Retirement is a life changing leap that everyone plans for at some point in their life. The change is so important that most of us want to avoid mistakes when planning for retirement.

However, some of us fail to realise its importance or plan for it too late.

Immediately, those are two retirement planning mistakes to avoid.

Jump straight to…

The Most Common Pitfalls in Retirement Planning to Watch Out For

We can’t see the future, we can’t anticipate what’s to come, and this makes creating a retirement plan a difficult task. But at the same time, if we could imagine the future, we can create a financial plan that can afford us a comfortable retirement.

Leaving Retirement Planning Till You’re Ready to Retire

While the old saying, “It’s never too late” may hold true, realising that at the latter years of your career you need a retirement plan may leave you thinking:

Do I have time to save for my retirement 10 years from now?

The question alone can cause a lot of stress and sleepless nights.

Fortunately, realising you need a financial plan for retirement at this stage may still work out for you if you follow these 5 steps.

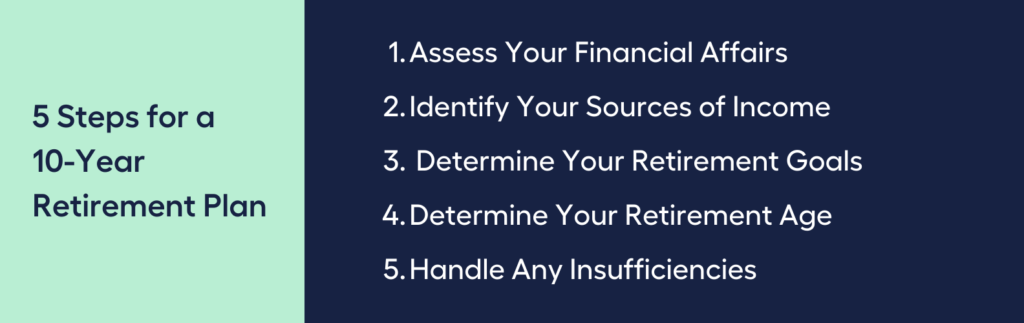

5 Steps for a 10-Year Retirement Plan

1. Assess Your Financial Affairs

2. Identify Your Sources of Income

3. Determine Your Retirement Goals

4. Determine Your Retirement Age

5. Handle Any Insufficiencies

If you plan or need to retire in 10 years, you have to understand that it will take a lot of discipline to stick to a 10-year plan. A 10-year plan to grow your money will test your willpower if you aren’t accustomed to wealth management.

Step 1:

Assess Your Financial Affairs

An honest evaluation of your current financial affairs is essential to developing a financial plan. Acknowledging that you might not be financially ready for retirement is a good starting point.

- Begin by calculating how much money you have accumulated in retirement accounts including your superannuation account and other investments.

- Your super balance can be found on your annual statement. You can also check in and see how it’s doing by logging into your super account online or through a mobile app.

Include taxable accounts if you intend to use them solely for retirement, but leave out cash set aside for an emergency fund or bigger purchases like a new car.

Step 2:

Identify Your Sources of Income

The majority of retirement money should come from existing retirement funds, but it might not be the only source. Age pension can be the lone source of retirement income for people who don’t have any retirement savings.

If you receive the Age Pension, you will also receive health benefits as well as reduced rates on telephone, gas and electricity, car registration, and public transportation costs.

Check the monthly income from Age Pension and include it to your list of resources. Income from a part-time employment while in retirement can also be added up.

Sources of Retirement Income

- Savings

- Superannuation

- Age Pension

- Other Investments

- Part-time Income

Step 3:

Determine Your Retirement Goals

Each individual has different retirement goals, as such they have different views on financial security at retirement age.

- Create a monthly budget to get a close to accurate estimate of regular retirement expenses, such as housing, food, eating out, and leisure activities.

- Be sure to include the cost of health and medical expenses in your budget estimate because they can add up significantly later in life and affect your cash flow. Examples of these costs include life insurance, long-term care insurance, prescription medications, and doctor visits.

Simplify your budget planning by using the MMS Budget Planner calculator. It can help you get a better understanding of your financial position by understanding your income and expenses.

Step 4:

Determine Your Retirement Age

A retirement plan entails assessing not only your expected spending habits in retirement, but also how many years you expect to be retired. A retirement that lasts 30 to 40 years differs greatly from one that lasts only half that time.

A reasonable target retirement age strikes a balance between the size of your retirement fund, also known as a retirement portfolio, and how long that retirement nest egg will last.

Step 5:

Handle Any Insufficiencies

| Is my Retirement Fund greater than the amount I’ll need to retire comfortably? | |

| Answer | What to do |

| Yes | Continue adding savings to your retirement accounts to stay on track |

| No | Find a way to bridge the gap |

| I’m behind schedule | Look for ways to earn more, save more money, decrease unnecessary spending |

All of the figures added up at this point should help answer the important question:

Is my retirement fund greater than the amount I’ll need to retire comfortably?

If the answer is yes, it is critical to continue adding savings to your retirement accounts in order to keep up the pace and stay on track.

If you answered no, it’s time to figure out how to bridge the gap because the age pension alone isn’t going to cut it.

If you are behind schedule, you need to figure out ways to add to your savings accounts and avoid financial hardship.

To make significant changes, you will most likely need to increase your savings rate and look for ways to earn more, while decreasing unnecessary spending. You need to eliminate your personal debt and credit card debt asap too.

You may also need to seek financial personal advice.

If you’re sick, you visit a doctor because that’s their expertise. If you need a financial plan, it’s best to talk to a financial advisor because retirement planning and wealth management is an area of expertise.

Get ahead of your retirement goals without the stress

with the guidance of a financial advisor.

Find the right financial advisor for you with the help of an My Money Sorted.

Or you can keep on reading, before seeking financial advice, to get an idea of how much income you need for retirement.

Not Enough Retirement Savings

A study by the Australian National University found most Australians accept that retirement income need not be equal to their current income.

Most Australians anticipate their retirement income to be 70% percent of their current income.

The current national median personal income is $41,860 ($805 weekly) according to the Australian Bureau of Statistics. At 70%, that’s an annual retirement income of $29,302.

Can you retire comfortably at $563 a week?

That’s higher than the current age pension annual income of $23,420.80 (maximum basic rate of $900.80 per fortnight). However, it’s lower than the Association of Superannuation Funds of Australia (ASFA) retirement standard for comfortable and modest living.

| ASFA RETIREMENT STANDARD FORCOMFORTABLE AND MODEST LIVING(annual retirement income) | ||

| Comfortable Income | Modest Income | |

| Single | $47,383 | $30,063 |

| Couple | $66,725 | $43,250 |

If you’re planning on a comfortable retirement and facing a shortfall, there are a number of things you can do to get your retirement on track.

Earlier we mentioned increasing your savings rate while decreasing unnecessary spending, and eliminating personal and credit card debts.

You can also consider increasing your super balance by making additional contributions to your superannuation account, deferring retirement, adjusting your retirement lifestyle expectations, or selling other assets.

You can work to improve your situation simply by knowing your current and projected retirement savings.

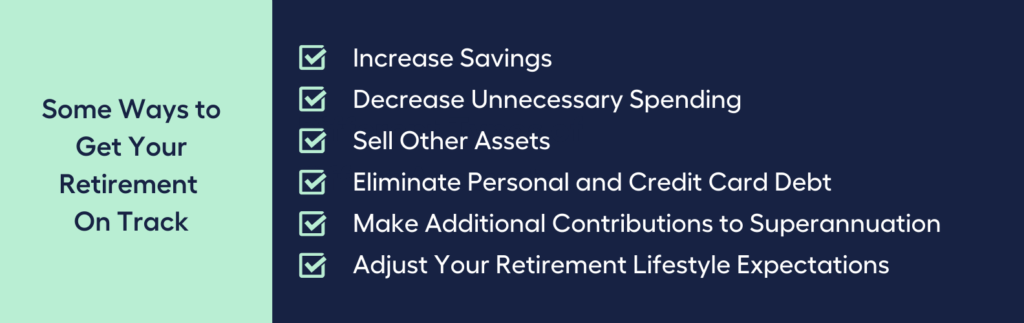

Some Ways to Get Your Retirement On track

✓ Increase Savings

✓ Decrease Unnecessary Spending

✓ Eliminate Personal and Credit Card Debt

✓ Make Additional Contributions to Superannuation

✓ Sell Other Assets

✓ Adjust Your Retirement Lifestyle Expectations

A financial plan to retire comfortably requires proper wealth management and a certain amount of risk tolerance.

Avoids Investing

If you have money to spare, money you don’t need or use to cover your weekly cost of living, it would be wise to consider the sharemarket as an investment option. With hundreds of lower-risk investment options like index funds and ETFs it’s now possible to invest in the sharemarket even if you have a low risk tolerance.

Leave your spare money to grow in an investment fund instead of giving it away or burning through it.

Whatever the investment has earned when you retire is basically free money!

Consider this:

According to a widely held belief, retirees should focus on their financial security by reducing their investment risk by putting more of their funds into cash and fixed interest investments rather than growth assets like shares and real estate.

However, even a 10-year investment horizon is lengthy, let alone one of 20 or 30 years. Savings could run out quickly if money is moved from growth assets into cash and fixed interest investments too soon after retiring.

So if retirees shouldn’t move money from growth assets too soon, it may be wise for your wealth management plan to include investing in growth assets.

According to one rule, investors should deduct their age from 110 to determine how much money they should put into growth assets. For instance, a 70-year-old might aim for a balance of 40% growth assets and 60% cash and fixed interest investments.

When looking to invest in growth products, consider its past performance, future performance, investment returns, investment fees, admin fees, and reviews ratings.

Should people with a low risk tolerance invest in shares too?

Approach any financial institution and they’ll probably give the same investment advice:

Don’t put all your eggs in one basket.

Doesn’t Diversify Their Income

Investment industry experts suggest that to invest wisely, people need to diversify or put their money in different investment options. It makes sense to diversify a financial portfolio for wealth management because diversification minimises risk.

Shop around for a financial institution that offers different investment choices and financial products. Look for investment products that are easy to sell or turn into cash.

Here are the Different Assets to Consider for Wealth Management and a Diversified Portfolio:

1. Cash Investments

2. Fixed interest or Fixed Income Investments

3. Shares

4. Managed Funds

5. Exchange Traded Funds (ETFs)

6. Investment Bonds

7. Annuities

8. Listed Investment Companies (LICs)

9. Real Estate Investment Trusts (REITs)

1. Cash Investments

Cash investments (such as savings accounts and term deposits) provide consistent, low-risk income in the form of regular interest payments, so they may be a good choice if you are risk averse or working on a short timeframe.

2. Fixed Interest or Fixed Income Investments

Fixed interest investments (a.k.a. fixed income or bonds) typically have a 5-year investment period and provide predictable income in the form of regular interest payments that are higher than cash investments. Governments and corporations in Australia and around the world issue fixed-income investments.

3. Shares

Buying shares (also known as equities or stocks) in an Australian or international company, essentially means purchasing a piece of that company and becoming a shareholder. If the value of the company’s shares rises, so will the value of your investment, and if the company makes a profit you may receive a portion of the company’s profits in the form of dividends.

4. Managed Funds

Managed funds pool investors’ money which is then invested and managed by a fund manager. A managed fund can specialise in a specific asset class; for example, an Australian shares managed fund will only invest in Australian companies. It can also be a diversified managed fund with a mix of cash, stocks, and real estate.

One of the advantages of pooling your assets in this manner is that you can gain access to investments and a level of diversification that an individual would not normally be able to obtain.

5. Exchange Traded Funds (ETFs)

An ETF is a type of managed fund that can be purchased and sold on a stock exchange, such as the Australian Stock Exchange (ASX). An ETF tracks a specific asset or market index. An index is a yardstick that measures investment performance.

ETFs are typically ‘passive’ investment options because they aim to track an index rather than outperform it.

6. Investment Bonds

An investment or growth bond (a.k.a. an insurance bond), pools investors’ money with an investment manager overseeing the funds and making day-to-day investment decisions, similar to a managed fund. Investment bonds are regarded as ‘tax-paid’ investments, with earnings taxed at 30% along the way. If you pay more than 30% in income tax, an investment bond may be a tax-efficient way to invest.

7. Annuities

Annuities provide a guaranteed income regardless of what happens in financial markets. These can take the form of a series of regular payments over a specified number of years (fixed-term) or for the rest of your life (lifetime annuity).

The payments you receive will be determined by factors such as the amount you put in and actuarial calculations, which forecast future outcomes based on economic and demographic trends.

An annuity can be purchased with either super or regular savings. It’s worth noting, however, that if you use your super money to make the purchase, you won’t be able to access the funds until you reach your preservation age and retire.

8. Listed Investment Companies (LICs)

LICs are a type of investment vehicle that is formed as a company and traded on a stock exchange. To provide diversification, most LICs operate similarly to managed funds, with an internal or external manager responsible for selecting and managing the company’s investments on your behalf. LICs frequently purchase stock in other companies.

8. Listed Investment Companies (LICs)

A REIT is a type of property fund that is listed on a public exchange, such as the ASX, and in which investors can buy units. Your money in the fund is then pooled and invested in a variety of property assets, which may include commercial, retail, industrial, or other property sectors, similar to a managed fund.

REITs can provide investors with more diversified exposure to the property market – including commercial and industrial property – and can potentially be more accessible and cost-effective than purchasing a single property.

Do note that income from most of these products is taxed. Aside from tax implications, there may be investment fees and exit fees attached to most of them.

Wealth management for a diversified portfolio needs the advice of an expert.

Find the right financial expert who can help you develop the best retirement plan by talking to My Money Sorted.

Or you can keep on reading to get an idea how inflation affects your retirement income.

Doesn’t Account for Inflation When Calculating Retirement Income

While your super fund and age pension may look like it will be enough at this point, additional investments help buffer the weight of inflation and other costs in the future.

Just like the rise and fall of interest rates, inflation is a natural process of economic growth, which explains why haircuts no longer cost a dollar and petrol is now regularly $2 per litre.

When interest rates fall, people have more money to buy goods and services. But if the demand for goods and services is greater than what’s available in the market, prices of goods increase. This is inflation at work, the impact of which is the buying power of your money decreases.

It’s wise to calculate inflation in your investment strategy. Consider increasing your savings, adding to your super fund, and diversifying investments to protect against inflation.

Underestimates Healthcare Costs

Speaking of insurance, have you considered healthcare insurance in your retirement?

Anyone with a Medicare card can receive free medical care in a public hospital as part of the comprehensive public healthcare system known as Medicare. Citizens, permanent residents, and some travellers are all covered for the majority of medically necessary procedures without any out-of-pocket costs.

The private healthcare system in Australia is made up of for-profit hospitals and other service providers. Because the majority of private patients have private health insurance, the majority of the cost of health care they receive is covered by a health fund. However, even after the health insurance benefit, most private treatments have out-of-pocket costs.

Medicare and private healthcare have pros and cons. Consider them when planning your personal finances after retirement.

| Medicare and Private Healthcare ✔️Pros and ❌Cons | |

| Medicare | Private Healthcare |

| ✔️ A public hospital will typically not charge you any out-of-pocket expenses. | ❌ Even if you have health insurance, you will most likely have out-of-pocket expenses as a private patient. |

| ✔️ The majority of hospital treatments are provided for free in public hospitals. | ❌ There aren’t many treatments available in the private system that aren’t also available through Medicare. |

| ✔️ Some out-of-hospital treatments, such as GP and specialist visits, as well as some medications, are covered. | ✔️ Private patients can still receive out-of-hospital care, such as GP visits and PBS medications. |

| ❌ Some surgeries will require you to join public waiting lists. | ✔️ In general, your wait for surgery in the private system will be shorter than in the public system. |

| ❌ For your treatment, you will be assigned a doctor or surgeon. | ✔️ You will frequently have a choice of doctor, specialist, or surgeon. |

| ❌ As a public patient, you will frequently be required to share a room with other patients. | ✔️ As a private patient, you may have access to a private room in a public or private hospital. |

As you go through your list of assets and sources of income in your retirement plan, remember to protect them in order to make the most of your income and assets after retirement.

Doesn’t Protect Their Income and Assets with Insurance

It took you a decade or more to build your financial portfolio so you can retire according to your retirement plan. Don’t put yourself at risk in your financial situation after retirement by not insuring your assets and sources of income.

Natural disasters in Australia have highlighted the importance of having adequate insurance coverage on major assets, particularly houses. A policy of “general insurance” refers to coverage on assets such as a house or a car.

If you lose these assets, having adequate insurance in place will ensure you are compensated for your loss.

Another source of income you need to insure is yourself.

We don’t know how long we’ll get to enjoy retirement, and we won’t know in advance if we will accumulate more wealth or debt after retirement.

Estate planning is another item you need to cover with wealth management. Insuring yourself ensures that your heirs need not worry about debts you leave behind.

Asset protection and estate planning are financial decisions that need guidance.

Find the right financial expert to provide you with professional help with your estate planning and asset protection by talking to My Money Sorted.

Or you can keep on reading to know how taxes affect your retirement.

Poor Tax Planning

Creating a diversified financial portfolio from different income streams ensures a high chance of living comfortably for a long period of time after retirement.

But don’t forget that income generated from most of these investments are subject to income tax, even your income from government funds. Fortunately, you may be eligible for Seniors and Pensioners Tax Offset (SAPTO) for deductions.

The Age Pension is part of your taxable income. If it is your sole source of retirement income, you will not be taxed.

Super investment earnings are typically taxed. This includes interest and dividends, less any tax deductions or credits.

Super income stream (withdrawing your super money in small regular payments over a long period of time)

– is usually tax free if you’re aged 60 or over

– is subject to tax if you’re under 60

Super Lump sum withdrawals

– You may be required to pay tax if you haven’t reached preservation age.

– It’s unlikely you’ll be required to pay any tax when you withdraw from a taxed super fund if you’re aged 60 or over.

– You may pay tax if you withdraw from an untaxed super fund if you’re aged 60 or over.

An Annuity purchased with money from outside super is taxed at your marginal tax rate.

Investment income earnings are taxed at your marginal tax rate. This includes earnings from interest, dividends rent, managed funds distributions, capital gains from property, shares and cryptocurrencies.

Take time to reflect on your key takeaways from this article.

Don’t Get Caught Out With These Retirement Mistakes – Get Your Money Sorted with Professional Financial Planning Advice

Now that you’ve taken note of what not to miss when planning for retirement, take the next step towards a comfortable retirement with the guidance from a financial expert.

Many people may be unaware of this…but just like you, 41% of Aussies intend to get financial advice rather than going it alone, according to an Australian Securities and Investments Commission (ASIC) report.

Find the right Financial Adviser for you with the help of My Money Sorted.

When you book a call with My Money Sorted., you’ll:

✓ get a better understanding of your money matters

✓ have an idea of the experts you can call on to help you reach your goals

✓ be matched with the right financial adviser who can help simplify your family’s journey to financial wellness

My Money Sorted is your stress-free pathway to getting ahead with your money. Here’s what your journey will look like:

Step 1: Start off with a quick money matters session with My Money Sorted.

Step 2: Get matched with a licensed Finance Adviser that’s right for your money situation

Step 3: Take the first step towards your money goals with a clear and sound roadmap prepared by an experienced Financial Adviser

It’s that easy!

Speak with My Money Sorted About Your Retirement Needs Today