Without a crystal ball to predict fluctuating interest rates in Australia, you might be considering if now’s the best time to lock in your home loan rate whether you’re looking at applying for a new mortgage or refinancing your current one.

Jump straight to…

- Without a crystal ball to predict fluctuating interest rates in Australia, you might be considering if now’s the best time to lock in your home loan rate whether you’re looking at applying for a new mortgage or refinancing your current one.

- Who is a fixed-rate mortgage best suited for?

- Is it better to have a fixed or variable rate loan?

- What is the penalty for paying off fixed mortgages early?

As of July 2022, the Reserve Bank of Australia (RBA) has lifted interest rates for the third consecutive month, adding further pressure on borrowers to carefully weigh their interest rate options.

And that brings us to one of the most crucial phases in the home-buying process: Knowing if a fixed rate home loan is right for you.

Choosing the right type of interest rate could have a significant impact on your household budget and ability to pay back your loan whenever there’s an interest rate hike.

To help you decide if a fixed rate home loan is a good fit for your needs, this article aims to help you gain clarity on:

- The benefits and drawbacks of fixed rate loans

- How it differs from a variable rate home loan

- How to pay for a fixed rate mortgage, and if making extra payments and paying your existing home loan early is allowed by lenders

Let’s start with the basics – defining a fixed rate home loan, who it’s for, and its difference from a variable rate home loan.

A fixed rate home loan is a home loan with an interest rate that remains the same for the duration of the loan (or how long you need to pay it back).

The interest rate you pay for this loan type stays the same for a fixed rate period – usually from one to five years. Once fixed, the interest rate is not affected by changes in the market.

Who is a fixed-rate mortgage best suited for?

Fixed-rate mortgages, or fixed rate home loans, are attractive options for borrowers who:

- Seek certainty to avoid riding the interest rate roller coaster that may go up or down

- Want to know the monthly amount that their loan repayments will be (ie. interest repayments)

- Plan to keep their properties for a long time

Is it better to have a fixed or variable rate loan?

There is no right or wrong answer to this question. It all depends on your circumstances, financial goals, and needs.

ASK:

Are you looking for certainty to make your budget predictable?

OR

Are you looking for flexibility to make extra payments, refinance before the term is up, or pay off your home loan early?

While a variable rate home loan usually provides the flexibility to make additional payments and shorten the loan term by settling the loan earlier, the rise and fall of interest rate is dependent on the lender’s variable rates and the RBA’s cash rate.

When choosing the rate to pursue, one should also take the following into account:

1. Interest Rate Trends and Forecast

Locking in a fixed interest rate is typically ideal if you anticipate an increase in home loan interest rates in the short term, while a variable interest rate is advantageous if you believe that interest rates are going to decrease.

2. Loan Term

You may not have a crystal ball to foresee long-term economic conditions, but if you do not anticipate taking on a loan for an extended period, you may prudently consider short-term options for your decision.

3. Personal Income Forecast

The bottom line of choosing between fixed rate home loans and variable rate home loans is the desire for financial security. Assess your own financial condition, taking into account your job security, expected wage growth, and available savings.

After all things have been considered, it comes down to whether one is better for you given your unique situation and aspirations. Both home loan rates provide various benefits but the decision really comes down to how much certainty you want over your monthly repayments.

And since we already mentioned making extra payments, this brings us to the next question…

Can you pay extra on a fixed rate mortgage?

There is less flexibility when it comes to making additional payments because the interest rate and repayments are locked in for a certain time period in a fixed rate mortgage.

A lender may allow you to make early or additional payments, but you may be asked to pay a break cost. A break cost is also known as early repayment cost, break fee, exit fee, early repayment adjustment (ERA), early repayment fee (ERF), prepayment costs, and economic cost.

A Break Cost is the calculated amount of the loss which a lender incurs if a borrower decides to break a fixed interest rate loan contract with the lender. This loss is passed onto the borrower as a Break Cost.

Why do lenders charge a break cost?

When you, the borrower, opt for a fixed rate home loan, you and the lender enter into a contract to fix the interest rate on your loan for a specified period. A lender then enters into a contract with a third party to lock in its funding expenses at a fixed interest rate for the same duration as your loan agreement in order to fund your loan.

So, when you choose to break your loan agreement with the lender by switching or paying off your loan early (in part or in full) by going over your allotted number of extra payments, this ultimately compels the lender to also breach the third party’s funding agreement and they need financial compensation for this.

Can I pay off a fixed rate loan early?

Yes, most lenders allow this option but, like what has been explained when it comes to making extra payments, paying off a fixed rate loan early is essentially breaking a fixed period contract with the lender.

Therefore, the lender may ask you to pay a break cost to cover for the loss that the lender may incur by breaking their funding contract with the third party.

If the current wholesale interest rate for the remaining part of the fixed interest loan term is lower than the original wholesale interest rate for the fixed interest rate period, a break cost will typically be assessed.

An example:

If your rate is fixed for five years, the lender will borrow money at a fixed rate for five years from a third party to lend to you during that time.

Once you decide to pay back (in full or in part) the loan before the loan term expires, then the lender can only invest the money for the remaining term of the five-year-contract.

Assuming that there was a decline in interest rates, the lender can now only invest at a reduced rate, which results in a loss or expense that will be passed along to you as break costs.

What is the penalty for paying off fixed mortgages early?

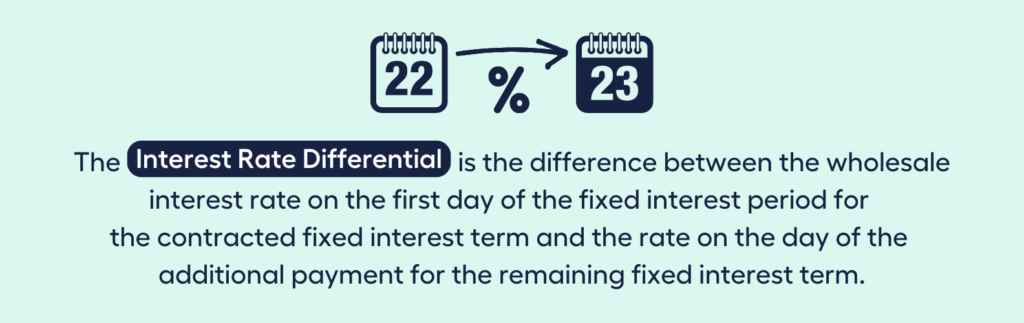

Each lender has their own way of calculating the fees they will charge you (this information should be included in your loan contract), but in general, lenders calculate the penalty (or the break cost) using the Interest Rate Differential.

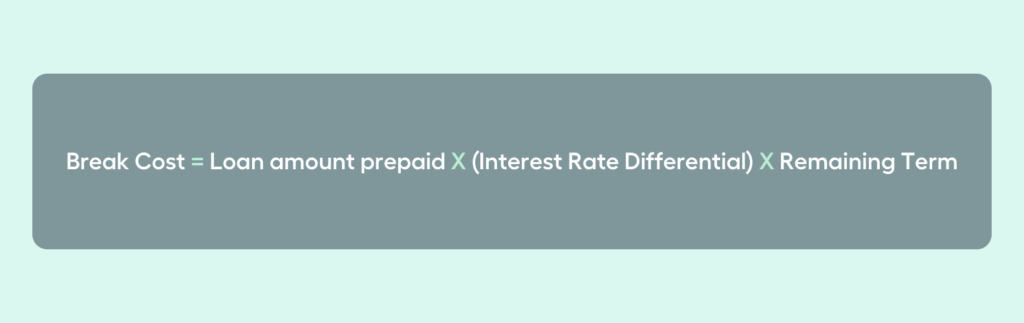

For example, the lender may use this Break Cost Formula:

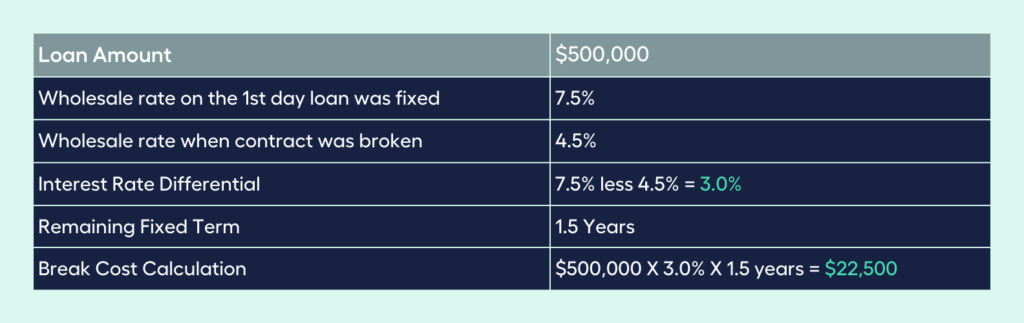

Sample Calculation:

Have you noticed that the loan term is taken into account in the calculation?

Due to this consideration, break costs are often particularly high for:

- Fixed loan terms that are 10 years or more

- Large loan amounts

Therefore, it is important to be cautious and enquire about how the break cost was determined and how much the wholesale interest rates have increased.

Some lenders may not be transparent about the process and may have earned a profit if the rates have risen at the time you paid off your loan early.

Advantages & Disadvantages of Choosing a Fixed Rate Home Loan

What is the advantage of a fixed rate mortgage?

The primary benefit of a fixed-rate loan is that it protects the borrower from abrupt, potentially sharp increases in their monthly mortgage payments if interest rates rise.

In general, it will be wiser to lock in your loan at a fixed rate if interest rates are currently low but on the verge of rising.

Here are some other key advantages of a fixed rate mortgage:

- Easier to budget because you know the exact repayment amounts

- Less stress from wondering if market rate changes will cause an increase in interest rates and repayments

What is the disadvantage of a fixed rate mortgage?

Key disadvantages of a fixed rate mortgage:

- Fixed rates do not decrease when market rates fall meaning you can’t take advantage of any lower payments if interest rates were to fall (as you can with a variable rate loan)

- Loans are less flexible when it comes to features like making additional repayments or paying your loan amount off early

- Fixed term fees or break costs may apply if borrower chooses to modify the terms, pay off the loan early or if they need to sell the house within the fixed rate period

You may view the effect of various rates, a comparison rate and loan terms on your monthly payments with our Repayment Calculator.

Understanding the key features of a fixed rate home loan, and the implications of making extra interest repayments and early loan repayment can help save you money and meet your financial goals.

However, one interest rate type is not necessarily better than the other. Some borrowers might find it more assuring to know that their fixed interest rate will take them on a steady cruise of predictable repayments, while others prefer the thrill of a possible rate fall, that could cause a decrease in repayments, provided by a variable interest rate.

Now that you know all the essential elements of a fixed home loan rate, do you think this is the type of interest rate for you?

You can take the first step:

Check Your Borrowing Power with MMS Mortgage Calculator

Knowing your borrowing power is just the first step. A mortgage is a big investment of both time and money, which is why It’s often best to receive guidance from a financial expert like a mortgage broker.

Many people may be unaware of this…but just like you, 41% of Aussies intend to get financial advice rather than going it alone, according to an Australian Securities and Investments Commission (ASIC) report.

Find the right Mortgage Broker for you with the help of My Money Sorted.

When you book a call with My Money Sorted, you’ll:

✓ get a better understanding of your financial options

✓ have an idea of the experts you can call on to help you reach your goals

✓ be matched with a mortgage broker who can help develop the best home loan strategy for your situation

My Money Sorted is your stress-free pathway to getting ahead with your home loan. Here’s what your journey will look like:

Step 1: Start off with a quick money matters session with My Money Sorted

Step 2: Get matched with a licensed Mortgage Broker that’s right for your financial situation

Step 3: Take the first step towards your financial goals with a clear roadmap that makes sense prepared by an experienced Mortgage Broker.

It’s that easy!