You thought getting a home loan was going to be tough but here you are, finally settled in your new home. As you look around the house a thought comes through your mind:

30 years is a long time. Is there a way to shorten the loan term?

Is there a way to pay off the home loan sooner?

When interest rates are affordable, it is a good time to consider ways to pay off your home loan faster, such as increasing the amount and frequency of your home loan repayments.

Another way to reduce your home loan balance and pay it off faster is by using a mortgage offset account.

Jump straight to…

Mortgage Offset Account Explained

A mortgage offset account provides you the opportunity to pay off your home loan sooner, potentially saving thousands of dollars in interest repayments.

An offset is a linked account to your home loan that functions similarly to a transaction account or savings account.

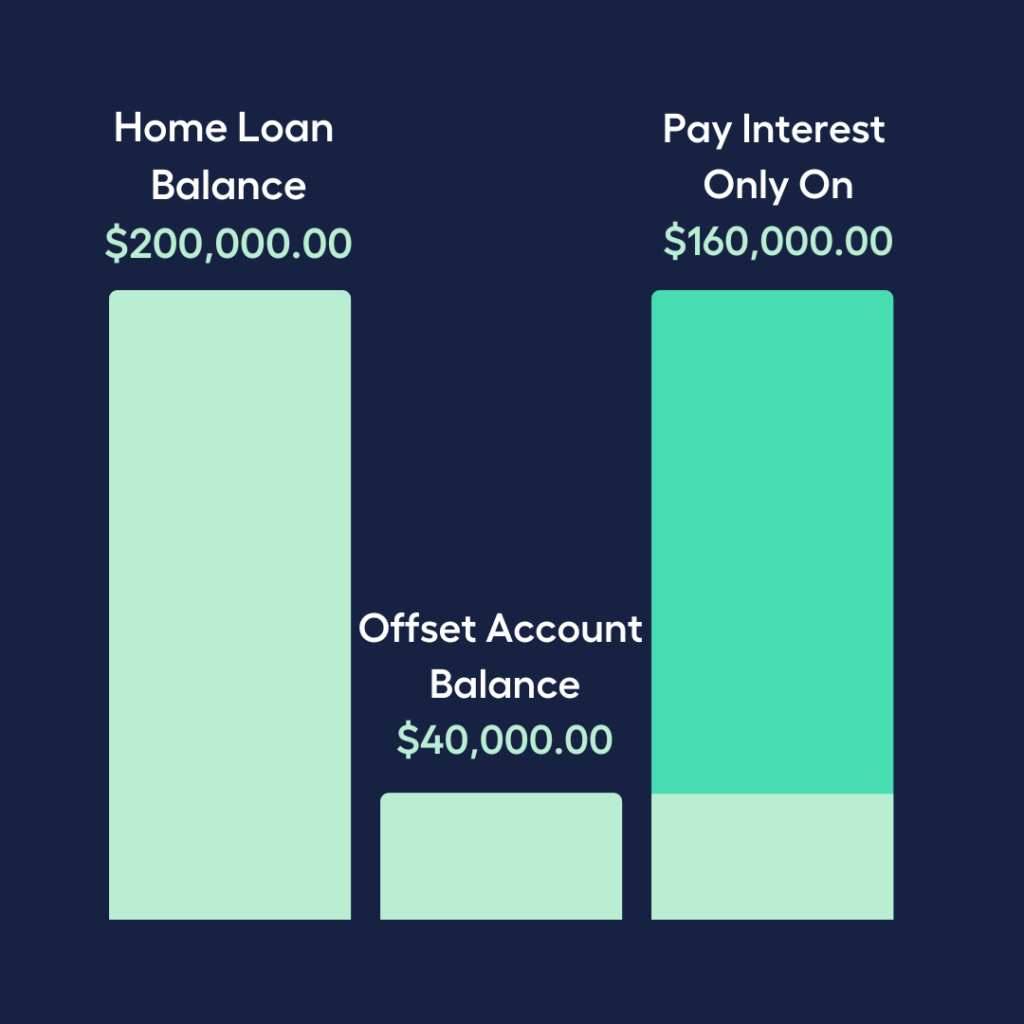

As its name implies, the amount in an offset account reduces the balance amount of a home loan. Thus you’ll only be charged interest on the reduced home loan balance.

As a simple explanation, imagine you have a home loan balance worth $200,000 and extra funds worth $40,000. If you put the $40,000 in an offset account, you only pay interest on $160,000.

Having an offset account does not necessarily reduce the amount of your monthly repayments.

You pay the same amount on monthly repayments but most of it goes to repaying the principal amount and less to pay interest. Thus, you have the potential to shorten your loan term and save money on interest overall.

Imagine you have a $100,000 home loan with a monthly repayment of $1,061 for 10 years at 5% interest per year.

Now, imagine the same loan with the same terms, but this time you have money in your offset account worth $20,000. So you’re paying $1,061 monthly against $80,000.

| Loan Amount: $100,000 Term: 10 years Annual Interest: 5% Monthly Repayment: $1,061 | ||

| Regular Home Loan | Home Loan with $20,000 Offset | |

| Balance | $100,000 | $100,000 |

| End of Year 1 | $92,762.81 | $91,826.81 |

| End of Year 2 | $84,480.87 | $82,473.74 |

| End of Year 3 | $75,775.20 | $72,642.15 |

| End of Year 4 | $66,624.14 | $62,307.55 |

| End of Year 5 | $57,004.89 | $51,444.22 |

| End of Year 6 | 46,893.51 | 40,025.10 |

| End of Year 7 | 36,264.80 | 28,021.76 |

| End of Year 8 | $25,092.31 | 16,497.28 |

| End of Year 9 | $14,349.43 | $0.00 |

| End of Year 10 | $0.00 | $0.00 |

With a home loan offset account, you’re no longer paying loan interest

on your home loan by the 9th year and can pay off the loan!

Now that you have a general idea of how a home loan and an offset work together, let’s dive into the specifics of how an offset account works in your favor.

How Does an Offset Mortgage Account Work?

Not all lenders offer a home loan offset account. Shop around and look for a lender that offers an offset account as a home loan feature.

Similarly, an offset is usually featured with a variable rate home loan, and lenders also offer different types of offsets.

Different Types of Offset Accounts

100% Offset or “Full” Offset

100% or “full” offset accounts use all of the money in your offset account to reduce the balance on your home loan account. These are frequently offered for house loans with variable rates.

The ‘interest’ that you accumulate on the offset account lowers the interest that you must pay on your loan each month. You will be paying back the loan principle more frequently.

Partial Offset

The interest you pay on your offset balance is less than the interest you pay on your loan. For instance, if your loan rate is 3% and the offset rate is 1%, you are still saving money, but not to the same extent as with a 100% offset.

Partial Balance Offset

A different type of partial offset account uses only a portion of the balance to offset your loan. Certain fixed-rate loans can be eligible for these types of accounts.

You would deduct $8,000 from your loan balance (40% of $20,000) and pay interest on $192,000, for instance, if you had a 40% partial offset account with a loan balance of $200,000 and savings of $20,000.

Just as there are different types of offset accounts, there are also different ways to package a home loan with an offset.

Let’s start with the ideal one!

Ideal Home Loan Offset Account Package

Depending on your financial situation, a home loan offset account works best as a package with a variable interest rate home loan, and a credit card with interest free days.

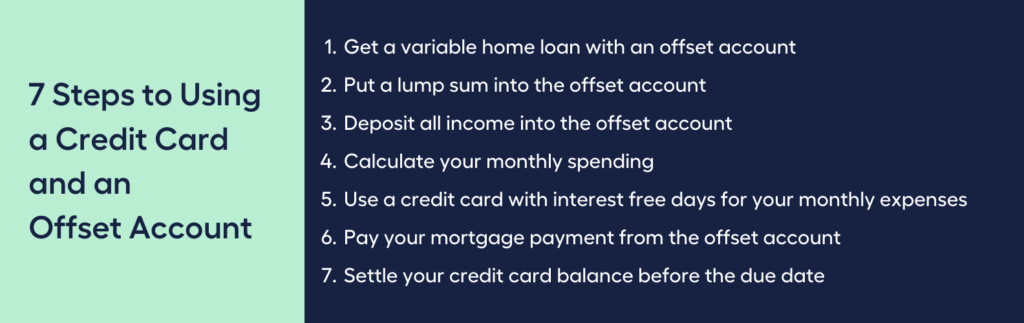

7 Steps to Using a Credit Card and an Offset Account

- Get a variable home loan with an offset account

- Put a lump sum into the offset account

- Deposit all income into the offset account

- Calculate your monthly spending

- Use a credit card with interest free days for your monthly expenses

- Pay your mortgage payment from the offset account

- Settle your credit card balance before the due date

Step 1:

Get a variable home loan with an offset

Variable rate home loans have interest rates that vary over time, and you benefit from any interest rate drops over the term of your home loan. If interest rates fall, you will pay less interest on your home loan balance.

Step2:

Put a lump sum into the offset

The lump sum becomes the starting point for saving money on your home loan through this transaction account. Deposit an amount that you can afford to keep there long-term.

Step 3:

Deposit all income into the offset

Your home loan interest is calculated daily based on the outstanding loan balance (and then charged according to your weekly, fortnightly or monthly repayment schedule). Every dollar you have in your linked transaction account saves you interest every day that it’s there.

Your offset account will also function as your everyday transaction account.

Step 4:

Calculate your monthly spending

The idea behind this approach is to keep your pay in the offset account for as long as you can, so be very thorough when calculating your monthly expenses.

You can use the MMS Expense Planner calculator to keep things simple.

Note: Do not include your home loan repayments in your budget since these will be deducted directly out of the offset account.

Step 5:

Use a credit card with interest free days for your monthly expenses

Obtaining a credit card with interest-free periods and promptly paying off the entire balance by the due date of each statement are critical to the success of this strategy.

As a result, you can use the card for regular purchases without incurring interest on the balance.

A word of warning here. If you fail to repay the monthly balance by the due date you will be charged interest on the balance so be sure to repay this on time.

Step 6:

Pay your mortgage payment from the offset

Pay your home loan directly from the offset account when it is due. You will be charged less interest on your home loan based on the daily balance of your offset.

Thus, you save money on interest charges each month, even when your repayments reduce the offset account balance until your next payday.

Remember two things:

- Your offset transaction account doesn’t earn interest

- Your repayment amounts should stay the same when you use this strategy.

Step 7:

Settle your credit card balance before the due date

Pay the balance on your credit card statement with the salary you deposit into the everyday transaction account you designated as an offset account.

To make this strategy work, you must pay the entire amount listed on your statement before the due date. Otherwise, credit card interest charges could negate the benefits of having money in your offset account.

This strategy even works better than simply having a lump sum of money sitting in an offset account.

Imagine you have a $100,000 home loan with a monthly repayment of $1061 for 10 years at 5% interest per year. You have an offset account with $20,000 but it also functions as an everyday transaction account where you deposit $1000 and withdraw credit card payments too.

| Week | Home Loan Balance | Deposit or Withdrawal | Offset Account Balance | Amount Interest is Calculated Against | Monthly Payment | Interest Payment | Principal Payment |

| 1 | $100,000.00 | $20,000.00 | $80,000.00 | ||||

| 52 | $91,049.09 | -$2,061.00 | $26,207.00 | $64,842.09 | $1061.00 | $270.18 | $790.82 |

| 104 | $79,537.46 | -$61.00 | $64,414.00 | $15,123.46 | $1061.00 | $63.01 | $997.99 |

| 156 | $65,264.37 | $102,621.00 | $1061.00 | $1,061.00 |

With the credit card and home loan offset account, your offset account balance has exceeded your home loan balance in the third year and you are no longer paying loan interest on your home loan!

Can You Have Multiple Offset Accounts?

In most cases, you can only link one offset account to your home loan. However, some lenders provide multiple offset accounts as a home loan feature.

Your funds from multiple accounts are totaled, and the total value of the funds in your offset accounts is deducted from your loan. These are referred to as multiple offset accounts.

When linking multiple accounts from the same bank, you are able to track your financial situation and save on interest conveniently.

You may not have a lump sum of money to put into your home loan offset accounts but you have more money saved for other things. You can create multiple accounts for these different purposes – one transaction account linked for daily expenses, one for your holidays, and multiple savings accounts depending on your personal goals.

On the other hand, monthly offset fees may be charged for each offset you have connected to your mortgage, increasing the annual fee component.

What other implications come with an offset account?

Offset Account Tax Implications

Your offset account not earning interest is advantageous as the money in it is not considered as taxable income.

However, when you withdraw funds from your linked mortgage offset account for a deposit on an investment property, you are not entitled to a deduction for the amount of charged interest on your home loan.

According to the Australia Taxation Office (ATO), an investment property has assessable value, thus taxable.

There are other tax implications when we compare an offset account with a redraw facility.

Offset Account and Redraw Facility Tax Implications

An offset account functions more like a typical transaction or savings account. You only pay interest on the difference after deducting the offset account balance from the remaining balance of your mortgage.

A redraw facility allows you to make additional payments to lower the remaining balance of your mortgage, which reduces the interest you pay.

However, those extra payments are not locked away; at a later date, you can withdraw them. This increases the loan balance, so you will pay higher interest rates.

Investment Property: Offset or Redraw Facility

Imagine you buy an investment property and get a loan of $400,000. The interest on an investment property loan is tax deductible. You then receive an inheritance that allows you to pay off $100,000, leaving a loan balance of $300,000.

| Investment Property Loan | $400,000* Interest of loan amount is tax deductible |

| Less loan payment (from inheritance) | $100,000 |

| Investment Property Loan Balance | $300,000* Interest of loan amount balance is tax deductible |

Afterwards you redraw $50,000 for a holiday. The loan reverts to $350,000, but as the redraw is for personal use the loan amount attributable to the investment property remains at $300,000.

| Investment Property Loan Balance | $300,000 *Interest of loan amount balance is tax deductible |

| Add redraw amount used for a holiday (loan used for personal purpose) | $50,000 *tax deduction can’t be claimed for interest of this amount |

| New Loan Amount | $350,000 *only the interest of $300,000 is tax deductible |

You can’t claim a tax deduction for the interest on the $50,000 redraw.

Now suppose you added an extra $100,000 to your offset account. The bank deducts this from the $400,000 remaining on your loan and only assesses interest on the $300,000 difference.

| Investment Property Loan | $400,000 |

| Less Offset Account Deposit | $100,000 |

| Investment Property Loan Balance | $300,000 *interest charges will be based on this loan balance |

The key distinction is that the loan balance, which is still $400,000, is entirely attributable to the investment property.

The $50,000 withdrawal from your offset account has nothing to do with the investment. You will pay interest on the entire $350,000 loan amount, but it will not all be deductible from your taxes.

An offset account gives you more flexibility in managing your home loans and savings accounts compared to a redraw facility.

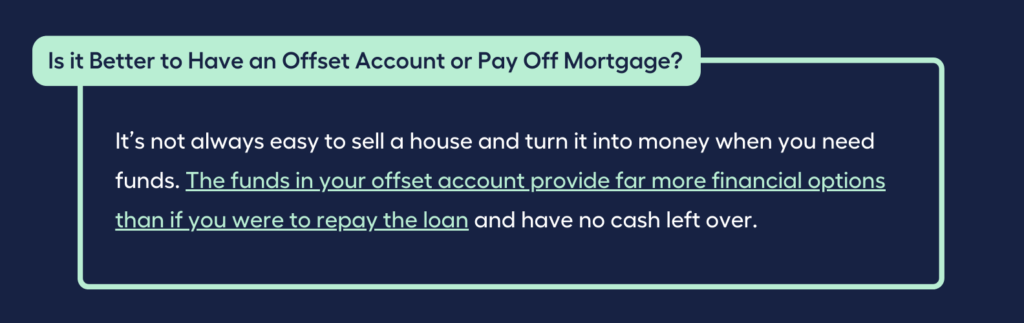

Is it Better to Have an Offset Account or Pay Off Mortgage?

The sooner you pay off your mortgage debt, the better your financial situation will be. However, you may be in a better position if you put extra mortgage payments into your offset account rather than directly into your mortgage.

It’s not always easy to sell a house and turn it into money when you need funds. The funds in your offset account provide far more financial options than if you were to repay the loan and have no cash left over.

Imagine you still owe $200,000 on your mortgage. You also have $170,000 in your offset account. You’ve been making extra repayments on the loan and can pay off the loan with $30,000.

| Account Details | Amount | Deduct |

| Mortgage Balance | $200,000 | |

| Offset Account | $170,000 | |

| Balance You Pay Interest On | $ 30,000 |

Scenario #1: You Close Out Your Mortgage

You keep adding to your offset account until you reach $200,000, and then settle the loan. You’re out of debt but you also have $0 left.

| Account Details | Amount | Deduct |

| Mortgage Balance | $200,000 | |

| Offset Account | $200,000 | |

| Balance You Pay Interest On | $0.00 | |

| Savings in Offset Account | $0.00 |

Scenario #2: Keep the Mortgage Open

You keep adding to your offset account, but don’t pay off the loan. You can add a little bit of money to the offset account each month.

Leaving money in the offset account is effectively the same as paying it off. Because you’re only paying interest on $30,000 in loan principal, your interest charges are minimal.

Best of all, you have a lot of money you can easily access in the offset.

| Account Details | Amount | Deduct |

|---|---|---|

| Mortgage Balance | $200,000 | |

| Offset Account (increasing) | $170,000 | |

| Balance You Pay Interest On (decreasing) | $30,000.00 | |

| Savings in Offset Account | $170,000 |

Remember that money in an offset account belongs to you; extra repayments do not and thuis you can no longer access these once you paid them.

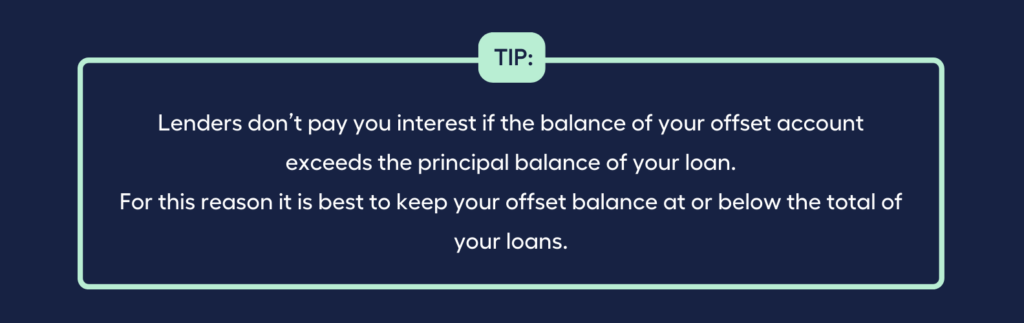

What Happens if Offset Account is More Than Loan?

You might deposit more money into your offset account than into the loan itself.

Once you’ve saved more than the amount of the loan, an offset interest is no longer helpful. And unlike a typical savings account, your lender will not pay you interest on the additional funds you have in your offset account.

Therefore, it is best to keep your offset balance exactly at or below the total of your loans. When you have excess money, you can start depositing it independently in a term deposit or a high return savings account.

Benefits of Using a Mortgage Offset Account

To recap, there are four benefits of using an offset account:

1. It shortens the term of your loan by lowering the balance of the loan against which interest is charged while maintaining your current repayment schedule.

2. It reduces interest payments. The more money you have in your offset account, the less interest you will pay on your home loan.

3. Potential tax advantages since your offset account’s interest gain is not regarded as taxable income.

4. Flexibility. Access to the funds in your offset account is unrestricted.

Disadvantages of an Offset Account

While we have covered off on the advantages of a mortgage offset account, it’s worth also considering the disadvantages.

1. Higher than average fees – be aware that having an offset account may incur additional charges.

2. Higher interest rates. Home loans with offsets normally have higher interest rates. Calculate the numbers to ensure that it is appropriate for you.

3. A sizable deposit is required in some circumstances for the account to be cost-effective given the added expenses.

4. Financial discipline is necessary. You likely will not get the full rewards of the feature if you regularly withdraw money from the offset account or leave the account with a zero balance.

Is it Worth Having an Offset Account?

The above mentioned pros and cons tells us that the offset strategy is not for everyone.

If you have a lot of additional debts, the offset strategy may not be for you at this moment. It’s typically best to settle all your debts first before getting an offset account.

If you lack discipline and can’t stick to a budget, you may find it difficult to keep track of your financial affairs.

However, an offset account may be a great option for you if you’re in a good financial position and can afford a home loan. One way to check your financial position and see if an offset strategy suits you is to check your borrowing power.

Check Your Borrowing Power with MMS Mortgage Calculator

Knowing your borrowing power is just the first step. A mortgage is a big investment of both time and money, which is why It’s often best to receive guidance from a financial expert like a mortgage broker.

Many people may be unaware of this…but just like you, 41% of Aussies intend to get financial advice rather than going it alone, according to an Australian Securities and Investments Commission (ASIC) report.

Find the right Mortgage Broker for you with the help of My Money Sorted.

When you book a call with an My Money Sorted, you’ll:

✓ get a better understanding of your financial options

✓ have an idea of the experts you can call on to help you reach your goals

✓ be matched with a mortgage broker who can help develop the best home loan strategy for your situation

My Money Sorted is your stress-free pathway to getting ahead with your home loan.

Here’s what your journey will look like:

Step 1: Start off with a quick money matters session with My Money Sorted

Step 2: Get matched with a licensed Mortgage Broker that’s right for your financial situation

Step 3: Take the first step towards your financial goals with a clear roadmap that makes sense prepared by an experienced Mortgage Broker.

It’s that easy!

Get Ahead Of Your Home Loan by Speaking with My Money Sorted Today