see you as a borrower prone to higher risk due to unpredictable income source |

| ✓ Save Time It’s typically an easier application process as lenders tend to have vastly reduced documentation requirements | X Higher deposit requirement Low doc loan lenders typically offer lower loan-to-value ratio (LVR), requiring higher deposits and lower loan amounts. Often, borrowers need to put down at least a 20% deposit. Lenders who may be willing to offer up to 95% loan amount will most likely charge substantially higher interest rates. |

| ✓ If you have a great credit score, you can negotiate the loan terms | X Lender’s Mortgage Insurance (LMI) may be required if loan amount is more than 60% of property value |

| ✓ Convert from Low Doc to Full Doc Some lenders allow borrowers to convert low-doc home loans to a full doc loan after two to three years if loan payments have been completed on time. This may also result in a slight interest reduction. | X A limited number of lenders offer low doc home loans which restricts your options and makes negotiating for lower interest rates more challenging. |

What are the Main Differences Between a Low Doc & Full Doc Home Loan?

Apart from the application procedure, low doc loans do differ from standard loans in a few areas.

Here’s a side-by-side comparison of these two types of home loans:

| Low Doc Home Loan vs Full Doc Home Loan | ||

| Low Doc Home Loan | Full Doc Home Loan | |

| Income Verification | Less financial documentation required Uses flexible, self-verification process through a signed Borrower Income Declaration Form as proof that borrower has capacity to repay the loan | More financial documentation required (standard docs like pay slips, bank statements, 2 years of tax returns) |

| Deposit | Typically larger, up to 40% in some cases | Usually, 20% of the property value |

| Interest Rate | 1-2 percentage points higher than full-doc loan *To make up for the higher risk that lenders assume by lending you money without fully confirming your income | Set in accordance with the official cash rate of the Reserve Bank of Australia (RBA) and market rates |

| Loan-to-Value Ratio (LVR) | Lower maximum LVR Most lenders will not offer a loan amount more than 80% of property value | Some lenders may allow more than 80% LVR under certain circumstances |

| Lender’s Mortgage Insurance (LMI) | Lenders may require LMI for loan amount that is more than 60% of property value | LMI required if loan amount is more than 80% of property value |

Tips to Get Approved for a Low Doc Home Loan?

Borrowers are finding it more challenging to get their home loans approved due to the fact that low doc home loan lenders are now trying to manage potentially high-risk products by enforcing stricter requirements that could very well make low doc loans resemble standard loans.

But don’t throw in the towel just yet!

Here are Some Tips to Help Increase Your Chances of Getting Approved for a Low Doc Home Loan:

Tip #1

Reduce Your Debt

Reduce the credit limits on credit cards and personal loans as you pay them off because lenders consider your overall credit availability in addition to the amount you owe when determining your potential debt level.

Tip #2

Consult a Mortgage Broker

A mortgage broker can assess your situation as a freelancer, independent contractor, and small business owner to see how your taxable income will impact your ability to borrow.

After having a better picture of your financial situation, a Mortgage Broker (also known as a Finance Broker) can connect you to specialist lenders who consider each application individually and develop solutions exclusively for self-employed borrowers like you.

Tip #3

Lodge Your Tax Returns

Make sure to lodge your tax returns on time and pay any assessed tax liabilities, the tax you owe the ATO, on schedule.

Tip #4

Make Saving a Habit

The ability to budget your spending and to save is the cornerstone of your home ownership dream through a home loan. Lenders will assess your capacity to pay for a loan by looking for at least a six-month history of high savings and low expenses.

Check Your Borrowing Power with MMS Mortgage Calculator

Knowing your borrowing power is just the first step. A mortgage is a big investment of both time and money, which is why It’s often best to receive guidance from a financial expert like a mortgage broker.

Many people may be unaware of this…but just like you, 41% of Aussies intend to get financial advice rather than going it alone, according to an Australian Securities and Investments Commission (ASIC) report.

Find the right Mortgage Broker for you with the help of My Money Sorted.

When you book a call with My Money Sorted, you’ll:

✓ get a better understanding of your financial options

✓ have an idea of the experts you can call on to help you reach your goals

✓ be matched with a mortgage broker who can help develop the best home loan strategy for your situation

My Money Sorted is your stress-free pathway to getting ahead with your home loan.

Here’s what your journey will look like:

Step 1: Start off with a quick money matters session with My Money Sorted

Step 2: Get matched with a licensed Mortgage Broker that’s right for your financial situation

Step 3: Take the first step towards your financial goals with a clear roadmap that makes sense prepared by an experienced Mortgage Broker.

It’s that easy!

Get Ahead Of Your Home Loan by Speaking with My Money Sorted Today