Imagine you’ve discovered a property that would make a good investment, but you don’t know where to begin when it comes to making a loan decision.

Should you get a mortgage that’s interest only or principal and interest for your investment property?

In this article, we’ll go over loan options with you so you can use the knowledge to choose a path that best meets your needs.

Jump straight to…

Difference Between Interest Only and Principal & Interest for Investment Property

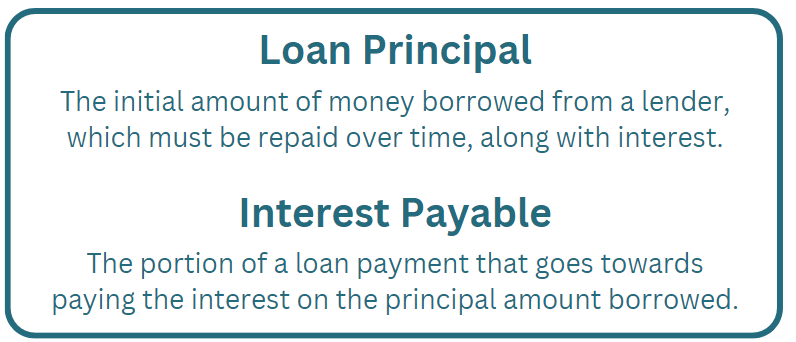

Your home loan consists of the loan principal and interest. The amount you borrow to finance your property purchase is known as the loan principal. On the other hand, the cost that the lender charges for borrowing the principal amount is known as interest.

The principal amount of interest only payments on home loans stays the same during the interest only period; the only component of the loan payment is the interest payable.

There are two main options available to you when looking for an investor home loan: interest only home loans and principal and interest home loans.

It’s important to understand how these different types of loan repayments work and how they might change in order to make informed financial decisions.

Interest Only Loans

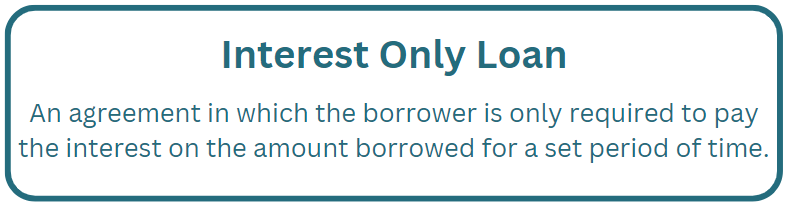

An interest-only loan is a type of home loan in which the borrower is only required to pay the interest on the loan for a pre-determined period of time. During this time, the principal amount remains unchanged.

After the interest-only repayment period ends, the borrower may have several options, such as paying off the loan balance, refinancing the mortgage, or beginning to pay off the balance in higher monthly payments, which include both interest and principal.

There are some benefits to interest only loans that make them desirable in some circumstances.

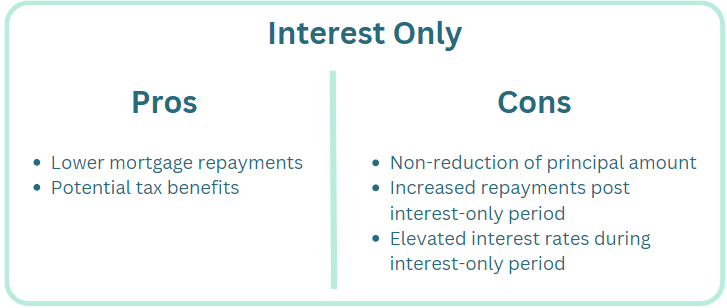

One significant benefit that gives borrowers flexibility is the offer of reduced mortgage repayments for a certain period of time. This feature is especially helpful for people who are changing their lifestyle, like taking time off work to take care of their children.

Furthermore, interest only loans might offer financial incentives to some borrowers in the form of potential tax benefits, particularly when used for investments.

Interest only loans allow you to save money for things like home improvements or the purchase of a new property because they have lower payments during this time.

But while interest only loans may seem appealing due to their lower monthly payments, it’s crucial to be aware of their potential drawbacks.

If you are not prepared, the loan repayments may increase suddenly after the interest only period ends. It is important to plan ahead because this sudden increase in costs can come as a surprise, and you may end up paying more interest.

Interest Only Repayments

It is wise to take proactive steps to prepare for the increase in home loan repayments that will occur when the interest only period ends.

First and foremost, you should create a detailed plan outlining how you will switch from interest only repayments to principal-and-interest repayments. This preparation guarantees a more seamless transition in finances.

In addition, there are other ways to reduce the home loan balance, like refinancing or thinking about selling the property before the interest only period ends.

Thirdly, to actively reduce the principal amount during the interest only period, a proactive approach entails making extra repayments. However, this option can be counterintuitive as to why you chose interest only in the first place.

By taking these proactive and forward-thinking steps, borrowers will be better equipped to deal with the shifting dynamics of their loan structure and repayment frequency.

Seeking the expertise of a financial advisor can be very helpful when making these difficult decisions. To maximise financial results, a financial advisor can offer specialised insights, evaluate unique financial situations, and develop individualised plans.

Is it good to have interest only on investment properties?

For some investors, interest only loans for investment properties may be a good choice, but there are risks and considerations to analyse. Here are some important things to think about.

Benefits of Interest Only Investment Loans

Interest only loans have the potential to have lower initial repayment amounts, which enables investors to better control their cash flow. The interest paid on investment loans is also typically tax deductible; an interest only loan can optimise these advantages.

Risks and Considerations

The borrower does not reduce the principal during the interest only period, leaving the loan balance unchanged. The total interest paid over the course of the loan exceeds that of a principal-and-interest loan because the principal is not touched during the interest only set period. The loan switches to principal-and-interest repayments at the end of the interest only set period, which could result in a significant increase in repayments.

Investment Suitability

Investors with a clear strategy and the ability to manage associated risks may find interest only loans appealing. Interest only loans may be beneficial for investors who place a higher priority on cash flow management and tax benefits than long-term equity growth.

How long can you have interest only on an investment property?

Depending on the lender, investment properties in Australia have different maximum interest only terms. This time frame usually lasts for five years after the settlement date.

Some lenders do, however, offer investors longer interest only loan terms, up to ten years in general. It’s important to speak with your specific lender to find out the exact maximum interest only period that applies to your investment property.

The loan will convert back to a principal and interest home loan for the balance of the term after the interest only period ends. Higher repayments could result from this shift, which might surprise borrowers who might have forgotten the interest only home loan period had ended.

Principal and Interest Loans

A principal and interest loan includes consistent repayments of the principal borrowed plus the interest accrued. The repayment amount is determined so that, at the end of the loan term, the loan principal is fully repaid.

In contrast to this loan arrangement, an interest only loan requires the borrower to pay back only interest for a predetermined amount of time, typically up to five years, before you start paying the principal amount borrowed.

Principal and Interest Repayments

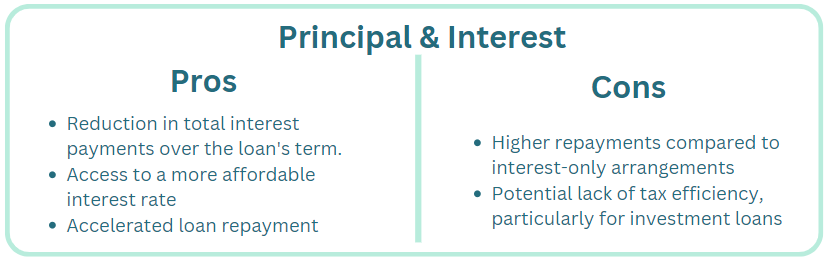

Choosing a loan with principal and interest has various benefits. First off, during the course of the home loan repayments, borrowers will pay less in interest. Furthermore, when compared to comparable home loans with an interest only structure, this loan type frequently has a lower interest rate. An additional noteworthy advantage is the quicker loan payback schedule, which enables early full property ownership.

A principal and interest loan does have certain disadvantages, though. Short-term cash flow is impacted because the regular repayments are typically higher than those linked to interest only loans. Moreover, investment loans might not be as tax-efficient as other loan types, so the overall financial plan needs to be carefully considered.

What is the best way to structure an investment property loan?

The best way to structure an investment property loan involves several factors, including your goals and purpose for the property purchase, your financial situation, payment flexibility, deposit, up front expenses, the different home loan products available to you, and ability to claim higher tax deductions. It’s important to consider the trade-offs that come with loan repayment types and loan structures, such as potentially higher interest rates and overall interest costs.

Should I pay interest or principal and interest?

With interest only loans, the borrower is only required to pay back the interest on the principal amount borrowed for the pre-determined timeframe, and no principal reduction is required. Interest costs on interest only loans can be tax deductible, even though they are typically higher than on principal and interest loans. Investors who depend on an increase in property value or rental income to pay off the loan frequently use this strategy.

On the other hand, principal and interest loans require you to pay back the loan interest as well as gradually lower the principal amount over time. Principal repayments lower the loan’s total interest expense and raises the property equity. This strategy is appropriate for people who want to increase the equity in their investment property and eventually become the sole owners.

A significant choice must be made when obtaining an investment property loan: should you concentrate on making interest only repayments or start lowering the loan amount?

Making this decision will help you customise a loan to meet your financial objectives. Long-term success depends on knowing the effects of principal and interest or interest only loans as the real estate market shifts.

Let’s go over important factors to assist you in making a choice that will support your goals.

Setting Your Objectives

Identify your primary financial goal, which may be to achieve capital growth, produce rental income, or both. If your goal is to maximise your rental income, an interest only loan might be a better fit. On the other hand, a principal and interest loan might be a better option if increasing the value of the property is your top priority.

Analysing the Real Estate Market

Analyse the real estate market as it stands today and any foreseeable changes. It might be beneficial to choose an interest-only loan if property values are predicted to increase. A principal and interest loan might be a better option in a steady or downturning market. Again, you need to circle back to your objectives when making this decision.

Assessing Your Ability to Take Risks

Think about how much risk you are willing to accept when investing in real estate. A principal and interest loan is generally regarded as less hazardous. This option gives your investment journey a structured approach by allowing you to gradually increase the property equity over time.

Strategies for Optimising Real Estate Investment Loans

Investing in real estate can be a profitable venture, but it requires careful planning and strategic decision-making to maximise returns and minimise risks.

One crucial aspect of this is optimising real estate investment loans, which involves exploring various lenders, maximising tax deductions, and choosing the right loan structures among others to enhance cash flow, returns, and tax benefits.

Exploring Diversified Lenders

Look into several lenders in order to discover the best possible deals and rates. This can lower your interest costs and improve the stability of your finances for any further real estate investments you make.

Optimising Loan Structure

Choosing the right loan structure is important to maximise cash flow, returns and tax benefits. For example, some property owners opt for an interest only loan for their investment property, allowing them to focus on repaying both the principal and interest on their primary home loan.

Analysing Your Borrowing Capacity

Finding the best loan structure requires a careful analysis of a number of variables. Think about choosing between principal and interest loans and interest only loans, opening an offset account, what amount to borrow, and diversifying your lenders.

Considering Fixed or Variable Rates

The decision between fixed and variable interest repayment is important when designing your home loan. Variable rates may offer short-term benefits with potentially lower interest rates, but fixed rates offer stability and predictable repayments.

Seeking Financial Advice

It’s critical to understand that there isn’t a single, perfect loan structure. Your choice should be in line with your financial objectives, borrowing capacity, and personal circumstances.

Looking for trustworthy home loan advice? Book a FREE 15 min Call or Send Us Your Questions to Get the Right Help!