Are you planning to move into a new home?

Whether you’re looking to upgrade or scale back, your dilemma could be which step you should take first:

Buy a new property OR sell your current home?

Jump straight to…

Perhaps you’re thinking that you can’t buy a new home until you’ve sold your old one.

But do you know that there’s a way out of your current dilemma?

It’s a system called simultaneous settlement.

Keep on reading because this article serves as a guide to selling and buying a home at the same time.

What is a Simultaneous Settlement?

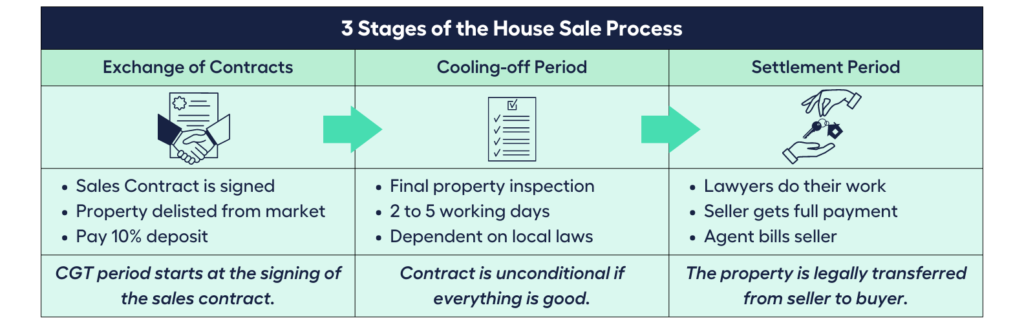

Settlement is the final step in the process of transferring property ownership.

Simply put, settlement is when the buyer pays the seller the remaining balance of the asking price and receives the keys to their new home.

It normally happens a few weeks or months after the sale contracts are exchanged and a deposit is paid.

A simultaneous settlement is one in which the settlements for the sale of your current property and the purchase of your new property take place simultaneously.

Here are the possible scenarios without a simultaneous settlement:

Scenario 1:

You sold your house but have not completed the purchase of a new property. You may have to temporarily rent another place until you are able to buy and move into a new one.

Scenario 2:

You bought a new house without selling the old one. You will be paying a mortgage on two properties.

With a simultaneous settlement, you can avoid putting yourself in any of these two scenarios. You don’t have to pay rent on a house while you’re looking for a new one to buy, and you don’t have to pay home loans on two properties at once.

Sounds wonderful, but there’s a downside.

If one of the settlements is delayed, this can cause problems!

Since both settlements depend on one another, if one of them has a slight problem, the entire transfer may be delayed.

If the issue results in a significant delay, you could be forced to pay penalty interest, or worse still you can even lose your deposit!

Buying a House If You Haven’t Sold Yet?

If that is your game plan, your thought could be:

Why not buy a house first?

In this scenario, you first purchase the new property and afterwards sell the old one. You will then be the owner of two properties at the same time and might have to temporarily pay two mortgages.

Imagine this:

Paying principal and interest repayments on TWO properties.

Ask yourself:

Can I afford to start paying for the home loan of my new property while continuing to make home loan repayments on my previous mortgage?

If your answer is NO, you can use a bridging loan to cushion the weight of paying two home loans.

A bridging loan is a short-term loan you can use until you have the money from the sale of your existing house to pay for your new home. It allows you to temporarily own both properties, and most of the time, the interest is capitalised (added to the loan) until you are able to sell your old property.

However, this option is not for everybody.

Typically speaking a bridging loan is only available to people who own 40% or more of the value of their home. Lenders won’t give you a bridging home loan unless you have a lot of equity in your home.

The main benefit of a bridging loan is that you can buy a home now, move into it, and it buys you time to sell your old home.

The downsides are that you’ll have to pay a lot of interest while you own both properties, you need a lot of equity to get a bridging loan, and you usually have to sell your home within a short loan term.

| Bridging Home Loan | |

| Benefit | Downside |

| You can buy a home now and move into it | You have to pay a lot of interest while you own both properties |

| It buys you time to sell your old home | You need at least 40% equity to qualify for a bridging loan |

| You have to sell your home within a short loan term |

Buyer beware:

Unfortunately, a lot of people who opt for this strategy don’t truly have the money to own both residences simultaneously!

As a result, their bank rejects their loan application, or they are compelled to quickly sell their old home, frequently for less than its market value.

Be sure you have sufficient funds so you can stick to the bridging loan terms, are able to sell your old house and settle its mortgage. This way, your loan repayments will decrease since you will just be paying for one mortgage instead of two.

Why not sell your current home first?

In this scenario, you sell your existing home before buying a new one.

You will need to decide where you will live in the meantime if you decide to sell your current property before buying a new one. This could entail staying with friends or relatives or renting a place until you can find a new home to buy.

However, it’s possible that you’ll be able to continue living in the house you just sold for some time.

You and your home buyer may enter into a “lease-back” agreement whereby you agree to continue living in the home for a predetermined amount of time in exchange for paying rent to the new owner. You might have to agree to a reduced asking price to entice the buyer to go along with this plan.

The benefit of this approach is that you won’t have to take the risk of agreeing to buy a new property without having a deposit ready because the money from the sale of your house will already be in your bank account.

- Selling your current home first can be a good option for buyers who don’t have much equity in their present house (you owe more than 80% of the property value), as you won’t be eligible for a bridging loan.

How Do You Buy and Sell at the Same Time?

Simultaneous settlement eliminates timing issues such as having to meet the cost of two mortgage repayments or renting a place, and may result in cost savings for you. If everything goes according to plan, you settle on the sale of your old home and move into your new one at the same time.

Your previous mortgage will be paid off with the proceeds from the sale of your existing property, and any remaining money will be used to lower the mortgage on your new house.

The Process of Simultaneous Settlement

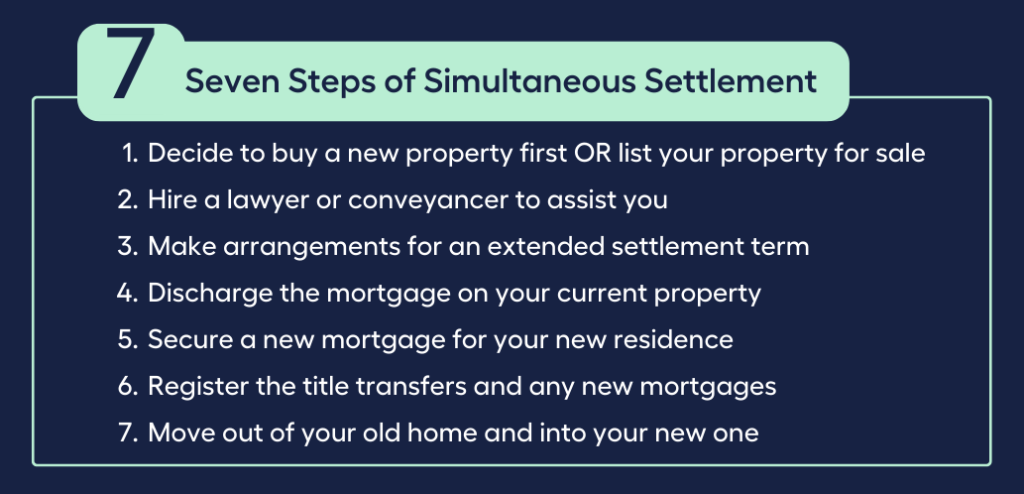

There are seven steps you need to do to complete a successful simultaneous settlement process.

Step 1

Decide to Buy a New Property First

OR

List Your Property for Sale

Knowing if you’re buying a property first or listing your property for sale is important because it will help mortgage brokers and conveyancers to devise the right simultaneous settlement plan for you.

Being decisive from the start will lower your chances of taking on two home loans or ending up renting a place because the timing didn’t work out.

Step 2

Consider Hiring a Lawyer or Conveyancer to Assist You

Due to the complexity of the settlement process, it is worth considering hiring a lawyer or conveyancer to assist you. A simultaneous settlement requires proper timing.

You should get paid at the right time so you can pay for your new home on time. Your conveyancer will ensure that your deeds of transfer, clearing of an existing loan, and taking on a new loan happen in a timely manner so that you avoid penalties.

Step 3

Make Arrangements for an Extended Settlement Term

If at all possible, make arrangements for an extended settlement term for either the sale or the acquisition of property.

For instance, if you decide to purchase a new home first, you can request an extended settlement period to give yourself more time to sell your existing home.

However, if you decide to sell your current residence first, you’ll have to bargain for additional time to look for a new residence before you can settle.

An Extended Settlement to give you more time to Look for a New Home (Sell Your Property First)

Most people who do simultaneous settlement sell their property with a long settlement of up to 6 months.

Their sales contract includes a clause that lets them move the settlement date up as long as they notify the other party four weeks in advance.

Then, they look for a new home to buy. When they find one, they can move the settlement date on their old home up so that both homes settle on the same day.

The only risk is that you might have to move out of your old home and rent if you don’t find a home to buy on time.

An Extended Settlement to Sell Current Property (Buy a Property First)

Some people buy a new home with a long settlement period of 6 months and a clause that lets them bring the settlement date forward.

Then, they can sell their old home and move up the settlement date on their new home so that it matches the date they sold their old home.

The risk of this choice is that if you don’t sell your home within the agreed period, you might lose the deposit on the new home.

| Two Types of Extended Settlement | |

| Sell Your Property First | Buy a Property First |

| Agree on a price and sign the contract to sell | Agree on a price and sign the contract to buy |

| Get the 10% deposit | Pay for the 10% deposit |

| Look for a house to buy | Look to sell your current property |

| Agree on a price and sign the contract to buy | Agree on a price and sign the contract to sell |

| Pay the 10% deposit | Get for the 10% deposit |

| Bring forward the settlement date | Bring forward the settlement date |

Step 4

Discharge the Mortgage on Your Current Property

Most of the time, it takes between 12 and 15 working days to discharge (pay off) an existing home loan, but this depends on your lender.

Here’s the Process for Discharging a Home Loan:

1. Inform your lender that you want to settle your mortgage.

2. Lender will ask you to fill out a form called a “discharge authority form” to get the process started.

3. Fill out the discharge authority form correctly and send it back to the lender as soon as possible.

To avoid making mistakes, you could ask your mortgage broker to help you fill out the form, or you could go to your lender’s office to fill out the form there.

4. After you send in the discharge authority form, your lender will make the “discharge of mortgage document”.

This document needs to be registered at the Land Titles Office in your state. Most lenders will do this for you, but you can do it yourself if you want to. If you decide to register the document on your own, go to the website of your state’s Land Titles Office to ensure you do t the right. This will save you time and trouble.

Step 5

Secure a New Mortgage for Your New Residence

If necessary, secure a new mortgage for your new residence. This wouldn’t be your first time getting a home loan, nevertheless, it’s best to freshen up on what you need to do.

Interest rates are important when looking for a good deal on a home loan.

Remember:

A home loan is a long-term debt, so even a small difference in interest can add up over time.

Compare rates for home loans

Talk to at least two different lenders to find home loan options that fit your needs. Even an interest rate 0.5% lower from one lender to the next could save you a lot of money over time.

If you need help, ask for it.

Since there are so many lenders and loan options to choose from, you may benefit by working with a mortgage broker to help you find the best loan options.

Pay Lenders Mortgage Insurance (LMI) or the Required Deposit

Another reason why buyers need mortgage brokers is because they can get the best home loan terms and interest rates for their clients and help avoid lenders mortgage insurance, which helps save money.

Get pre-approval to buy

Consider getting loan pre-approval from a lender. Lenders will ask for proof of your current finances so they can figure out if you have the financial capacity to pay back the loan.

Pre-approval lets you know the maximum amount you can borrow and is typically valide for a period of 3–6 months.

It doesn’t lock you into taking out a loan. It lets you set a price range that you can afford and shows sellers and agents that you are serious about buying.

Step 6

Register the Title Transfers and Any New Mortgages

Register the title transfers and any new mortgages with the land titles office of your state or territory. Here is when you need your conveyancer’s help.

Step 7

Move Out of Your Old Home and Into Your New One

Congratulations!

This is the settlement day. All your paperwork is in order, and everybody involved in the buying and selling of two properties is happy.

Do you know what it takes to make simultaneous settlement a success?

The process requires good negotiation skills and typically a willingness to sell your property for less than it is worth or to purchase your new property for more than it is worth.

This way, the other party will be more motivated to accept the lengthy settlement timeframe.

Enlist the assistance of knowledgeable experts like a real estate agent, a conveyancer or solicitor, and a mortgage broker to help you work though what can be a hefty amount of paperwork and a tricky process.

Are you keen on exploring the option of going through a simultaneous settlement, but you have no idea where to find the right experts who can guide you through the meticulous process?

- Did you know you can have a free, no-obligation chat with My Money Sorted? My Money Sorted can connect you with the experts who are a good fit for your situation.

The Pros and Cons of Simultaneous Settlement

We’ve had a thorough discussion on the simultaneous settlement process and along the way mentioned some pros and cons of the process. Let’s identify them again just to make sure what we’re getting into is clear.

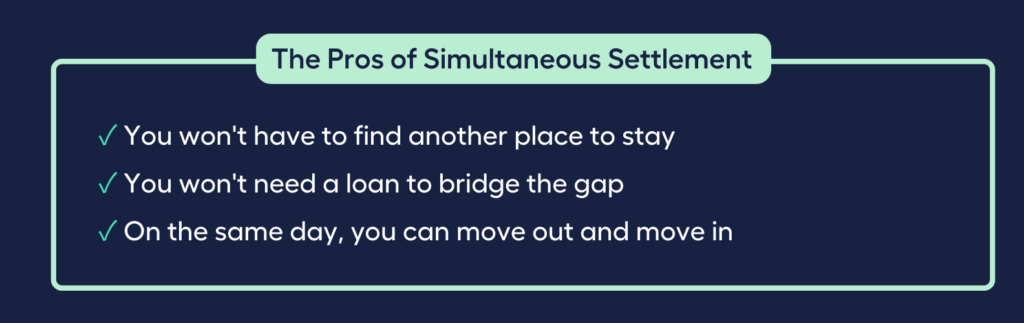

The Pros of Simultaneous Settlement

You won’t have to find another place to stay

One of the best things about simultaneous settlement is that you can move right into your new home. This means you won’t have to worry about renting a place, or staying with friends or family, or having to store your furniture, which is usually a problem if you sell first.

You won’t need a loan to bridge the gap

If you buy a new house before selling your old one, you will usually have to pay for two mortgages: one on your old house and one on your new one. Most of the time, the second mortgage will be a “bridging loan”. This can be expensive, and because most bridging loans have a time limit (usually no more than 12 months), you may feel rushed to sell.

On the same day, you can move out and move in

In a simultaneous settlement scenario, the properties are usually given to the new owners on the day of settlement or, if necessary, the next day. This means that, unless you are moving a long way away, you can move out of your old home and into your new home on the same day. This will save you money on moving costs and keep you from having to store your things temporarily.

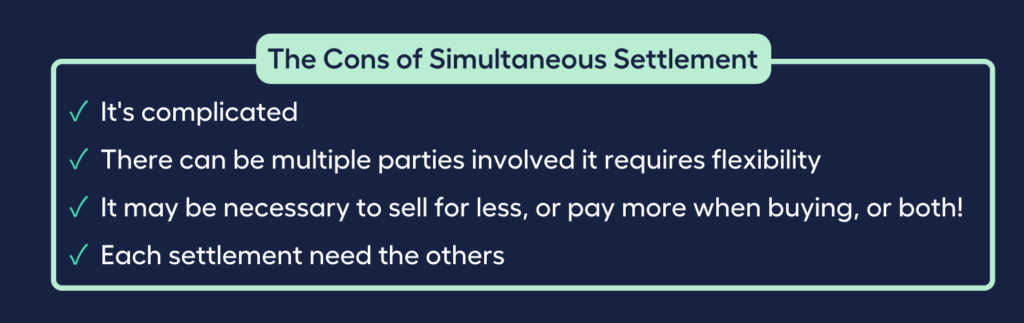

The Cons of Simultaneous Settlement

It’s complicated

Most people hire a lawyer or conveyancer because the financial and legal process is pretty complicated.

There can be more than one person or group involved

There may be a lot of people who need to pay and be paid, and the timing could be tricky.

For example:

The person who buys your old property will owe you money, and you will owe money to the seller whose property you just bought. Plus, both your lender and the lender of the other party will want their needs to be met. Under the terms of the sales contracts, real estate agents may also need to be paid.

It needs flexibility

Most of the time, you will need to try to negotiate a longer time to pay.

If you sell your home first, you can ask for a longer settlement period from the buyer, like six months, which should give you enough time to find a new place to live. But getting the other party to agree to this may be difficult.

If you buy first, you might be able to make your purchase “subject to the sale of your current property”. This means that you won’t have to move into your new home until you’ve sold your current one. Again, though, the seller may not easily agree to this condition, especially in a “seller’s market” where properties are in high demand.

It may be necessary to sell for less, or buy for more, or both!

For a simultaneous settlement to go through, you might have to give up something.

For example:

You might have to sell your home for a little less than you wanted and pay a little more than you planned to for your new home.

Each settlement is dependent on the other

If there is a problem at either end, it could cause delays, possible penalty fees, or even the loss of the deposit on your new home. And if there is a chain of settlements, there can be even more trouble.

If you talk to the right people, the simultaneous settlement process will go more smoothly.

If you have a good real estate agent and lawyer, you’ll get the information you need to make good decisions.

If you’re entering into a simultaneous settlement, you’ll need a very experienced conveyancer, and if you’re using a bridging loan, seeking the guidance of an expert mortgage broker can help make the process less stressful.

You may have reached this far in reading this article because you are truly interested in simultaneous settlement.

Have all your questions been answered?

If you’re still having doubts or simply need information to help you navigate the process, talk to My Money Sorted for free!

Many people may be unaware of this…but just like you, 41% of Aussies intend to get financial advice rather than going it alone, according to an Australian Securities and Investments Commission (ASIC) report.

Find the right Mortgage Broker for you with the help of My Money Sorted.

When you book a call with My Money Sorted, you’ll:

✓ get a better understanding of your home loan options

✓ have an idea of the experts you can call on to help you reach your goals

✓ be matched with a mortgage broker who can help develop the best home loan strategy for your situation

My Money Sorted is your stress-free pathway to getting ahead with your home loan.

Here’s what your journey will look like:

Step 1: Start off with a quick money matters session with My Money Sorted

Step 2: Get matched with a licensed Mortgage Broker that’s right for your financial situation

Step 3: Take the first step towards your financial goals with a clear roadmap that makes sense prepared by an experienced Mortgage Broker.

It’s that easy!

Is simultaneous settlement the right course of action for you? Contact a My Money Sorted to find the best financial advice.