Deciding whether to invest in property or buy your own place can be like trying to navigate a maze blindfolded.

On one hand, if you pick the right property, you could potentially make a killing with tax perks, rental income, and capital gains. But on the other hand, owning your own home offers security and a sense of belonging, not to mention the opportunity to create your own dream home.

Let’s face it, the Australian property market is probably one of the most cutthroat in the world. So, before you make a move, you need to weigh the pros and cons of each option.

In this post, we’ll discuss the key differences between an investment property and your very own home, so you can make an informed decision based on your specific needs.

Jump straight to…

What Does PPOR Mean?

Your main residence or dwelling is your principal place of residence (PPOR) and it is exempt from capital gains tax. Anything used exclusively or mostly for residential housing is referred to as a dwelling, such as a house, a townhouse or villa, a strata title apartment, a villa in a retirement village, a caravan, a houseboat or other mobile home.

Dwellings are exempt from Capital Gains Tax (CGT)

Dwellings, when sold, are exempt from Capital Gains Tax (CGT). This should be easy to understand, with 67% of Australian homeowners owning and residing in their home.

However, for property investors, there are other tax implications when they own not only a residential home but also an investment property, which may be rented to a tenant.

Let’s talk about how to qualify a property as a PPOR.

Criteria to Qualify as a Principal Place of Residence

Your dwelling is regarded as your principal place of residence (PPOR) or main residence by the Australian Taxation Office (ATO) if:

- You and your family live there.

- It contains your personal belongings.

- It is the address where your mail is delivered.

- It is your address on the electoral roll.

- Services such as gas and power are connected.

If your property increases in value, you will benefit from a capital gain when you sell. But understand that when you sell an asset, capital gains tax (CGT) may eat away a big chunk of your profits, depending on your income level.

Despite being known as “capital gains tax,” it is actually a component of your income tax. It is not a separate tax. Your tax obligation will go up if you have a capital gain.

Let’s talk about proving a property as a PPOR and what that means for investors.

How Do I Prove My Principal Place of Residence in Australia?

Now let’s check if your main residence or dwelling qualifies for capital gains tax (CGT) exemption.

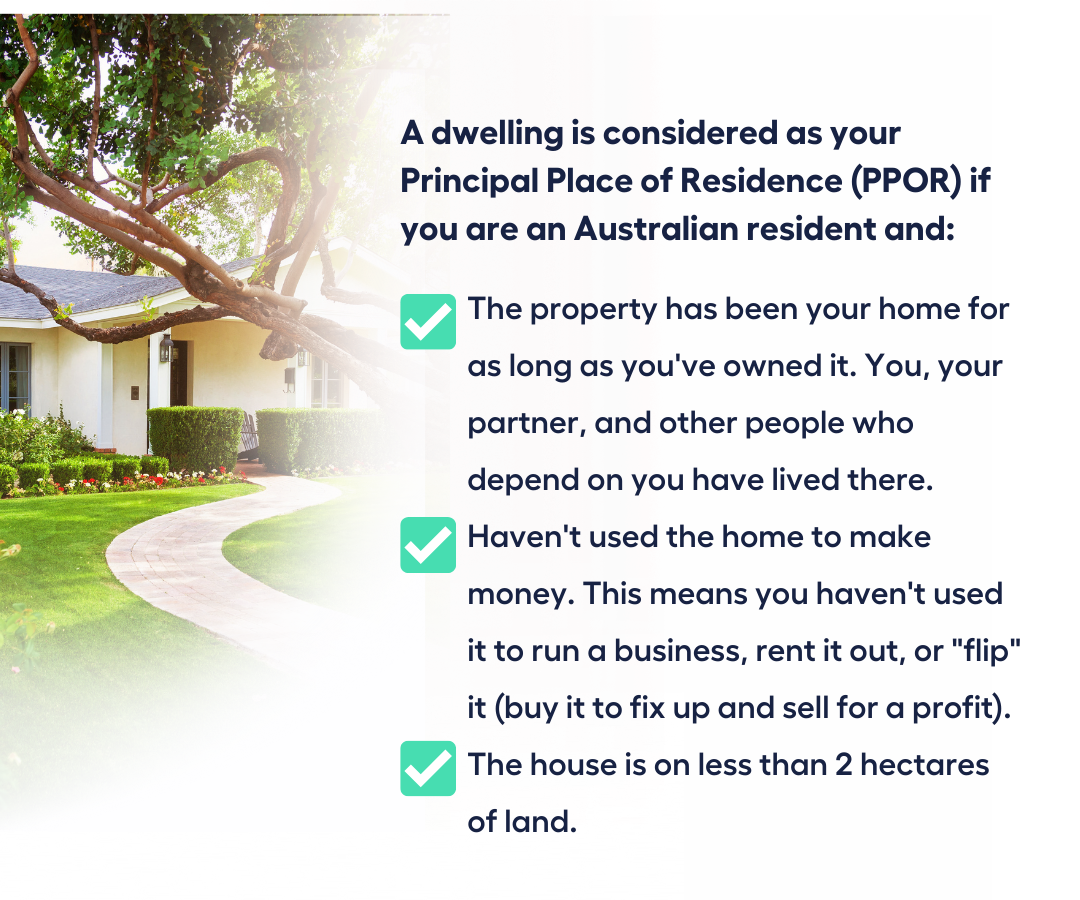

You do not pay capital gains tax when you sell your current home and you can ignore any capital loss if you meet all of these conditions:

- You are an Australian resident and the property has been your home for as long as you’ve owned it. You, your partner, and other people who depend on you have lived there.

- You are an Australian resident and haven’t used the home to make money. This means you haven’t used it to run a business, rent it out, or “flip” it (buy it to fix up and sell for a profit).

- You are an Australian resident and the house is on less than 2 hectares of land.

You can still be eligible for a partial exemption even if you don’t meet all of these requirements. You can calculate the proportion that is exempt using the CGT property exemption tool.

You do not qualify for the full primary residence exemption from CGT if you rent out a portion of your house or operate a business out of your house.

The portion of your home you used to rent out or operate a business is subject to CGT when you sell it.

Why?

Because you can typically claim a deduction for that portion of your home when filing your income tax return, and for the fiscal years you earn from it.

To determine your assessable capital gain or loss, you consider:

- the percentage of the floor area designated for rental or business

- the period you used it for rental or business

- the increase or decrease in property value of your home since you first began renting it out or doing business there (presuming that this occurred after August 20, 1996).

You can continue to treat your old home as your primary residence for up to 6 years if you move out and rent it out. However, for the same time period, you are not permitted to claim a main home exemption for any other property.

How Many Times Can You Claim Main Residence Exemption?

Only one residence may be listed as your “main” residence at any given time. This means you can claim main residence exemption on any qualified principal place of residence.

For example:

You want to sell home no.1 because your family is growing and you need to buy home no.2. You can claim CGT exemption on house no.1 when you sell it.

Home no.2 is eligible for the primary residence exemption for CGT purposes as soon as you purchase it, as long as you move in as soon as is practical. When buying a home, the “date of acquisition” is the settlement date of the contract.

Should you wish to sell home no.2 in the future because you want to downsize to home no.3, you can claim CGT exemption on house no.2 when you sell it. And home no.3 becomes eligible for the primary residence exemption for CGT purposes on its acquisition date.

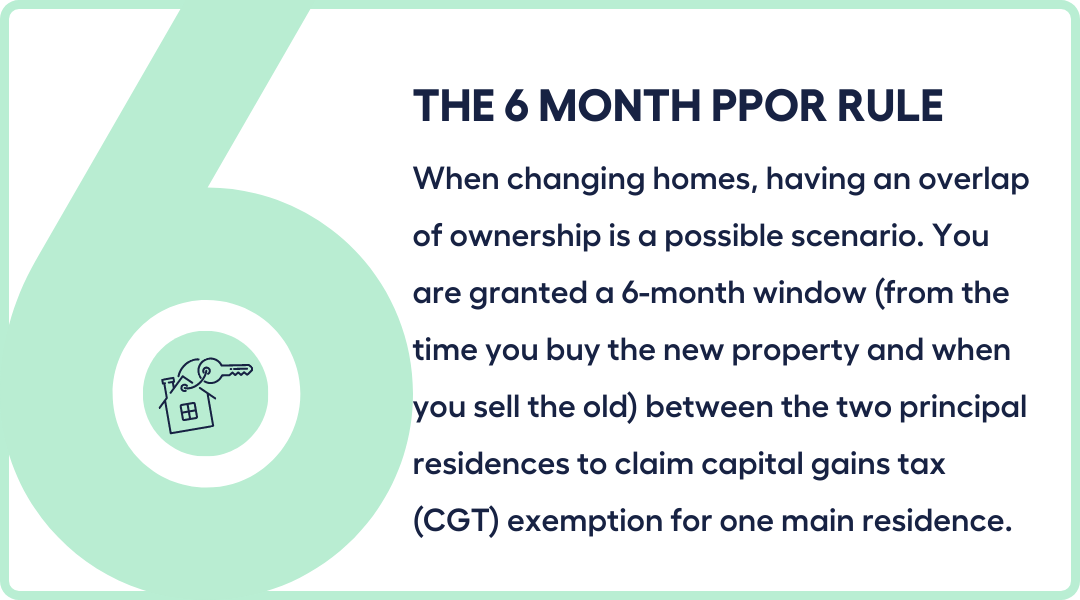

Overlap of ownership when changing homes

The 6 Month PPOR Rule

In the example above, you can’t avoid having an overlap of ownership for the short term when changing homes. In such a scenario, you are granted a six-month window (from the time you buy the new property and when you sell the old) between the two principal residences.

You can treat both as your primary residence for up to 6 months if each of the following is true:

- You continuously occupied your previous home as your primary residence for at least three months in the 12 months prior to selling it.

- When it wasn’t your primary residence for any portion of those 12 months, you didn’t use your former house to earn money (like rent).

- Your new home becomes your primary dwelling.

The main residence exemption only applies to both properties for the final six months before you sell your previous home if it takes you longer than six months to sell it.

Prior to this, throughout the time that you owned both properties, you may designate one as your primary residence. The other will be charged CGT at that time.

Can You Have 2 Principal Residences in Australia?

The 6-month rule is the only scenario where you can have 2 principal residences for CGT purposes, because typically, a house ceases to be your primary residence the moment you stop residing there.

However, there are instances where you can continue to treat a property as your primary residence for CGT purposes and still be exempt from CGT after you stop residing there, as long as you regard the home as your primary residence:

- For up to 6 years if it’s used to produce income, such as rent (sometimes called the ‘6-year rule’)

- Indefinitely if it is not used to produce income.

During this period after you stop living in the property but continue to treat it as your principal place of residence:

- It is still exempt from CGT (just as if you were still living there, even if you start renting it out after you leave).

- You cannot treat any other property as your primary residence (except for up to 6 months if you are moving).

To be eligible, the property must have been your main residence first and you stopped living in it.

Scenarios when you have 2 Primary Residences and still be exempt from Capital Gains Tax (CGT)

Primary Property is used to generate income

You can continue to treat a property as your primary residence for CGT purposes for up to 6 years if it is used to generate income, such as rent. This is known as the 6-year rule.

If you’re absent more than once while owning the property, the 6-year period applies to each absence. A period of absence ends when you stop renting your home and either move back in or leave it vacant.

Primary Property is NOT used to generate income

You can also treat a property as your primary residence for CGT purposes indefinitely if it is not used to produce income, such as a vacation home.

You can also use the main residence exemption if you live in a different home to your spouse or children.

A home different from your dependent child

If you and a dependent child under the age of 18 live in separate residences for a time period, you must designate one of those residences as your main residence for that time period for CGT purposes.

A different home from your spouse

For CGT purposes, if you and your spouse have different homes for a certain amount of time, you and your spouse must either:

- Choose one of the homes as the main residence for both of you during that time, or

- Each choose one of the different homes as your main residence for that time.

If you propose different residences for the period and own 50% or less of the nominated home, you are eligible for an exemption for your share.

If you own more than 50%, your share is exempt for half the period that you and your spouse live in different houses. The same applies for your spouse.

This rule applies to each spouse’s main dwelling, regardless of ownership.

Your spouse is another person who is:

- legally married to you

- in a relationship with you and that relationship is registered under a state or territory law, or

- living with you in a committed domestic partnership even though you are not legally married.

Investment Property vs PPOR

So, you’re saving for a deposit because you dream of owning a property.

But which should you purchase first, a home for your family or an investment property?

Depending on your personal circumstances and the property you’re considering buying, you’ll have to decide which to buy first—an owner-occupied property or an investment property. Think about your financing options, such as fixed or variable-rate home loans, for investment purposes.

Investment Property or Permanent Residence

House with Money vs House with Family

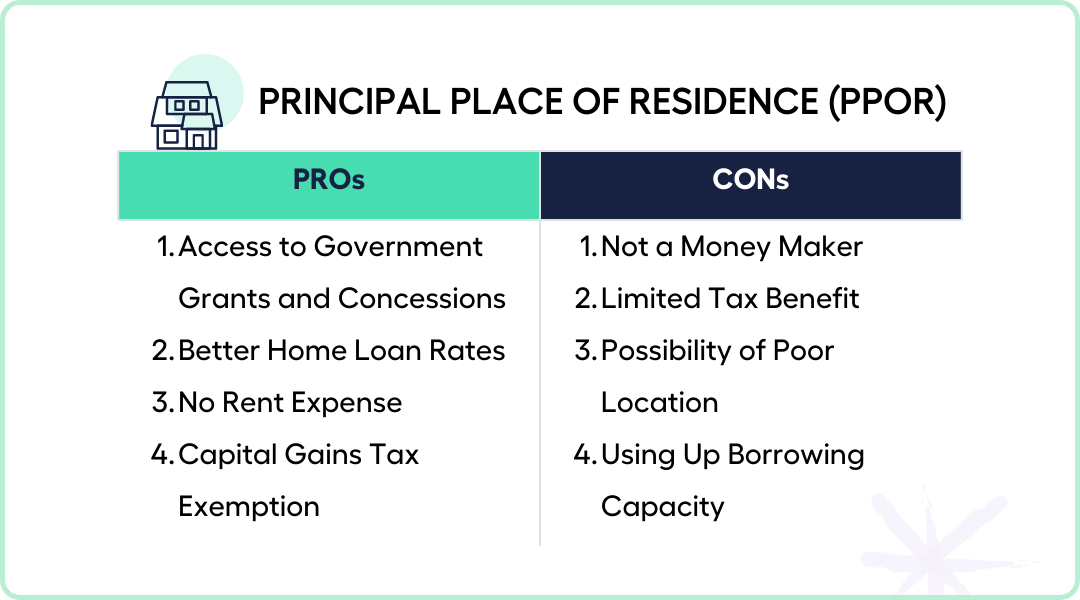

PPOR Pros

Let’s have a look at the advantages of buying a principal place of residence first.

1

Government Grants and Concessions

You may be eligible for government grants for first-time home buyers, especially if you buy off the plan or a new build house.

Many states provide large first-time homebuyer grants and tax breaks on land, which can assist to lower the price of buying a home.

To be eligible for the grant, a homeowner must typically live in the property for 6 to 12 months, depending on the locality.

2

Better Home Loan Rates

Lenders will provide you more flexible loan terms, better interest rates, and discount periods than they would if you were a real estate investor.

Owner-occupier mortgage loans are frequently less expensive in terms of interest rates and other closing charges, such the appraisal fee.

3

No Rent

Instead of subsidising someone else’s goals by renting, the money you spend goes towards building your own long-term wealth.

When you own your house, you are also not subject to the whims of a landlord. Plus, you and your family will enjoy the security and comfort of familiarity by remaining where you are.

4

Capital Gains Tax Exemption

If and when you decide to sell your PPOR, you will not be subject to capital gains tax, which is a significant benefit if you plan to hold the asset during several growth cycles.

PPOR Cons

Like all investments, buying a principal place of residence first has its disadvantages.

1

Not a Money Maker

Only when you sell your property will you get a return on your investment, that is if you hold onto the property over several growth cycles.

Until then, you’re making home loan repayments to live in your property. It’s a money taker not a money maker.

2

Limited Tax Benefit

Aside from the CGT exemption, a PPOR provides no additional tax deductions or benefits.

3

Poor Location

Your location will be determined by your first-time home buyer budget, and you may not be able to live where you really want to—close to work, near friends or recreational activities.

This is one reason why some people buy rental properties in places where they can afford them and then rent a home (that’s less expensive than mortgage payments) in their dream neighbourhood.

4

Using Up Borrowing Power

If you do get to live in your dream neighbourhood, you may end up exhausting your entire borrowing power.

It may take some time to build up enough of a buffer to borrow money for investment or other purposes. Being stretched in this way might also lead to financial strain.

Investment Property Pros

Now let’s have a look at the advantages of buying an investment property first.

1

Rental Income

Unlike a primary residence, an income-producing property may pay for itself, especially if it is positively geared – that is its income exceeds property expenses.

2

Tax Benefits

An investment property allows you to claim tax deductions that can considerably lower your tax liability.

Negative gearing: Your investment property is negatively geared if the net rental income is less than your mortgage payments. In this case you may be able to deduct the full amount of your rental expenses from your rental income, salary and other income.

Rental Expenses: For capital works, asset depreciation, and borrowing costs, you typically have a number of years to claim a deduction. These costs include:

- Borrowing costs: the costs of taking out a loan to buy a home.

- Capital expenditure: the costs of building construction as well as structural renovations and additions.

- Improvements: anything that improves, increases the value of, or changes the character of the item on which work is being performed.

- Depreciating assets: such as carpets, drapes, appliances such as a washing machine or refrigerator, and furniture.

- Initial repairs: costs incurred to correct defects, damage, or degradation that existed when you purchased the property.

- Capital works: expenses incurred in the construction of the property as well as structural modifications, alterations, and extensions to the property.

Management and Maintenance Costs: You can deduct expenses related to the management and maintenance of your rental property, including interest on loans, in the tax year in which you incur them.

Expenses that may be eligible for an instant deduction in the tax year in which they are incurred include:

- advertising for tenants

- body corporate fees and charges

- council rates

- water charges

- land tax

- cleaning

- gardening and lawn mowing

- pest control

- insurance (building, contents, public liability, loss of rent)

- interest expenses

- prepaid expenses

- property agent’s fees and commission

- repairs and maintenance

- legal expenses.

3

Business Decision

An investment property allows you more flexible buying criteria. You can make your decision entirely on financial considerations, without the emotional attachment of having to buy something you actually want to live in.

Thus, there’s a better chance of buying a property that fits your budget and pays for itself.

4

Grow Wealth

If your investment property is located where there is strong rental demand and provides good rental returns and you can rent where you wish to reside for less than a PPOR in that region would cost to buy, your borrowing power will be less constrained.

Using rental income, you can either increase your mortgage payment to increase equity in your home or use your cash flow to fund other investments.

Investment Property Cons

Buying an investment property first also has its disadvantages.

1

No First Homeowner Grants & Concessions

If you buy the property as an investment, you will not be eligible to take advantage of the first homeowner grant and concessions.

This also means that you may never be able to take advantage of these benefits because you will have previously purchased a property—the ‘first’ home owner criterion is no longer relevant.

2

No Capital Gains Tax Exemption

With investment properties, like apartments, you are liable to pay tax when sold, which is difficult to accept if your investment plan is to invest for capital growth!

3

Having a Landlord

If you buy an investment property first and rent a home, you will be subject to the whims of your landlord, lease agreements, and strata restrictions. You may have difficulty finding a property that permits pets or meets your other requirements.

Final Thoughts: Which is the Best Money Move?

There are at least 3 factors that will influence your decision to purchase a PPOR or an investment property first:

- Is there a personal/non-financial reason for you to own a PPOR?

- Is there a significant cost difference between buying and renting a PPOR?

- What is the deposit amount?

If there is no emotional/non-financial motivation for purchasing a PPOR, the primary consideration will be whether the cost of renting is less than the cost of the mortgage and holding costs of home ownership (maintenance, insurance, council rates).

Another issue that can sway the argument is the overall amount of money available for a deposit. The more cash available for a deposit, the more likely it is that purchasing a PPOR is more financially advantageous than purchasing an investment property.

Because you can re-leverage a PPOR with a debt recycling approach to swiftly create an investment portfolio – this biases PPORs in the long run because you can reduce your effective PPOR continuing costs while having a growing deposit base for investments.

Trying to Decide Between Investing in Property and Buying a Home? Book a FREE 15 min Call or Send Us Your Questions!