Is it too late to build wealth in your 40s?

According to the Australian Bureau of Statistics (ABS) the average retirement age in Australia is 55.

You may be thinking, “that seems a little early doesn’t it”?

And you would be right. In fact many Australians return to work after retiring.

State Super’s 2018 Study Beyond Paid Work discovered that 36% of those who returned to work after retiring cited financial reasons.

Given these figures, wouldn’t it be nice to retire wealthy and have savings to cover your cost of living indefinitely?

Fortunately, if you invest smartly, it is possible.

But investing at any age isn’t always straightforward.

In this article, we will explore ways to build wealth at any stage of life, learn about the different sources of income that could help in wealth building, and look at how to calculate the cost of securing your financial future.

Jump straight to…

Is it too late to start investing in your 40s?

No, you haven’t missed the bus if you’ll only start investing in your 40s.

In fact, your 40s are your prime earning years! It’s the perfect time to have investment accounts and build long term wealth!

If your current super or savings balance isn’t as large as you’d like it to be, don’t worry. We have tips to begin investing your hard earned savings at any stage of life.

How to Build Wealth At Any Stage of Life

Investing to build wealth is important at any stage of life, but the same investment strategy doesn’t apply to all stages of life.

You may have been more tolerant of risk when you were younger, but you had less money for investments. While those who are nearer retirement age have more money saved but less time to make up for any losses from riskier investments.

Investing requires different strategies for every financial situation or needs in life, but there are constants such as setting an investment goal and knowing your financial situation.

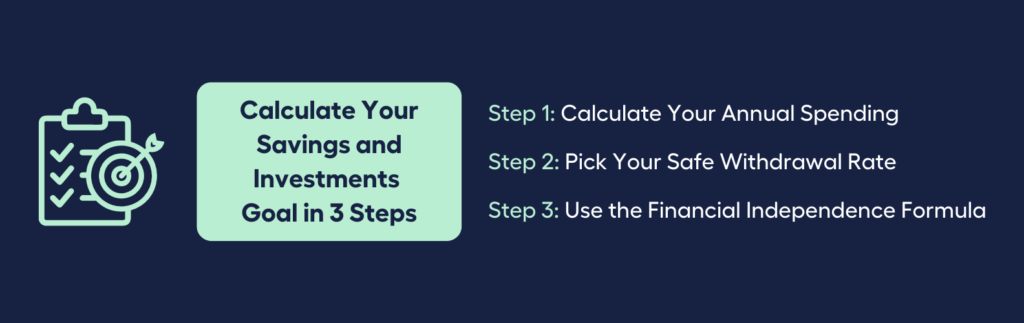

Calculate How Much Financial Independence Will Cost

Before we start thinking of creating an investment strategy, let’s put a number to your financial independence or savings and investments goal.

Calculating your savings an

Step 1:

Calculate Your Annual Spending

Sum up your monthly expenses (including ongoing monthly contributions to accounts such as your emergency fund, savings for holidays, car maintenance, and so on) and multiply it by 12.

Add quarterly bills multiplied by four, then add your annual premiums.

| How to Calculate Your Annual Spending | |

|---|---|

| Monthly Expenses x 12 = | Annual expense |

| Quarterly bills x 4 = | Annual bills |

| Semi-annual contributions x 2 = | Annual contributions |

| Annual premiums = | Annual premiums |

| TOTAL | Annual Spending |

Step 2:

Pick Your Safe Withdrawal Rate

The safe withdrawal rate (SWR) is a method that teaches financially independent people how to withdraw money from their bank accounts each year, typically between 3-4% of the balance, without running out of funds for the rest of their lives.

The 4% rule stems from an influential 1998 study by three professors of finance at Trinity University.

The study discovered that the 4% rule holds true regardless of market ups and downs. Your assets can last the rest of your life if you don’t withdraw more than 4% of your initial investments each year.

Step 3:

Use the Financial Independence Formula

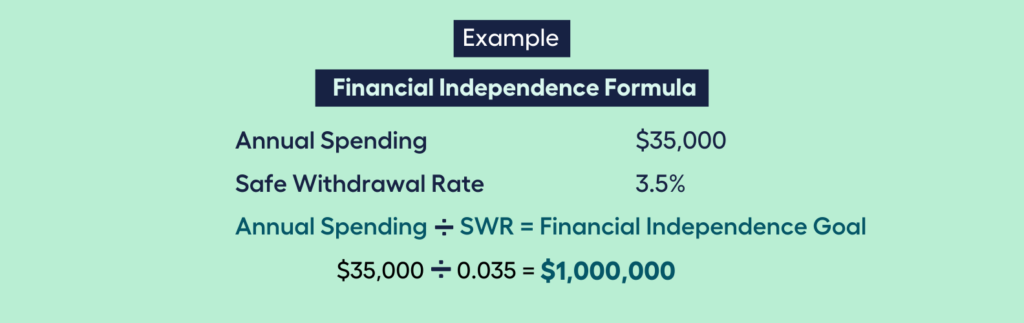

Your financial independence number is calculated by dividing your annual spending total by your safe withdrawal rate.

For example:

If your annual spending of $35,000 is divided by your safe withdrawal rate of 3.5%, your financial independence number will be $1,000,000.

Now that you can estimate how much savings you need to be financially independent, it’s time to understand your spending habits.

Understand Your Spending Habits

Knowing your spending habits helps you with the financial decisions of where and how to make changes and not lose money.

You can start by making a list of all the things you spend money on over the last three months and average them. Determine whether the spending you see corresponds to your priorities.

It is important to keep detailed records of your spending because the day-to-day charges are the ones you can quickly change compared to major costs like rent or mortgage repayments.Simplify the process of tracking and understanding your expenses by using the MMS Budget Planner Calculator. You can easily input your expenses and see the total amount you’re currently spending.

Knowing where to curb your spending habits can help you maximise cash flow, savings and your ability to grow the balance of your investments.

Maximise Cash Flow

When we create a budget and cut back on unnecessary expenditures, we expect our funds to increase and have more money to save or invest.

But sometimes, this thought crosses our mind:

I’m still not saving enough.

Outside of managing outgoings and taking on a new job or having multiple income sources, there are other ways to increase your funds.

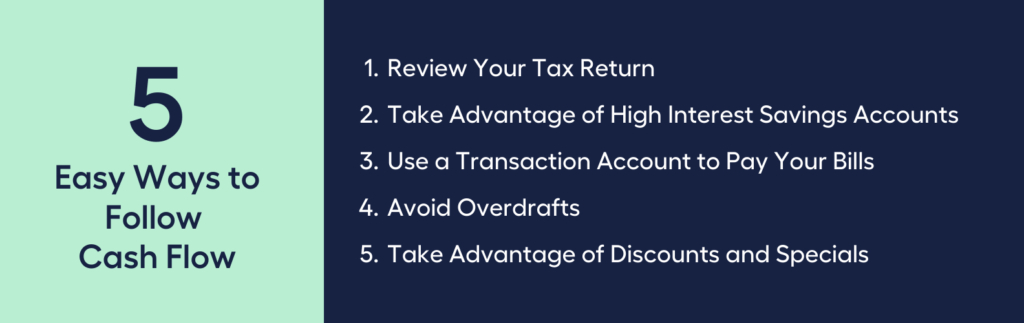

5 Easy Ways to Follow Cash Flow

- Review Your Tax Return

- Take Advantage of High Interest Savings Accounts

- Use a Transaction Account to Pay Your Bills

- Avoid Overdrafts

- Take Advantage of Discounts and Specials

Here’s the lowdown on how to make your cash flow:

1. Review Your Tax Return

Spend the time to take advantage of every tax deduction available to you and maximise the amount of each tax return. Get more of those dollars into your savings account.

2. Take Advantage of High Interest Savings Accounts

Shop for a savings account that offers a high interest rate and get one that has fewer fees. Although savings accounts are designed to encourage you to save, some also have high withdrawal fees which can be a great way to discourage you from withdrawing your savings.

3. Use a Transaction Account to Pay Your Purchases, Bills, and Credit Card

Transaction accounts don’t offer a high interest rate, but many don’t charge account fees. These are best for settling your daily, weekly, and monthly expenses. Open a transaction account separate from your savings account.

4. Avoid Overdrafts

A bank charges you overdraft fees if you withdraw more money from your account than you have in it. Some banks charge a high interest rate on overdrafts too. Interest charges and overdraft fees from ATM withdrawals or debit card purchases can pile up and drain your savings account.

5. Take Advantage of Discounts and Specials

If it doesn’t affect your available funds negatively, take advantage of early bird discounts on bill payments and search for special offers before purchasing necessary items. If you get into the habit of doing it, you can add significantly to your savings.

There are other tips to save more money sooner. The general idea is to pick those that suit your personality and create a habit of it.

Manage Debt

As you get ready to build your savings and investments, keep in mind that having debt is not bad—a mortgage can help you realise the goal of owning a home and may even help you build wealth if your home increases in value.

But owing too much money or having the wrong kinds of debt, like high-interest credit card debt, might make it difficult to achieve other investment objectives.

3 Steps to Manage Your Debt More Effectively

1. Take Account of the Money You Owe

2. Get an Update of Your Credit Report

3. Find Ways to Consolidate Debt

Let’s break it down.

Step 1: Take Account of the Money You Owe

Make a list of all your unpaid debts. Include the interest rates for each so you can identify which are costing you the most money.

Step 2: Get an Update of Your Credit Report

Ask one or more of the three credit reporting agencies to provide you with a free copy of your credit report. This helps you ensure that you haven’t overlooked any unpaid debts.

Also, it’s a good idea to check if there are any accounts there that you don’t recognise.

Step 3: Find Ways to Consolidate Debt

- Can you combine multiple loans with high interest rates into one with a lower interest rate?

Yes, this can be done.

One way to consolidate is to move various credit card balances to a single card with 0% interest. Check if you qualify for a credit card balance transfer.

- Are there any low-interest personal loans available for you to take out in order to pay off high-interest credit card balances?

Whichever path you choose, it is best not to incur additional debts until the old ones are paid.

Once you have checked all options, you can seek financial advice to create a strategy to settle your debts sooner and increase your savings.

Multiple Income Streams

There are two types of income that help achieve your long term financial goals or retirement plan:

Active Income and Passive Income.

Active income is when you work and get paid for it.

Passive income can be derived from different sources, including:

- Rental income form investment property

- Dividends from shares, payments from annuities, and interest from term deposits – all of which do not require the input of your time in order to generate income

Passive income is a great way to generate funds for your financial freedom or early retirement plan.

Generate Passive Income

Before we list the various ways you can generate money passively, do understand that it involves working upfront before earning income (continuously).

3 Basic Methods to Generate Passive Income

- Generate Funds from Rent

- Grow Your Savings Through Investments

- Take Advantage of Information Technology

1. Generate Funds from Rent

The money generated from a rental property is a passive income you can use to help build your retirement fund.

Generally, people think of a house or an apartment when rent is mentioned. But you can lease out other properties.

You can rent out a room, an extra parking space, rent out household items, and even rent out properties on a short term basis. There’s a market for all of these, and one of its benefits is it doesn’t affect the value of your property.

2. Grow Your Savings Through Investments

Depending on your objectives and financial situation you may find yourself investing in various investment accounts and financial products such as mutual funds and individual stocks.

Mutual funds or managed funds are a type of financial product that pools money from many different investors to invest in a variety of securities, including bonds, equities, money market instruments, and other assets.

Investing in a single mutual fund investment account allows investors to access investments and a degree of diversity that are typically out of reach for an individual.

Wealthier investors with a higher risk tolerance may look at investing in the share market themselves and buy shares from individual companies listed on the stock exchange.

Other investments where you can invest your hard earned savings are exchange traded funds (EFTs), investment bonds, real estate investment trusts (REITs).

Note that, unfortunately, it’s not always as simple as studying past performance of an investment product in order to have an idea of its future performance.

3. Take Advantage of Information Technology

The information age has provided both individuals and companies the opportunity to generate additional earnings passively.

You can do it too by doing the initial task of creating a product and allowing online companies to sell the products for you at a certain amount with minimal fees.

Investing your time in creating something you enjoy and earning from it adds to the fun.

How a Financial Advisor Can Help You Build an Investment Portfolio

With the wide variety of financial products available in the market, the simplest way to get started on your investment journey may be to seek financial advice. Without sound investment advice, there’s a greater risk of falling short of your timeline and emptying your retirement savings too early.

What if you could tap into the wisdom of an experienced financial adviser instead of taking the all too common ‘hit-and-hope’ approach?

Many people may be unaware of this…but just like you, 41% of Aussies intend to get financial advice rather than going it alone, according to an Australian Securities and Investments Commission (ASIC) report.

Find the right Financial Adviser for you with the help of My Money Sorted .

When you book a call with My Money Sorted, you’ll:

✓ get a better understanding of your money matters

✓ have an idea of the experts you can call on to help you reach your goals

✓ be matched with the right financial adviser who can help simplify your family’s journey to financial wellness

My Money Sorted is your stress-free pathway to getting ahead with your money. Here’s what your journey will look like:

Step 1: Start off with a quick money matters session with My Money Sorted

Step 2: Get matched with a licensed Finance Adviser that’s right for your money situation

Step 3: Take the first step towards your money goals with a clear and sound roadmap prepared by an experienced Financial Adviser

It’s that easy!

Start Building Wealth to Secure Your Financial Future by Speaking with My Money Sorted