Are you now paying a fixed-rate mortgage and worried that it may increase by twofold soon?

If so, you might want to think about moving to a mortgage with a variable rate. Even though switching to a mortgage with a potentially variable interest rate may seem foolish, you may end up saving money over time.

The advantages of moving to a variable rate mortgage are discussed in this article, along with options on how to do so through refinancing. You will know how to pay less interest and maybe save thousands of dollars over the course of your mortgage once you’ve finished reading this article.

Jump straight to…

Fixed vs Variable Rates

There are many ways to structure a home loan. Some options include the type of payment and the type of interest rate. The repayment type can be ‘principal and interest repayments’ or ‘interest only’. Let’s look at the different kinds of interest rates and how they affect a home loan.

Your interest rate on a fixed-rate home loan is locked in for a certain duration of time, commonly anywhere from one and five years.

On the other hand, the interest rate on a variable interest rate home loan can change at any time, depending on what the lender decides – this is commonly influenced by interest rate changes implemented by the Reserve Bank of Australia.

Whether you choose a fixed rate or variable rate for a home loan depends on your own preferences. Let’s compare fixed and variable home loans to help you determine which is best for you.

Fixed Rates

When you apply for a fixed-rate home loan, your lender will likely give you a rate lock feature. This means that from the time you apply for your loan until the end of your fixed-rate period, the rate you are offered will not change.

A fixed-rate home loan is not for everyone and is not a one-size-fits-all solution for your home loan needs, but it does have its own benefits

Benefits of a Fixed Rate Home Loan

1. Fixed-rate mortgages give you peace of mind.

With fixed interest rates, you know exactly how much your weekly, fortnightly, or monthly repayments will be. This makes it easier to plan your budget and keep up with your repayments. You will pay the same amount until the end of the fixed rate period.

You can then choose to re-fix your loan, which lets you take advantage of your lender’s new fixed interest rate. Otherwise, the interest rate will revert to the applicable standard variable rate for the loan classification and repayment type.

2. You can better plan your budget with a fixed rate.

A fixed-rate home loan is great for first-time buyers who are on a tight budget, especially if they still have to pay for moving costs and home improvements.

3. With a fixed rate, you don’t have to worry about sudden rate hikes.

With a fixed-rate home loan, you can breathe a sigh of relief when interest rates go up because nothing changes with your home loan repayments.

When there are low interest rates, it makes a lot of sense to buyers to apply for a home loan. So, even if interest rates go up quickly, you can still take advantage of a low rate.

4. You can save a lot of money with a fixed-rate home loan.

With a fixed interest rate, you don’t have to worry about it going up. So you can save and use the money for other things without hurting your budget.

However, fixed-rate loans have their own problems, too.

Disadvantages of a Fixed Rate Home Loan

1. When you get a fixed-rate home loan product, you have a lot less freedom.

Since these loans are not affected by changes in the market, your repayments may be stuck at a higher rate than the average for the industry when interest rates go down.

2. Fixed-rate home loans may also have fewer features from some lenders.

Some lenders offer redraw facilities (some of which will also attract an additional charge) but they are not typically offered on a fixed rate home loan. With a redraw facility, you can use the extra repayments you paid on your home loan.

Note that home loans with a fixed rate can’t be linked to an offset account, which is a transaction account linked to your home loan account that offsets your interest payable. At the end of the fixed-rate period, the interest rate on your loan will revert to a variable rate. When this happens, you can consider whether opening an offset account is right for you.

3. Exit and switching fees for fixed-rate home loans tend to be higher.

If you stay with your lender but refinance to a loan with a better rate or more features, you could pay a switching fee.

When you choose to cancel a fixed term early and move to a different lender, your bank charges break costs, aka “early exit fees”.

High exit fees can make it hard for you to refinance your loan. To minimise break costs, try to refinance as late as possible or at the end of your fixed rate term.

Should I Fix My Mortgage for 2 or 5 Years?

Variable rates may be best if you have lots of savings. But if you can barely afford your loan repayments, it may not be worth the risk.

How long you fix your mortgage depends on your personal objectives and how long you require certainty.

A 2-year fixed-rate term may be best if you won’t stay in the property long. After 2 years, you can sell the property and leave. Or you can remortgage for another fixed-rate contract if you want to stay. You may even receive a better deal if interest rates have dropped.

A 5-year fixed-rate mortgage is a reasonable option if you don’t want to be trapped into a long-term contract but still want to know what your repayments will be while you build a cash reserve or work toward achieving your short and mid term goals. Additionally, 5-year rates typically aren’t substantially higher than 2-year rates. Thus, you could stay protected without spending much more.

Variables Rates

With a variable-rate home loan, your interest rate can change depending on the economy or the market. The RBA can change the cash rate, which can also cause interest rates to change.

2 Types of Variable Rates

Standard variable rate home loans give you flexibility and usually come with extra features like offset accounts, redraw facilities, and the ability to split your loan.

Or you could get a basic variable rate, which usually has a lower interest rate but doesn’t have extra features like an offset account.

Knowing the pros and cons of a variable home loan rate product and how to manage it to meet your needs is crucial because interest rates affect how much you’ll pay over the life of your loan.

Benefits of a Variable Rate Home Loan

1. Variable-rate loans give you more ways to pay back your loan.

You can pay off your loan faster without having to pay interest rate break costs. Some variable-rate loans also have features like offset accounts or redraw facilities that help you pay less interest on your loan balance while still giving you access to any extra money.

2. It’s easier to refinance an existing home loan.

If you’re on a variable rate, switching to a different financial institution or home loan product may be easier if you find a better offer elsewhere since you don’t have to pay break costs.

3. If rates go down, you may pay less.

Rates can go down for a number of reasons, but mostly because the cost of borrowing money has gone down. If you are on a variable rate, this means that your repayments will go down.

4. You can reduce the interest amount.

By using your offset and redraw facilities offered in variable home loans, you can lower the amount of interest you have to pay back over the life of the loan.

Disadvantages of a Variable Rate Home Loan

1. You may stand to pay more if rates rise.

Lenders can raise variable interest rates at any time, increasing your costs. Borrowers’ rates may change over the loan’s duration. Repayments climb if your bank raises rates.

To avoid mortgage stress if variable rates climb, include a buffer in your home loan.

2. There’s the risk of cash flow uncertainty.

Variable rate borrowers will have trouble predicting long-term cash flow because rates might vary at any time. Variable loans necessitate borrower flexibility. If cash flow issues emerge, loan features like offsets and redraw facilities might help.

Is It Better to Go With a Fixed or Variable Rate?

One of the most important decisions to make about your home loan is whether you want a fixed or variable interest rate. When choosing the type of loan interest rate, borrowers need to think about their own needs and personal financial circumstances.

The rate you choose may depend on what you want to use the loan for.

Fixed-rate loans can be good for property investors who don’t want to pay off their investment home loans faster and like how simple and predictable fixed payments are.

Borrowers who want to refinance, renovate, or sell their property might choose a variable rate so they can remain flexible when the time comes to make a move.

Do you want to check which repayment scheme suits your budget and in which home loan type you can save the most?

You can use the MMS Loan Comparison Calculator to find the best scheme for you.

Remember, whether you choose a fixed rate or a variable rate, it’s important to read the loan product’s terms and conditions carefully.

Can I Change My Mortgage From a Fixed to Variable Rate Mortgage?

YES, you can change your mortgage from a fixed rate to a variable rate anytime, although doing so before the fixed rate term ends will cost you money.

Here’s why:

Your lender frequently obtains money from wholesale money market banks to pay for your home loan. A fixed-rate home loan locks in the lender’s funding costs to mitigate interest rate risk.

If you break your fixed rate period early, your lender must continue to pay the wholesale money market. If they lose money, lenders will levy a fixed rate break cost along with other fees.

You can find out more about fixed rate break costs in your home loan contract and the terms and conditions that come with your loan. Or you can talk to a home lending specialist to get an idea of how much it will cost to break a fixed-rate loan.

Refinancing Your Mortgage

Refinancing involves switching mortgage lenders to get a new home loan. Your new financial institution’s lending criteria apply for the approval of your new mortgage.

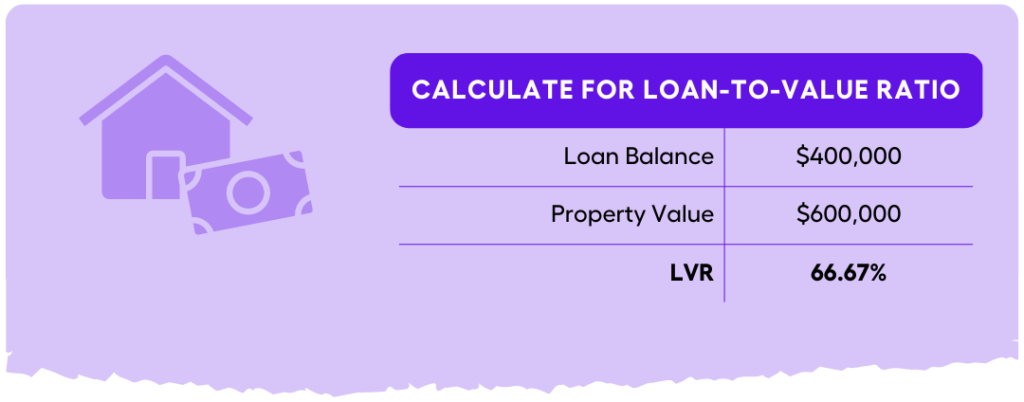

Loan-to-value ratio (LVR) is one of the criteria used by lenders to assess your risk. The lower your LVR, the ‘safer’ you are as a borrower.

LVR shows how much your home loan is worth as a percentage of the value of your home. Divide the loan balance by the value of the property to get the LVR.

For example, a loan balance of $400,000 is divided by the property value of $600,000 to get an LVR of 66.67%, which is considered a low LVR.

Note: An LVR of less than 80% is considered low

When refinancing, you repeat the loan application process with a few extra steps. Because many lenders only provide their lowest rates to new customers, you may save more by filling out more paperwork.

Refinancing can increase your options and save you money.

Broker vs Banks

You can get a home loan from a bank, but keep in mind that they don’t have access to as many options as mortgage brokers do.

And if you work for yourself or if your income changes often, banks may be less likely to offer you a favourable interest rate.

It’s hard to find the best bank home loan deal because of these two things.

With the help of an experienced mortgage broker with an Australian Credit Licence (or an authorised representative of a licence), you may have a better chance of getting a home loan at a good or comparable interest rate, even if you:

- do not have a very good credit score

- are self-employed

- have a variable income

- have been turned down before

- seeking a big loan

Mortgage brokers give independent advice and are required by law to act in your best interest. In fact, if mortgage brokers don’t do what’s best for their clients, the federal government can fine them more than $1 million.

The best part is that you don’t have to pay a mortgage broker any of your hard-earned cash because banks pay mortgage brokers a commission for bringing in business.

All of these points have increased the likelihood of Australians using the services of a mortgage broker. According to the most recent Mortgage & Finance Association of Australia (MFAA) data, more than 2 out of 3 current Aussie home loan borrowers are served by mortgage brokers.

Questions to Ask When Refinancing

Refinancing is a step in the right direction for many borrowers who want to take advantage of market conditions.

Here are 10 questions you need to ask your broker about refinancing if you plan to talk to him or her about it:

- Is it a good idea for me to refinance?

- How is the process of refinancing going to work?

- How much does refinancing cost?

- How quickly can I get a new loan?

- Should I refinance with the same lender I have now?

- What kinds of loan features can I get if I refinance?

- I have existing loans. Should I refinance in order to consolidate them?

- Will I be able to access my home’s equity?

- Should I get a mortgage with a fixed rate or one with a variable rate?

- When I refinance my loan, are there any restrictions?

- For homeowners wishing to reduce their interest payments, switching from a fixed-rate to a variable-rate mortgage can be worth considering.

You also need to consider more than interest rates when refinancing a home loan by looking at the big picture since a mortgage is a long-term commitment.

Although the prospect of an increase in interest rates can be unsettling, those who can tolerate the risk may find that a variable-rate mortgage’s total cost savings and flexibility make it worthwhile.

As with any financial choice, it’s crucial to thoroughly weigh the advantages and disadvantages and, if necessary, seek the help of a finance expert. You might possibly save tens of thousands of dollars over the course of your mortgage if you take the time to carefully consider your alternatives and make a well-informed choice.

Many people may be unaware of this…but just like you, 41% of Aussies intend to get financial advice rather than going it alone, according to an Australian Securities and Investments Commission (ASIC) report.

Don’t Let Interest Rates Get You Down – Discover Refinancing Options When You Book a FREE 15 min Call or Send Us Your Questions.