You may be reading this article because you are getting close to or have recently passed the age of 40.

Looking at those around you, you’ve made a quick assessment of what they’ve achieved in their lives:

✓ Successful career or a stable and well-paying job

✓ Instagram-worthy home and a nice car

✓ Cash in the bank, an investment portfolio, and a retirement plan set up

As you compare yourself to others you start to panic. Reflecting on your life, you wonder:

Is it too late to save for retirement at 40?

Say hello to middle age, a time when many start to feel like they’ve missed the opportunity to get set up financially, a mindset that, if not shifted, will lead to things going downhill quickly.

But has the opportunity to get set up financially really passed us by at the age of 40, or are we at a prime age to do so?

Studies show that if you find your purpose in life, you can have and achieve anything you want.

In the context of retirement, having a financial purpose, by working on a retirement savings plan, could help see you through a midlife financial crisis.

In this article, we cover the best ways to address a midlife financial crisis by:

- Looking at ways to get your retirement savings up to date in your 40s

- Identifying who can best help you in creating a retirement savings plan, and

- Going through the steps that could pave the way for a comfortable retirement

Jump straight to…

How to Catch Up on Retirement Savings in Your 40s

The first thing you need to check is your money mindset:

What is your perspective when it comes to your age – are there limiting beliefs that are holding you back from living your best life?

While we’ve been made to believe that when we hit 40 all we have to look forward to is:

…grey hair starting to multiply every time you look at the mirror

…joint pains stopping you from being as active as you were in your 20s

…needing prescription glasses to read the menu of your favourite restaurant

…getting fed up with your current job and wanting to make a career shift

…going through a divorce…

We can also choose to look at this stage in life between young adulthood and old age from a different perspective summed up by the saying:

Life begins at 40.

You may have had some detours in your younger years due to wrong money decisions, but your past does not define your future. You can always start anew.

To move forward, we could always transform mistakes into valuable lessons that could lay the groundwork for the best decades of your life.

Think about it—at 40, you are:

…approaching your peak earning potential

…more aware of your money goals and situation

…wiser due to lessons learned from the past

…and more confident because of the wisdom gained through the years.

Age is not a barrier, but rather a chance to realise your full potential and live the life you’ve always wanted.

But you don’t have to bust a gut working to save for a hefty retirement income to make your retirement dream a reality. Instead of gambling on your future, consider seeking financial advice from a financial planner to help chart the course of the best decades of your life.

Work with a Financial Planner to Create a Retirement Savings Plan

All of us are familiar with the four seasons of the year, but do you also recognise the four seasons of your own life?

A reason exists for every season.

You may be in the winter season of your life right now:

Feeling stuck inside a sinking ship in the middle of an ocean of debt, hoping somebody hears your cries for help and sends a money rescue team who can bring you back to financial security.

- Remember: whatever the season is right now, it will change once more.

Winter is the best time for you to learn and plan for the next money season of your life.

Sure, a successful financial future would be easy to plan and predict if you were an oracle. Luckily, you don’t have to be one when planning for your retirement savings because there are financial planners who can give personal financial advice.

Financial Planners:

- Can work with you in creating a retirement savings plan. They have the expertise in researching and choosing the financial products that match your personal needs and particular circumstances when it comes to retirement planning.

Financial planners can take care of your long-term growth strategy, including superannuation funds, life insurance, and other types of wealth protection insurances so you can avoid the mistakes which may cost you time and money, mistakes that can be very common when you try to do it on your own.

You might be thinking right now:

Retirement savings tips and tricks can be easily found online.

That is absolutely true.

But do you know the key element these online resources lack?

A step-by-step retirement savings plan developed by an experienced financial planner that is customised to your unique personal circumstances.

A financial planner can help you to:

✓ Spend less while building your wealth

✓ Increase your superannuation account balance using tax-efficient methods

✓ Safeguard your income

✓ Build a portfolio of investments

In other words, the work of a financial planner is extensive and crucial to your long-term security and financial health.

Define Retirement Savings Goals

In general, there is no “one-size-fits-all” amount when it comes to retirement savings. Understanding your preferred retirement lifestyle will help define your retirement savings goals. You can then use these goals to calculate how much income you need to save for the future.

Calculate Retirement Income: How Much Will You Need For a Comfortable Retirement

To calculate your retirement income, you can start by defining what a “comfortable retirement” means to you. The next step is calculating how much money you’ll need to reach your retirement income objectives once you have a clear picture of the “comfortable retirement” you desire.

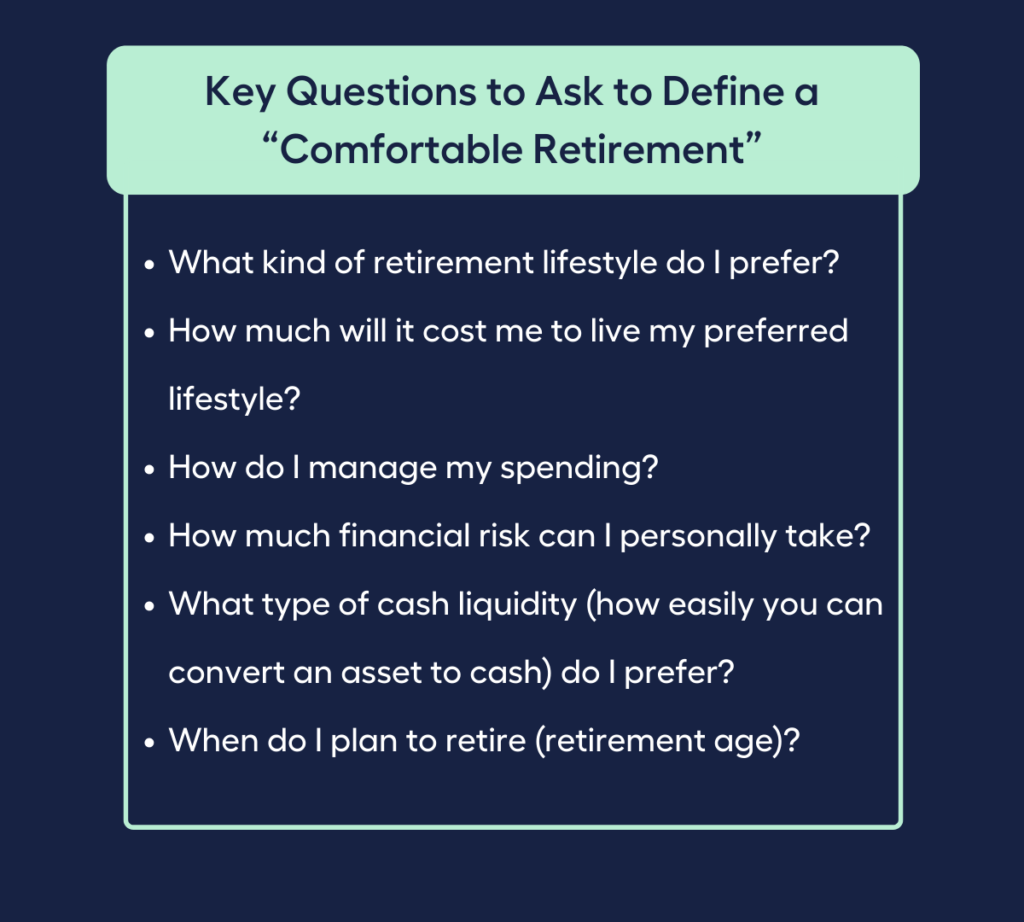

Key Questions to Ask to Define a “Comfortable Retirement”

- What kind of retirement lifestyle do I prefer?

- How much will it cost me to live my preferred lifestyle?

- How do I manage my spending?

- How much financial risk can I personally take?

- What type of cash liquidity (how easily you can convert an asset to cash) do I prefer?

- When do I plan to retire (retirement age)?

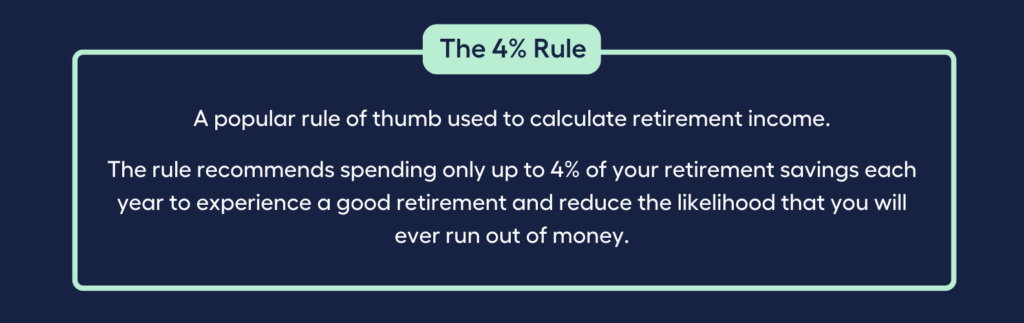

A popular rule of thumb to calculate retirement income is the 4% rule. The rule recommends spending only up to 4% of your retirement savings each year to experience a good retirement and reduce the likelihood that you will ever run out of money.

If you’re looking for specific figures as a benchmark, the Association of Superannuation Funds of Australia (AFSA) has released a retirement standard for comfortable and modest living.

According to AFSA, the comfortable annual retirement income for singles is $47,383 and $66,725 for couples, while the modest annual retirement income for singles is $30,063 and $43,250 for couples.

Do you think this amount is enough for your needs and wants come retirement age?

To estimate how much retirement income you will need, you can start by tracking your current expenses.

Get a better understanding of your expenses by using the MMS Expense Planner calculator. You can input a variety of income and expense items to serve as a guide for your financial position. It will then calculate how much you are spending based on your frequency choice (weekly, monthly, annually).

Get Your Retirement Accounts Sorted

Now that you have a benchmark for your retirement income, it’s time to shake your money maker to explore options that can help make you money.

Your financial life may still be in the winter season right now but anticipate the coming of spring — the time to act and seize opportunities.

Get to work by sorting your retirement accounts starting with your superannuation.

Superannuation (aka “super”) is the portion of your salary and savings set aside in a fund to support you through retirement years.

It’s extremely important that you keep track of your superannuation balance because it will have a big impact on your retirement savings. To make your super grow, you must put it to work.

Below are some of the different ways to make the most of your super.

Two Ways to Make Super Work for You:

1. Review and Consolidate Your Super

2. Give Your Super a Boost

1. Review and Consolidate Your Super

If this is the first time in ages that you have thought of your super, now is a good time to conduct a super review. Your default super plan may not be the right fit for your situation and retirement income goals.

Why?

Employers simply pay super into the fund nominated by the employees. In instances where the employee doesn’t have a super fund to begin with, the employer will simply pay super into a default super fund.

For example, if you have a default super fund, you may be paying high super fees that are taken out of your potential retirement income. Additionally, your money may be sitting in a poor performing super fund which may mean you are not receiving the highest possible returns.

Also, you may have switched employment or changed addresses a couple of times and now have several super accounts, which means you are paying annual fees on multiple accounts.

By paying only one set of fees when you combine all your super accounts into one, you can save money. There is less paperwork, and it is easier to keep track of your super balance when you simply have one account.

Furthermore, insurance and other financial services are typically included in super funds, with allocations done automatically.

Thus, when reviewing your super, you need to check if these insurance products (that could contribute to your retirement income) are included in your super:

- Life and Death Cover

- Total and Permanent Disability (TPD) benefit

- Income Protection Insurance

You can also choose the super fund that best suits you if you are eligible to do so.

If you’re doing a DIY review and consolidation of your super and you suddenly find yourself lost in the process, seeking the expert advice of a financial planner to help customise your super account can be a worthwhile alternative.

2. Give Your Super a Boost

Can you imagine yourself enjoying these things that spark joy and provide comfort when you reach retirement age?

✓ recreational activities

✓ dining out

✓ local and international holidays

✓ home renovations

✓ private health care

Boosting your super savings by making extra contributions can help make these retirement aspirations a reality.

Ways to Boost Super Contributions:

Booster #1

- Before-Tax Contributions (aka Concessional Contributions)

Concessional contributions are the money deducted from your salary pre-tax. With the power of compound interest, these contributions could be a solid source of retirement income.

Examples of before-tax contributions are Superannuation Guarantee (SG) contributions, employer award contributions, additional pre-tax contributions from employer as part of the salary package, salary sacrifice contributions, personal contributions with a tax deduction, and First Home Super Saver (FHSS) Scheme contributions.

Booster #2

- After-Tax Contributions (aka Non-Concessional Contributions)

Non-concessional contributions are any additional contribution you make for which you have already paid taxes. This could be extra money from an inheritance, dividends, a bonus, or even a windfall.

Aside from the perk of non-concessional contributions being exempt from taxation, it will also be totally tax-free when you access your super in retirement, whether in the form of a lump sum payment or in increments as part of a pension.

You may also be eligible for a super co-contribution from the government if you make a non-concessional contribution.

Make a Budget to Live Below Your Means

At age 40, budgeting is a must to get ahead with your money. Budgeting provides healthy boundaries to your hard-earned money by giving each dollar a purpose — helping provide for your needs as well as growing your money too.

You may have felt optimistic during the financial spring season in anticipation of the fruits of the retirement accounts you’ve sorted, but summertime in the money season is not the time to relax. Now is the time to develop good money habits by making a budget to live below your means.

A budget accounts for both income and expenses over a given time frame, such as a month or a year.

A budget allows you to:

- optimise your income

- reduce your spending

- get financial clarity

All in all, it is a tool to help reach your money goals.

3 Types of Personal Budgets:

1. Zero-Based Budgeting Method

The Zero-Based Budgeting Method follows the concept that each dollar in your budget needs to be given a category and serves a purpose such that at the end of each month, you’ll be able to track down 100% of your money.

In contrast to a traditional budget that allows excess money to be spent on unnecessary items or left just sitting in your savings account, a zero-based budget forces you to allocate any extra money to savings, debt repayment, or any other money goal.

Ultimately, the goal is to have no money left over at the end of each month.

2. The 50/30/20 Budget

If you’re a beginner when it comes to budgeting, the 50/30/20 budgeting method may be fit for you because it is easy to understand.

The objective is to divide your expenses into three categories:

- Utilities, Rent, Groceries, and Other Fixed Expenses = 50%

- Discretionary costs (such as those for shopping, entertainment, and nights out) = 30%

- Savings and debt repayments = 20%

| 3 Categories of The 50/30/20 Budget | |

| Utilities, Rent, Groceries,and Other Fixed Expenses | 50% |

| Discretionary costs (such as those for shopping, entertainment, and nights out) | 30% |

| Savings and debt repayments | 20% |

As long as you know the difference between a want and a need, and set aside enough money for savings and debt, you can keep to this budget.

3. The Goal-Based Budget

If you’re working towards a specific money goal, you may want to consider the Goal-Based Budget Method.

For example, you need to upgrade your car for your growing family and so you need to save for a deposit. Or maybe you need to save for a trip to attend the island resort wedding of your best friend. These goals should be funded entirely by the short-term income you get.

To achieve this goal, you might even need to make sacrifices in other areas of your spending plan.

- Do take note that it is not effective for long-term budgeting. This is because your spending and saving patterns will probably change to match your new goal.

Just remember that when making a budget, there is no right or wrong approach. Some prefer to write their budget down on paper, while others prefer to use a spreadsheet or budgeting tool. Choose a method that works best for you.

Get started by keeping track of your income and expenses using the MMS Budget Planner calculator. It can help give you a better understanding of your financial position and can also show how much more you are spending than earning.

Reduce, Refinance, or Consolidate Debts

Any of these items on your list of debts?

- Credit cards

- HECS debt

- Car loan

- Mortgage

Feeling overwhelmed?

Even if repayments for these debts are current, keeping track of all the payments can be a hassle and can stress you out, preventing you from focusing on earning income that can contribute to your retirement savings.

This brings us to a major take-away when it comes to debts:

Learn how debt affects retirement planning.

Understanding good and bad debt is essential when building a safety net for retirement.

Debt consolidation can reduce stress and interest rates and could help you better manage your current money situation. However, it won’t reduce the total amount you owe, and a thorough assessment of its long-term implications is a must.

Learn ways to cut down on bad debt as well. Handle credit card debt responsibly by paying in full and on time to avoid credit card fees. But if paying in full isn’t possible due to your present circumstances, try to pay more than the minimum to avoid interest building up.

Refinancing your mortgage is another opportunity to save money because keeping your existing mortgage may require you to pay an expensive home loan loyalty tax. By considering a new home loan with a different mortgage lender, you may be able to access a loan with lower interest rates which, in the long run, means more savings.

Protect Yourself with Insurance

One option you need to consider when saving for retirement is insurance. It can protect your ability to save money that will serve as a reliable source of income in retirement.

If an unexpected illness or injury were to shorten your working life, the correct insurance can help you maintain your super payments and accumulate the retirement savings you’re aiming for.

A good place to start when deciding what type of insurance you may need once you retire is to assess your needs in light of your lifestyle preference.

Questions to help determine the right insurance cover for your preferred lifestyle:

1. In case of my death or disability, how much money would my family need to pay for my expenses?

2. If my family’s source of income is abruptly cut because I am unable to return to work due to a disability, or if I were to pass away, how would they manage to pay for recurring expenses like rent or mortgage repayments?

Although some types of life insurance may be included in your super, consider reviewing if it provides the right level of protection for your situation. Life and Death Cover, Total and Permanent Disability (TPD) and Income Protection insurances are common forms of insurance that will ensure you’re covered on all bases.

Consider Building Retirement Savings with Investments

After retirement, you will no longer have a steady income stream. Aside from your superannuation account, another way to grow your money during your financial spring season is by investing.

The two common investment strategies are:

Defensive Investing and Growth Investing.

Defensive investing is a strategy that aims to consistently generate investment income rather than focusing on capital growth. When you’re not spending your money, you can use this strategy by making a deposit in a high-interest savings account or investing in fixed-interest assets like term deposits, corporate bonds, and government bonds.

On the other hand, growth investing is for individuals who are able and willing to tolerate market fluctuations. The goal of this investment strategy is to increase the value of money invested. Examples are investments in shares and real estate.

These investments can be “planted” during the spring and summer seasons of your financial life; thus, you need to persist to reap the results when autumn arrives — your retirement.

It’s Never Too Late to Start Saving For Retirement

Winter, spring, summer, or autumn — as one season ends, another one begins. Like the four seasons, when a life chapter ends, a new chapter begins. Making the appropriate retirement savings plan will make it possible for you to live the future you want in the next chapters of life.

It doesn’t matter where you start. All that matters is you do.

But you don’t have to do it alone.

What if, instead of taking the all too common ‘hit-and-hope’ approach when it comes to planning for your retirement, you could tap into the wisdom of an experienced financial adviser?

Many people may be unaware of this…but just like you, 41% of Aussies intend to get financial advice rather than going it alone, according to an Australian Securities and Investments Commission (ASIC) report.

Find the right Financial Planner for you with the help of My Money Sorted.

When you book a call with My Money Sorted, you’ll:

✓ get a better understanding of your financial options

✓ have an idea of the experts you can call on to help you reach your goals

✓ be matched with the right financial planner who can help simplify your family’s journey to financial wellness

My Money Sorted is your stress-free pathway to getting ahead with your money.

Here’s what your journey will look like:

Step 1: Start off with a quick property investment alternatives session with My Money Sorted

Step 2: Get matched with a licensed Finance Planner that’s right for your money situation

Step 3: Take the first step towards your money goals with a clear and sound roadmap prepared by an experienced Financial Planner.

It’s that easy!

Speak with My Money Sorted Today About Your Retirement Planning Needs and Get Your Money Sorted Today