We’ve all heard the saying, “don’t put all your eggs in one basket.”

It means not staking our entire future on the success or failure of one thing.

The concept of diversification revolves around combining a wide range of investments in an effort to lower your overall investment risk.

You have a residential home, and you’re still paying off your loan balance. You also have super and some cash invested in the share market, but now you’re considering property investment, an alternative investment that can bring in a steady stream of income.

You’re not alone. The Australian Taxation Office (ATO) has reported that more than two million Australians own an investment property.

Jump straight to…

What is an Investment Property?

An investment property is real estate purchased with the intention of earning a profit.

The profit can be a rental yield if you lease it to a resident or a business. It could also be future gains if the property is sold for a profit.

Most property investors get into investment property buying for both of these reasons.

Just remember:

So look for the right property, one that people will lease or rent now, or will want to buy in the future, rather than one you will reside in.

But before we dive into the ins and outs of investment property, let’s consider an important question:

Is it possible to buy another property while paying off an existing home loan?

Difference Between a Home Loan and an Investment Property Loan?

Do you know that buying an investment property is possible while paying off your home loan?

In fact, as a property investor, you can get a home loan for your investment property while paying off the loan on your owner-occupied residence.

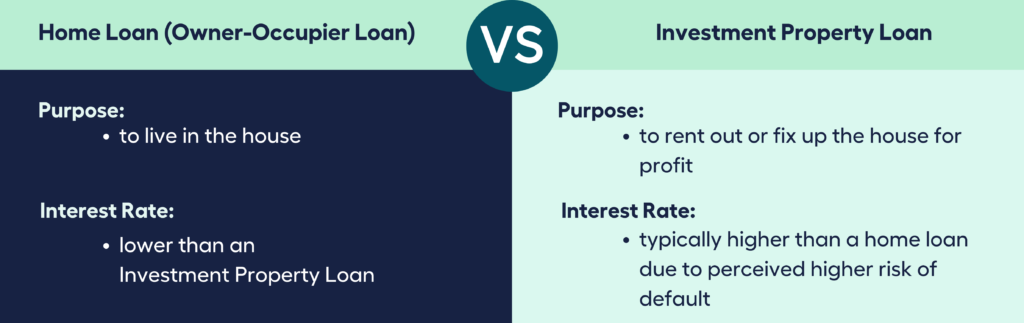

As the names suggest, the distinction between owner-occupied and investment properties is based on what you intend to do with them.

An owner-occupied property is one that you purchase with the intention of living in it.

It is considered an investment if you intend to rent it out or flip it.

If you intend to live in the house, you will require an owner-occupied home loan.

If you plan to rent out the house or fix it up to sell for a profit, you’ll need an investment home loan.

It is essential to differentiate between these two types of home loans because they are treated differently in terms of taxation and lending criteria.

And you must obtain a home loan that is appropriate for the type of purchase; otherwise, you may be charged with fraud.

An investment home loan typically carries a higher interest rate due to the perceived higher risk of default.

For taking on this perceived level of additional risk, the lender must be compensated and will rarely loan you the full amount required to purchase the property.

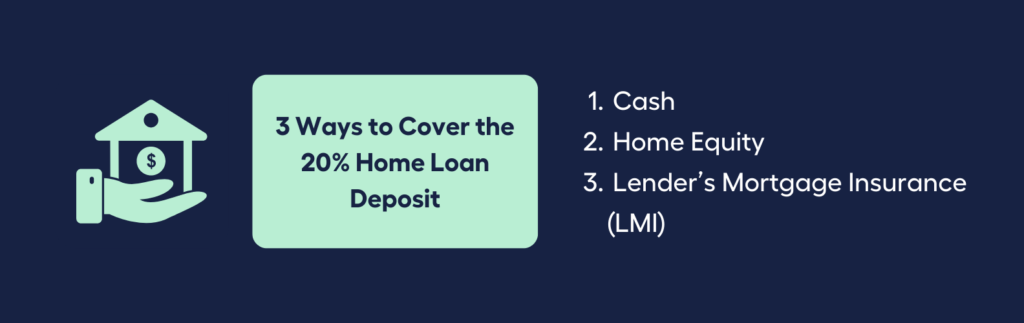

Do you need a 20% deposit for investment property?

Some lenders may only offer a maximum Loan to Value Ratio (LVR) of 80% due to stricter lending criteria for investments.

This means you only get a loan amount equivalent to 80% of the property price.

2

Shares

This means you must provide a 20% deposit, either through savings or equity from an existing property to get an investment loan approved.

In some instances, you may be able to use the equity in your residential home to cover the 20% deposit.

You can also get Lender’s Mortgage Insurance (LMI) if you don’t have a full 20% deposit.

LMI is an insurance policy that protects the bank if you are unable to make your monthly repayments. It’s usually either a one-time fee or a fee added to the loan amount.

So now you have three ways to cover the 20% deposit:

Cash, equity or LMI.

Can you get a 30 year loan on an investment property?

A 30-year loan on an investment property is possible. In fact, 30-year home loans are the most common type of loan for second homes.

However, 10-, 15-, 20-, and 25-year terms are also available.

These are the factors that can help determine the loan term that is best for your investment property:

- purchase price

- interest rate

- your monthly budget

- how long you intend to hold the property

How much should you borrow for an investment property?

Earlier, we mentioned that most lenders only offer a loan to value ratio of up to 80% of an investment property’s price.

So, you may be able to get a loan amount of up to $480,000 if you’re purchasing a property worth $600,000.

However, a loan to value ratio of 80% is not the rule.

You may be able to find a specialist lender willing to offer an LVR of up to 95%, which is what many lenders offer for owner-occupied home loans.

Just remember that lenders tend to view an investment home loan as riskier than standard home loans, and as such, you must be in good financial standing to qualify.

Is it harder to get a mortgage for an investment property?

While getting approved for an investment loan may appear difficult, it is not impossible.

Keep these basic lending criteria in mind:

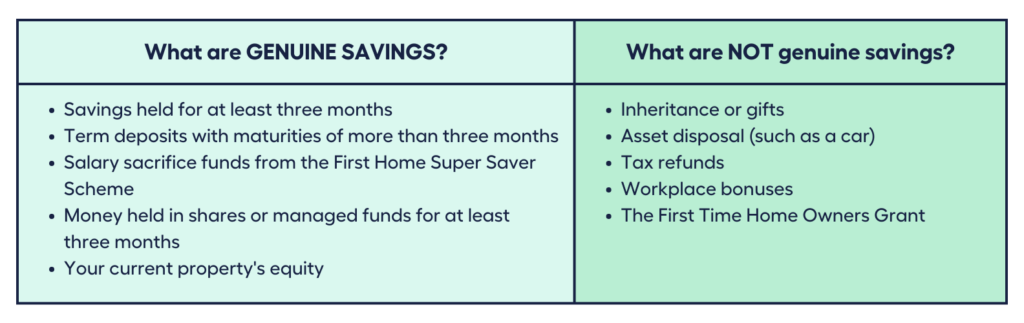

- You should have a minimum of 5% to 10% of the property value in genuine savings

- A favourable credit history

- A credit score that is above average

- Employment security

Lenders use the term “genuine savings” to describe savings that you yourself saved over a period of time, usually three to six months.

Now, before you take a chance on investing in real estate, it is best to prepare for it otherwise you could find yourself in the deep end searching for a way out.

How Do Beginners Invest in Real Estate?

Investing in a rental property is a significant financial commitment, and landlords who take the time to get professional advice and plan carefully before investing usually get the best results.

1. Know how long you intend to keep your investment property

Will this rental property be used as a primary residence or as a stepping stone to the purchase of additional investment properties?

2. Recognise your financial situation

Before looking at properties to invest in, it is critical to understand your capacity to pay back or service the loan even without rental income.

3. Know the neighbourhood

Speak with a local real estate agent or buyers advocate to learn about current market trends in the area and to gain a better understanding of property prices that are compatible with your financial situation.

- Recognise the rental market

Understanding the rental market, like understanding the location, will give you insights into what renters are likely to pay and can help you calculate your return on investment.

5. Determine your potential return

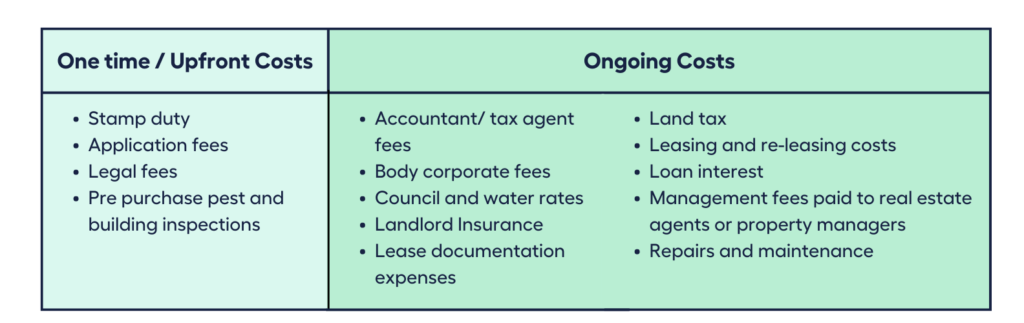

Determine the rent you will receive and be sure to take into account other expenses such as ongoing and upfront costs associated with real estate investing.

You’ll be ready to apply for your investment home loan once you have planned your strategy for real estate investing and budgeted for the associated costs.

You can learn about the various types of investment loans and their associated interest rates when you talk to our Finance Buddy.

I want to see all my options with the help of a Finance Expert

Book a FREE Call TodayThe Advantages and Disadvantages of Investment Property Loans

Real estate is an appealing investment opportunity for many Australians due to its potential tax benefits and the role in can play in wealth generation, but it is not without potential downsides.

Investing in real estate can be an effective way to accumulate wealth and secure your financial future if done correctly.

To be successful, this endeavour requires careful planning and unwavering commitment.

Advantages of Investment Property Loans

Here are some things to think about when investing in real estate:

- Capital Growth

Capital growth is the gradual increase in the value of an asset over time.

When looking to purchase an investment property, it’s critical to consider whether the neighbourhood or location’s value is anticipated to rise.

Look for suburbs with plans to accommodate population growth, such as the construction of schools and train stations.

If you do your homework, you may find yourself purchasing a property for less than its true market value.

- Rental Earnings

It is critical to ensure a consistent rental income stream.

You want to find a rental property with a high yield. This will assist you in covering mortgage repayments with rental income.

- Tax Deductions

Many property expenses, such as advertising to prospective tenants, loan fees, and maintenance costs, may be eligible for a tax deduction.

When your rental income is less than its expenses there may still be a silver lining.

Consult a tax advisor because an investment loss reduces your total taxable income, which has the potential to lower the amount of tax you would pay in a given year.

- Take the First Step to Owning a House

More first-time home buyers are opting for an investment property as their first step towards home ownership.

Purchasing an investment property is an excellent way to get on the property ladder while continuing live and rent in a desirable area.

Disadvantages of Investment Property Loans

Here are some challenges to investing in real estate:

- Inadequate Liquidity

If you have an immediate need for funds in the event of an emergency, you cannot expect to immediately cash in your investment.

It is essential to understand that property investment is a long-term strategy that entails purchasing and holding the property over the long term. You should not expect to realise ‘quick’ financial gains.

- Costly Entry and Exit Fees

The high cost of financing is one of the most significant barriers to many Australians investing in property.

A deposit alone can range from tens of thousands to hundreds of thousands of dollars.

When purchasing an investment property, stamp duty, legal fees, and insurance coverage can be costly.

Exit fees, such as capital gains, must also be considered.

- Ongoing Expenses

Home loan repayments, council rates, maintenance and renovation costs, and insurance are just a few of the potential ongoing costs of owning a property.

Be aware of your expenses if you wish to avoid negative gearing.

Negative gearing happens when expenses on your investment property are more than the rent it brings in.

A good long-term investment plan is one where the rental income from your property exceeds all recurring costs.

- Vacancy Rates and Bad Tenants

If you don’t have a tenant, you may have to cover the monthly loan repayment yourself for the duration the property is vacant.

You can also have a nightmare dealing with bad tenants.

Bad tenants cause emotional stress, and their actions can result in financial losses, if they consistently fail to pay rent or cause damage to your property.

What makes a good investment property?

Setting aside the benefits and drawbacks, certain factors can make or break you as a property investor. When looking for a home, careful planning and due diligence are essential, especially if it is your first investment property.

What if you could launch your investment journey with the guidance of an experienced finance expert instead of taking the all too common ‘hit-and-hope’ approach?

Many people may be unaware of this…but just like you, 41% of Aussies intend to get financial advice rather than going it alone, according to an Australian Securities and Investments Commission (ASIC) report.

Learn how to choose the best possible investment options that match your financial goals and situation by consulting with qualified finance experts like a financial adviser.

Find the right Financial Adviser for you with the help of My Money Sorted

When you book a call with My Money Sorted, you’ll:

✓ get a better understanding of your money matters

✓ have an idea of the experts you can call on to help you reach your goals

✓ be matched with the right financial adviser who can help simplify your family’s journey to financial wellness

My Money Sorted is your stress-free pathway to getting ahead with your money.

Here’s what your journey will look like:

Step 1: Start off with a quick money matters session with My Money Sorted

Step 2: Get matched with a licensed Mortgage Broker that’s right for your financial situation

Step 3: Take the first step towards your money goals with a clear and sound roadmap prepared by an experienced Financial Adviser

It’s that easy!