What qualities do you look for in a lifelong partner?

Whatever the qualities are, it might not be wise to jump and commit to the first person you meet. After all, we’re talking about a long term relationship.

Getting a mortgage is similar in many ways:

A home loan is a long term financial obligation that can last 30 years, and it’s probably going to be the biggest debt you’ll ever have.

Jump straight to…

You’ll want the best deal for your home loan because securing a loan with an interest rate even a fraction of a percent lower can save you thousands over 30 years.

And this brings us to a commonly asked question:

Between a bank and a mortgage broker, who would you pick to give you the best deal on a 30-year debt?

In this article, we’ll discuss these two options to help you decide which one you should use for mortgage advice — a bank or a broker?

Mortgage Broker vs Banks

Paying off your mortgage requires spending a large amount of time and money.

Would you rather leave your search for the best deal to chance or would you consider getting the help of home loan specialists like mortgage brokers and loan officers?

A specialist who isn’t only familiar with the home loan application process, but one who is committed to getting the best home loan deal for their clients.

A mortgage broker and a bank loan officer will both ask you questions about your financial situation and assist you in filling out and submitting a mortgage application.

However, their duties are significantly different in other aspects.

- A loan officer works for a bank, credit union, or other mortgage lender and will only offer the products and mortgage rates of the financial institution they work for. Quite often too, a loan officer handles other loan products such as personal loans and credit cards.

- A mortgage broker works on behalf of a borrower to find the lowest rate and best home loan deal from a variety of lending companies. A mortgage broker typically isn’t licensed to handle other loan products such as personal loans and credit cards.

| Mortgage Broker vs Bank Loan Officer | |

| Mortgage Brokers | Bank Loan Officers |

| Works on behalf of a borrower | Works for a lending institution |

| Offers products from various lenders | Offers products from lending company that employs them |

| Looks for the best rates in the market | Provides the best rates in their product list |

| Deals only with mortgages | May handle other loan products |

At first glance, a mortgage broker would seem to be a better choice. But let’s have a closer look before we decide.

What is a Mortgage Broker?

A mortgage broker acts as an intermediary between a prospective borrower and banks and other lenders, and assists the borrower to apply for and secure a home loan.

Mortgage brokers have an obligation to act in your best interests when advising you to take out a loan.

A qualified mortgage broker will ask information from you in order to:

- Determine how much you can comfortably borrow

- Look for choices that will work for you

- Describe the terms and costs of each loan, including the interest rate, features, and fees

- Make a loan application and see it through to settlement

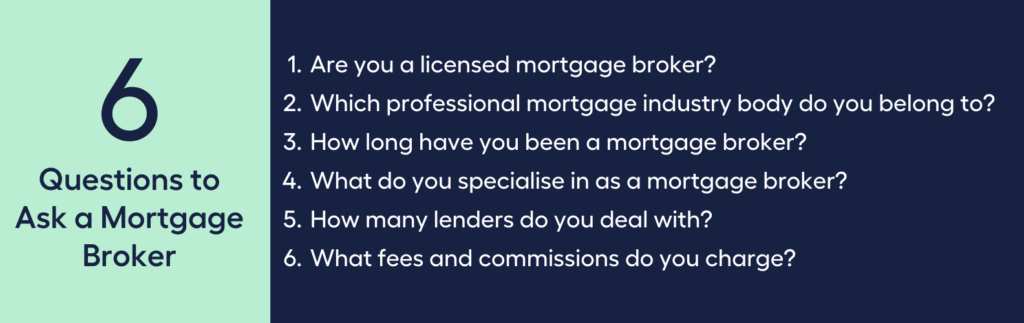

But asking questions and providing information isn’t a one way street. You can ask brokers some key questions to make sure the broker is a good fit for you.

It’s important for you to find out if a broker is a licensed mortgage broker and a member of a professional mortgage industry body like the Mortgage and Finance Association of Australia (MFAA) or the Finance Brokers Association of Australia (FBAA).

You should also know how long the mortgage broker has been in the industry and their specialisation, such as first home buyer loans, refinancing, and investment property loans among others.

Find out if the mortgage broker can offer you different home loans from a large number of Australian lenders, and what fees and commissions they may charge.

Having this exchange of information during your first meeting will help you find the best broker for your needs.

What is the Difference Between Banks and Mortgage Brokers?

Both banks and mortgage brokers aim to provide a home loan to a customer.

Here’s where the difference lies:

How they serve their customers.

How they serve YOU.

Mortgage brokers are obligated to work in their clients best interests as mandated by the Royal Commission recommendations for mortgage brokers.

Banks and other lenders, on the other hand, are not covered by the best interest duty.

Because brokers work in your best interest and banks don’t have to, this means that brokers work for you, banks don’t.

- A broker will educate you about fees, charges, and due dates among others.

- A broker will remind you that your repayment starts one month from the date of settlement of your home loan for a monthly repayment, or 15 days after settlement for fortnightly repayments.

- Part of a broker’s service often includes revisiting your home loan rates every year with different comparison rates to check if you need to refinance your home loan for a better deal.

In the process, a broker will also let you know that you have to pay early repayment fees if you make extra repayments on your home loan greater than what the lender allows, or pay off the whole loan early.

More than simply giving you an interest rate update, your broker can also teach you the pros and cons of principal and interest repayments.

And advise you when to go with a fixed rate or when to stick with a variable rate. Educate you on the various fees and charges that come with a home loan.

Licensed brokers can and will provide you all these because they work in your best interest.

Is it Better to Use a Mortgage Broker or Go Straight to the Bank?

Depending on your financial situation and personal circumstances, one may be better than the other.

Someone with a good credit score may make a different decision than someone with a poor credit score.

The trick is to obtain home loan quotes from both providers and compare offers and turnaround times for underwriting, appraisal, and loan processing from start to finish. The differences might surprise you.

Homebuyers who compare quotes from at least three lenders before selecting an underwriter frequently get the best for a home loan.

Home Loan Comparison Tip:

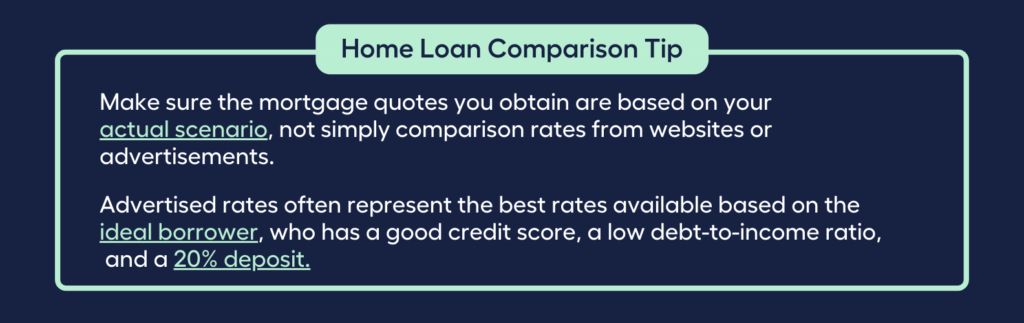

- Make sure the mortgage quotes you obtain are based on your actual scenario, not simply comparison rates from websites or advertisements. Advertised rates often represent the best rates available based on the ideal borrower, who has a good credit score, a low debt-to-income ratio, and a 20% deposit.

Mortgage lenders will need the following information to provide you with an accurate quote:

- The location of the property

- The property’s value

- Your loan amount and deposit

- Your credit score

Based on the information you supply, lenders can usually provide you with a rate quote in a matter of minutes.

Which is Easier to Get a Home Loan Through?

The ease of getting through a home loan process depends mostly on the borrower’s situation.

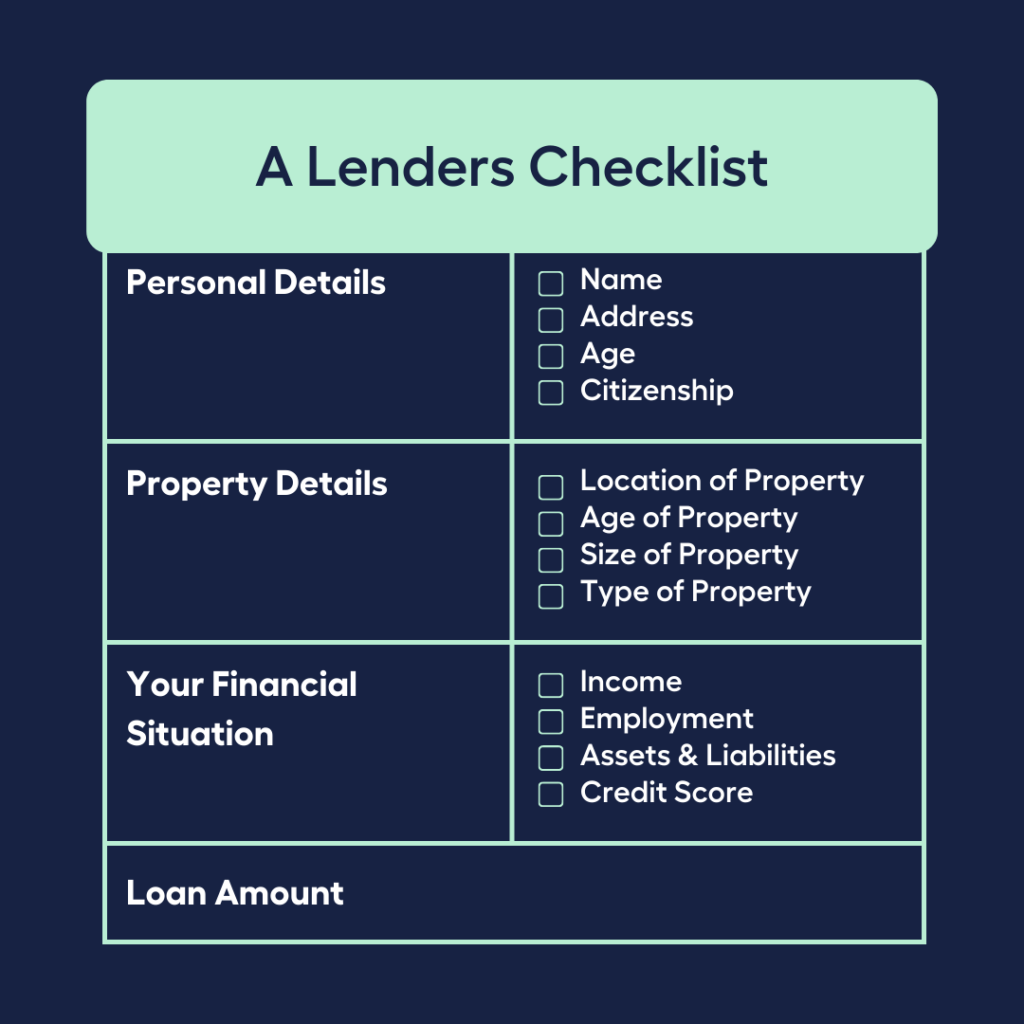

A lender will look at different factors to ensure your home loan eligibility. Different lenders may have different requirements for home loans, but you can usually count on them to ask for some basic information.

Personal Details

Your personal details include information such as name, address, citizenship, and age. Age and health are of special significance as the lender needs to ensure that you will be able to repay your loan throughout its loan term.

Property Details

Information about the property includes the property value, location, age, size, and type (house, unit, etc.). Some lenders impose limitations on the kind of properties they would accept as collateral for loans.

Your Financial Situation

Lenders must guarantee that a mortgage is appropriate for the borrower. They will evaluate a number of indicators to determine your financial position, including your income, employment, assets and liabilities, and credit score.

Loan Amount

The lender will often take into account how much you need to borrow in relation to the value of the property. This affects the loan-to-value ratio (LVR), the possibility of having to pay lenders mortgage insurance (LMI), and your ability to pay back your mortgage.

If you tick all the boxes included in the lending criteria, you’ll probably have an easy time getting a loan whether you get a mortgage broker or go directly to a bank.

However, if you don’t check all the boxes, it might be worth considering getting the services of a mortgage broker to help get the loan approval you need.

A first time home buyer will likely benefit from a mortgage broker as well, as a broker knows how to navigate the application process and assist in the home buying journey.

That being said, as a borrower, you can always check comparison sites to see if your bank or broker is providing you the best rates.

It is in your best interest to compare rates since you’re getting into a long term debt, and every percentage point lower can save you thousands over the loan period.

Which Can Secure Better Rates?

As mentioned earlier, mortgage brokers are obligated to find the best deal for their clients, while banks and lending institutions are not.

To set things straight:

Banks do offer good interest rates, they just don’t offer it to everybody.

So, who gets offered competitive interest rates by banks?

Banks give better interest rates to low-risk borrowers, such as those with a strong credit history, a good deposit, and a stable income.

Banks often compete with each other for new customers to increase their business, subsequently, banks offer better rates to new customers than their existing customers.

Banks want the business a broker brings and will fight hard for it because a mortgage broker can walk out the door to look for a better deal for their customer.

And why so?

A good mortgage broker has access to many different types of loan products from different lenders, and only applies with a lender they expect will approve your loan.

A mortgage broker works for you, and they will use their credit knowledge to present your home loan application highlighting the strengths in your home loan application.

Rest assured, all licenced mortgage brokers must not provide a home loan recommendation that will leave you in a worse off position as stipulated in the National Consumer Credit Protection Act (NCCP Act).

Which Is Better for Refinancing?

As a homeowner, remember to practise prudence when accepting the initial refinance rate provided by a lender. This is especially true if you’re submitting an application through your current lender.

If the refinance home loan terms, interest rates, and fees are the same across both your existing lender and a new lender, refinancing with your current lender could have two significant advantages:

Cost savings and convenience.

1

You may be able to save money

Refinancing a home loan, like your initial mortgage, has charges. Settlement fees typically range from 2% to 5% of the total amount borrowed, or around $5,000 on average.

However, if your lender already has an appraisal report, title information, and a mortgage insurance policy on your home, you may get fee waivers or save on certain expenses.

You could save money on the following expenses:

- Fee for title insurance

- Mortgage insurance premium

- Fee for loan origination

- Fee for home appraisal

2

It may be faster and easier

Considering that you already have a relationship with your current lender, refinancing with them may be simpler. The lender already has your financial information and payment history on file, so it might be able to speed up some of the paperwork needed for a refinance.

Additionally, keeping everything under one roof may be more effective if the bank or credit union you use for your personal banking also underwrites your home loan.

Conclusion: Is a Broker or Bank Better?

There is no right or wrong answer when it comes to choosing between a bank and a broker since the choice is highly dependent on your financial situation and knowledge about home loans.

If you’re financially stable and knowledgeable enough about home loans, interest rates, finance options, and comparison rates, it’s likely you’ll always get a good deal and get the right loan.

On the other hand, a mortgage broker may be suitable for you if you’re not particularly knowledgeable with loan options, not confident with your finances, a first time home buyer, or don’t have the time to compare loans and shop for a credit provider.

What’s important is to always be on the lookout for a better deal for yourself. You wouldn’t want to get tied down to a high interest rate if there is a better rate available, at the same time you wouldn’t want to get caught with fees and charges you were never aware of.If you need more information about securing the best deal on your home loan, talk to My Money Sorted for free!

Many people may be unaware of this…but just like you, 41% of Aussies intend to get financial advice rather than going it alone, according to an Australian Securities and Investments Commission (ASIC) report.

Find the right Mortgage Broker for you with the help of My Money Sorted

When you book a call with MMS, you’ll:

✓ get a better understanding of your home loan options

✓ have an idea of the experts you can call on to help you reach your goals

✓ be matched with a mortgage broker who can help develop the best home loan strategy for your situation

My Money Sorted is your stress-free pathway to getting ahead with your home loan.

Curious what happens during a call with My Money Sorted?

Watch this video!

It’s that easy!

In the Market for a Mortgage? Chat with Us Today.