Like many Australians entering the property market, you’re probably grappling with the choice between buying a first home or an investment property.

Meet Alex, a 35-year who dreams of having a place to call his own. However, the continuous threat of rising interest rates leaves him pondering his ability to meet his home loan.

Imagine committing to a half-a-million-dollar home loan, and suddenly, your weekly mortgage repayments jump by an additional $150, stretching your budget thin.

This scenario is all too common, especially if the chosen home lacks potential for market or location growth. Join us as we explore financial aspects, loan eligibility, costs, and potential returns, offering insights to help you make smart decisions for your financial future.

Jump straight to…

First Time Buying Property & Unsure If You Should Be Buying an Investment Property Before Your First Home? Read on!

Facing the dilemma of buying your first home or an investment property?

It’s a pivotal choice, laden with considerations. On the one hand, owning a home provides stability and a sense of security, while on the other hand, buying an investment property can generate rental yield and property value appreciates over time.

To help you make an informed decision, we’ve compiled a list of factors to consider when deciding between buying your first home or an investment property as many Australians are torn with these two.

This decision isn’t just about bricks and mortar; it’s about sculpting your financial future.

We understand the magnitude of this choice, and that’s why we’re here to guide you through the labyrinth of options. We’ll guide you in your home buying journey by uncovering the pros and cons of both paths, helping you weigh the scales and make an informed choice.

The Pros & Cons of Buying a First Home

The Australian Dream of home ownership has traditionally been associated with security and stability. With growing property prices, however, many people are beginning to wonder whether purchasing a home is the best decision for them.

Renting, on the other hand, provides flexibility and financial rewards while also making people feel unstable and transient. We will look at the advantages and disadvantages of buying your first home in Australia to help you make an informed decision.

Pros of Buying a First Home

Undoubtedly, Australia’s housing market is booming, especially in Sydney and Melbourne, maintaining strong conditions with a continuous upward trend in property prices.

Meanwhile, market conditions in cities such as Brisbane have stabilised, and there are signs of increased home turnover.

There are numerous benefits to exploring the Australian real estate market. While the robust market is a compelling factor, there are also several other compelling reasons to consider a property purchase.

Lower Entry Cost via Grants & Schemes

In Australia, there are numerous government grants and schemes available to first-time home buyers. Because each programme has slightly eligibility criteria and benefits, it is critical to consult the respective state government website for further information.

Here are some of the ways first-time buyers can access financial assistance:

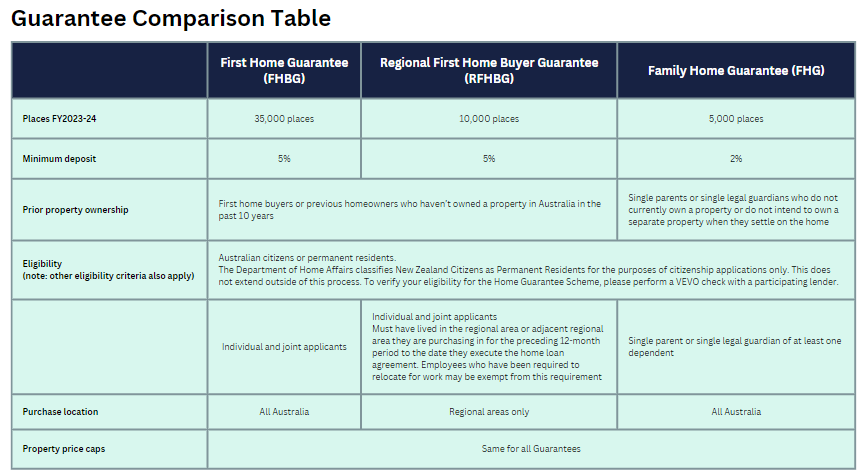

The Home Guarantee Scheme (HGS)

The Home Guarantee Scheme (HGS) is a government-backed initiative designed to help eligible first-time home buyers take that exciting step into homeownership sooner. Administered by Housing Australia on behalf of the Australian Government, the HGS offers distinct Guarantees to cater to different needs and circumstances:

- First Home Guarantee (FHBG)

Are you dreaming of your first home? The FHBG has your back, allowing eligible home buyers to purchase their dream home with a minimal 5% deposit. For the fiscal year 2023-24, there are 35,000 spots available to make your dreams a reality.

- Regional First Home Buyer Guarantee (RFHBG)

If you’re considering a home in a regional area, the RFHBG is here to assist you. This Guarantee supports eligible regional home buyers to secure their new home with a mere 5% deposit. In the fiscal year 2023-24, 10,000 spots are waiting for you in regional areas.

- Family Home Guarantee (FHG)

Single parents and single legal guardians with at least one dependent can now step into homeownership with just a 2% deposit. The FHG is tailored to your unique situation. In the fiscal year 2023-24, 5,000 places are available to help you create a stable home for your family.

*Note that the New Home Guarantee (NHG) is no longer available. Nevertheless, if you reserved an NHG spot on or before June 30, 2022, you can proceed with the settlement, provided you meet the eligibility criteria and comply with NHG requirements and timelines.

First Home Super Saver Scheme (FHSS)

For tax-savvy individuals looking to own their first home, the First Home Super Saver Scheme (FHSS) is your golden ticket. With FHSS, you can leverage your home deposit savings by tapping into your super fund. You can make voluntary contributions into your super fund, both pre-tax and post-tax. These contributions can be the key to your dream home.

Under FHSS, you can withdraw up to $50,000 from your super fund for your home deposit. However, there’s a limit on how much you can withdraw in a single financial year – $15,000.

You can expect access to your funds within 15 to 20 days, making your home ownership journey a reality in no time.

It’s important to note that if you have any outstanding debt with the Australian Taxation Office (ATO) or another Commonwealth agency, your withdrawal amount may be adjusted to repay the debt.

The FHSS is a tax-smart strategy for first-time home buyers.

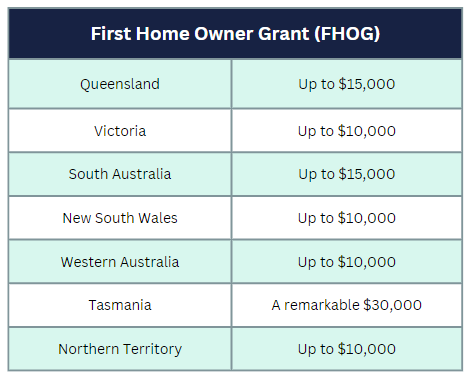

First Home Owner Grant (FHOG)

If you’re a first-time buyer looking to purchase a new house, the First Home Owner Grant (FHOG) is your greatest buddy. The FHOG differs by state, but it can provide you with up to $30,000 in financial support to help you build or buy a new house. It is accessible throughout Australia, with various award amounts depending on your location:

Here’s the best part: the FHOG is entirely tax-free, so you won’t have to include it as taxable income on your annual lodgement. Don’t miss out on these valuable opportunities to make your homeownership dream a reality. Be sure to check your state’s website for more detailed information on these incredible programs.

To determine your eligibility for the grants and schemes mentioned, you may check the following eligibility tool by Housing Australia. Please be reminded that this is general advice and does not constitute eligibility determination. You may seek the help of a professional mortgage broker for assistance and to discuss individual circumstances.

Help to Buy Scheme

In 2024, the Australian government is launching the Help to Buy Scheme, a fantastic opportunity for eligible first-time buyers to co-purchase a home with government support.

This project gives a substantial boost, guaranteeing 30% equity for existing homes and a hefty 40% equity for new dwellings.

Potential as a Future Investment Asset

Australia’s property market drives economic growth and job creation, making it a profitable investment platform.

Furthermore, the different grants and schemes provided by the government, along with the tax incentives for first time home buyers can significantly reduce the amount of funds needed to secure a property, making it easier for first home buyers to enter the property market.

Owning a home can also provide a potential for capital growth over time. It can help you accumulate wealth that you can pass on to your offspring or use as collateral to purchase a second house.

Additionally, using the equity from your first property to buy your second can help you establish a property portfolio and rent out your investment properties.

Stability and security

Australia’s stable democracy protects property rights, providing stability and security. Apart from that, its real estate market as well as its economy is booming.

The country’s property market is also known to offer long-term financial advantages, which in turn provides an ideal platform for investment, building activity, and employment.

Also, having a place to call home and make memories with their loved ones, provides first time home buyers a long-term solution for their housing needs.

Tax Benefits

There are tax advantages when purchasing a home in Australia depending on the state or territory you’re in, as well as your individual circumstances. It’s recommended to seek professional advice from a tax accountant or financial advisor to determine your eligibility for these benefits. The possible tax benefits for owner-occupied properties are the following:

- Stamp duty concessions

Stamp duty is a tax levied by each of Australia’s state and territory governments on the sale of certain types of property (including real estate and motor vehicles).

The tax, often known as “transfer duty” or something similar, assists in covering the expense of transferring a property’s legal title from one owner to another.

Stamp duty exemptions are state-based incentives; you should check regional government websites for specific state and territory tax incentive programmes, as well as eligibility if you qualify.

For example, in New South Wales, first-time home buyers can receive a full exemption on stamp duty for homes valued up to $800,000, while in Victoria, eligible buyers can receive a concession on homes valued up to $600,000.

- First home super saver scheme

Although not a tax exemption per se, the First Home Super Saver (FHSS) scheme allows you to make voluntary contributions to your super to help save for your first home through voluntary concessional (before-tax) and voluntary non-concessional (after-tax) contributions to your super fund.

You can reduce your taxable income by salary sacrificing your first home savings into super. You can also pay less tax on FHSS earnings compared to traditional bank accounts and enjoy higher returns on contributions.

Your super is taxed at a mere 15%, plus a few extra percent upon withdrawal – potentially less than your regular tax rate, accelerating your savings.

What’s more, if you’re purchasing a home with a partner or flatmate, they can also supercharge their savings by adding up to $15,000 per year to their own super as long as they meet the criteria.

- Tax Deductions for Homeowners

If you’ve set up your working space in your own home or are using a room or another part of your home for running a business, you may be eligible for certain tax deductions.

You can claim a tax deduction on the costs incurred in operating the business or claim tax deductions on depreciating assets.

Strong Real Estate Market

A strong real estate market makes a home a potential future investment asset due to several reasons.

- Diversification

Real estate is a great way to diversify an investment portfolio and offset the risk of high-risk investments, such as money invested in the stock market.

- Appreciating Asset

Investing in real estate long-term provides an appreciating asset that usually bounces back if held onto long enough.

- Passive Income

Should you wish to rent out your property or a portion of it to a tenant, real estate can generate passive income, which can be useful closer to retirement.

- Equity

Investing in properties can give property owners access to equity, which can be used for additional expenses or to create even more passive income from investment.

These factors make real estate a compelling investment opportunity for those looking to diversify their portfolio and generate long-term gains.

Cons of Buying a First Home

While the dream of owning your first home is exciting, it’s essential to be aware of the potential hurdles. In this article, we’ll explore the cons and challenges that come with buying your first home in Australia, equipping you with the knowledge to navigate this significant financial milestone.

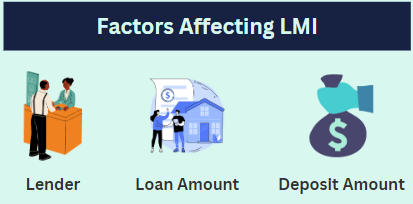

Lender Mortgage Insurance

Lenders’ Mortgage Insurance (LMI) is an insurance that protects the lender rather than the borrower. It protects the lender in the event that the borrower defaults on their home loan repayments.

It is a one-off payment shouldered by the borrower if the home loan is more than 80% of the property value or simply put, when a borrower’s downpayment is less than 20% of the property value.

This insurance can definitely have an impact on your mortgage and overall financial situation so it’s crucial to understand its ins and outs.

Although you don’t need to arrange the LMI yourself as your lender will sort it out for you, it’s good to be informed of the factors that affect the LMI cost. LMI does not have a fixed amount and can substantially vary depending on certain factors such as:

- The loan amount

- The lender

- The size of the deposit

In general, the lower your deposit and the greater your loan, the higher your LMI premium. Furthermore, some properties are deemed riskier by insurers, which might result in higher premiums.

There are several online calculators available that can produce an estimate based on your individual circumstances to give you an idea of how much LMI might cost you. Just keep in mind that these calculators are simply estimates, and your actual premium may differ. To get a more accurate price, always speak with your lender or mortgage broker.

There are also instances where you may qualify for an LMI waiver. You may consult with your lender or mortgage broker to see if you may be eligible.

Property Costs & Maintenance

The high upfront fees are one of the most significant disadvantages of home ownership.

These include the mortgage deposit, which can be as much as 20% of the total loan amount. This may put the great Australian dream out of reach for first-time homebuyers.

Then there are the ongoing interest payments, which can total hundreds of thousands of dollars over the life of the loan.

Our dreams for our first home are frequently much larger than our savings accounts can accommodate. According to the Australian Bureau of Statistics (ABS), the median dwelling price in Australia’s combined capital cities is now $923,641. The median unit price in the capital cities is $647,148 and the median dwelling value in the combined regional areas is $595,940.

A basic bank home loan would typically require a deposit of between 10% and 20%, implying that you will need to save between $50,000 and $100,000.

Maintenance and repairs might become a costly strain for those who are already struggling to repay their home loans.

When you rent, your landlord covers these occasionally unplanned costs, but as an owner-occupier, you must foot the tab.

You are responsible for the maintenance and repairs of your property as a homeowner. This can be a time-consuming and costly obligation, especially for first-time home buyers who may lack the essential skills or experience.

Other Potential Disadvantages

Buying a home can have other potential disadvantages, such as the risk of falling home values, rising interest rate, negative equity, and the uncertainty in the property market.

Falling home values

Purchasing a property in a declining market may result in the property being worth less than the purchase price.

Although this is only an issue if the owner plans to sell quickly, it can be a concern for first-time home buyers.

Rising interest rates

Rising interest repayments as a consequence of rising interest rates might cause problems for house buyers because their debt multiplies in line with expected cash rate increases.

This can raise the cost of homeownership and make it more difficult for first-time house purchasers to make mortgage payments.

Potential for negative equity

If the value of your property falls and you owe more on your mortgage than it is worth, you may be in a negative equity situation.

This might make selling your house or refinancing your mortgage difficult, and it can be a financial strain for first-time home buyers.

Uncertainty in the property market

The property market can be volatile, and there is always the possibility that the value of your home will decrease.

This can be a source of concern for first-time homebuyers, who are making a long-term financial commitment and may be more exposed to market shifts.

The Pros & Cons of Buying an Investment Property

Buying an investment property has long been a popular avenue for building wealth and securing financial stability.

Australia with its vibrant economy, stunning landscapes, and a strong demand for rental properties offers a diverse range of opportunities in the property investment market.

However, before you jump headfirst into the property market, it’s crucial to weigh the pros and cons that come with it.

Pros of Buying an Investment Property

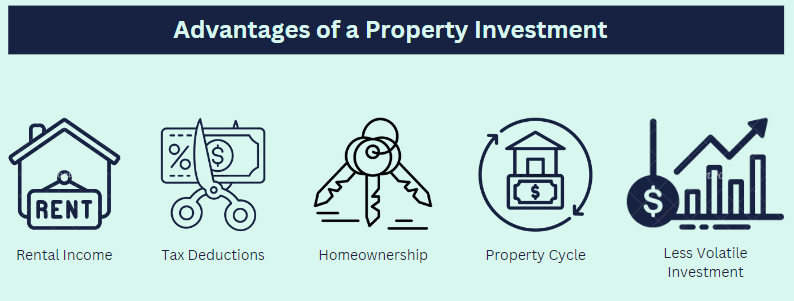

Investing in Australian real estate offers an array of advantages. With a stable economy and a strong demand for rental housing, you can expect a reliable stream of rental income.

Additionally, the country offers a transparent legal framework and high rental yields to a diverse market and the possibility of tax deductions, the pros of buying an investment property in this country are not to be overlooked.

Rental Income

Rental income is a significant benefit of owning an investment property. You can save more and fund your future home or next investment with the extra passive income. This can help you as an investor to accumulate wealth and attain your financial objectives more quickly.

Securing good tenants for your investment property can generate valuable rental income, which can be instrumental in covering mortgage repayments and property ownership expenses.

It’s essential to keep in mind that having your property tenanted is a positive step, but it doesn’t automatically guarantee a profit.

The trend of rentvesting, which involves buying and renting out your investment property while you rent a home in a preferred location with great amenities also shows potential and is popular among the younger population, especially first time home buyers.

Rentvesting is suitable for people who want to own an investment property and receive rental income for a secure financial future.

Tax Deductions

Purchasing an investment property can result in substantial tax savings.

- Depreciation

Depreciation is a tax break introduced by the Australian Taxation Office (ATO) that allows property investors to recoup the loss in value of their property and its fittings. First-time homebuyers can possibly claim up to 60% of the total purchase price by getting an ATO-compliant tax depreciation report. For a new home, such as an apartment, this can result in tax savings of more than $200,000 over a 40-year period, with the majority of the advantages realised in the years immediately following the property acquisition.

- Negative gearing

Negative gearing is a tax strategy that allows investors to borrow money to acquire an investment property where the rental revenue falls short of the property’s expenses. The investor can deduct this loss from their other income, such as their wage, as a tax deduction. This can result in lower taxable income and, as a result, lower tax liability.

- Capital Gains Tax

When an investor sells an investment property for more than the purchase price, they are subject to capital gains tax (CGT). However, if the property is owned for more than a year, investors may be eligible for a 50% CGT deduction, lowering their overall tax liability.

- Stamp Duty

Stamp duty is a tax levied on real estate purchases. When purchasing an investment property, first-time homebuyers may be eligible for stamp duty discounts or exemptions, reducing the financial burden connected with the acquisition.

To take advantage of the entire range of tax benefits available when purchasing an investment property, it is critical to hire a certified depreciation specialist to provide a detailed depreciation report for the property.

Make sure the organisation you choose for the depreciation report is officially recognised as a tax agent by the Australian Taxation Office (ATO).

For investors to be eligible for tax benefits, the tax depreciation report must correspond to the ATO’s stated requirements. As a result, investors should check the qualifications of their chosen tax depreciation firm and confirm that their reports are ATO-compliant.

Other Advantages of Buying an Investment Property

A Step Toward Homeownership

Purchasing an investment property can serve as a stepping stone to homeownership, potentially allowing you to enter the property market sooner compared to saving for a primary residence. Being able to afford properties in certain locations may necessitate a smaller deposit, making it more accessible than purchasing a home in a major city.

Property Cycle Leverage

Embracing the concept of “rent vesting” allows you to capitalise on rising investment property values while enjoying the amenities of your preferred location.

As the value of your investment property rises, you can either use the equity or sell it. This money can then be used to purchase your dream home, one that is exactly fitted to your requirements and circumstances.

Less Volatile Investment

Investing in property offers a less volatile option compared to investments like shares, which can be unpredictable and subject to rapid fluctuations. Property values may indeed fluctuate, but these changes tend to occur gradually, providing you with the advantage of planning your next steps more effectively.

Cons of Buying an Investment Property

As a first-time homebuyer entering the realm of property investment, you may encounter certain disadvantages.

Property Management Costs & Maintenance

Owners of investment properties must additionally handle tasks such as property maintenance and tenant management.

Acquiring and maintaining an investment property as a first-time homebuyer in Australia can bring significant financial responsibilities. Managing tenants and addressing repair and maintenance issues can become substantial expenses.

You must account for various property expenses, including tenant screening, property advertising, bond lodging, rent collection, and maintenance costs. Alternatively, you may opt to hire a property manager to handle these tasks, incurring additional expenses.

Capital Gains Tax

CGT is a tax levied on capital gain derived from the sale of capital assets acquired in Australia on or after September 20, 1985, such as property or shares.

When you sell an investment property for a profit, you pay tax on capital gains based on the difference between the asset’s cost and the disposal proceeds. The amount of tax you owe is determined by your annual taxable income, with long-term capital gains taxed at lower rates than ordinary income.

- CGT on Investment Properties

Unlike your primary residence, investment properties do not enjoy an exemption from CGT. This implies that when you decide to sell your investment property in the future, you’ll be subject to CGT on any capital gains accrued.

- No CGT Discount for Short-Term Ownership

If you’ve held the investment property for less than 12 months, you won’t qualify for the 50% CGT discount applicable to assets held for over a year. This can substantially increase your tax liability on any capital gain.

- Impact on Your Financial Position

Paying CGT on a property investment can diminish the profits you gain from the sale, potentially affecting your overall financial situation. This can be a drawback for first-time homebuyers relying on the sale of their investment property to fund their primary residence purchase.

- Complexity and Confusion

CGT is a complex concept, even for experienced real estate investors. First-time homebuyers may find it challenging to navigate CGT intricacies, possibly necessitating professional advice, which can add to the overall cost of buying an investment property.

Other Disadvantages of a Property Investment

The other disadvantages of Investing in property as a first-time buyer include the absence of government incentives and entitlements designed for first-home buyers, and high interest investment loans.

Fewer First-Home Buyer Entitlements

Government incentives and entitlements, which are frequently customised for first-time home buyers, do not typically extend to investors.

This means you are unlikely to be eligible for the first-time homebuyer grant or the federal government’s loan deposit programmes.

Furthermore, stamp duty deductions and concessions that are beneficial to traditional first-home buyers may not be accessible in most circumstances for investment properties.

Higher Interest Rates

One drawback of purchasing an investment property as a first-time homebuyer in Australia is the likelihood of facing higher interest rates.

Investment loans, particularly interest-only loans, often come with slightly elevated interest rates. This is primarily because lenders and regulators perceive these loan types as having a higher risk of default.

While interest-only loans may appeal to investors seeking tax advantages, it’s important to note that once the interest-only period concludes, you’ll be obligated to make principal and interest repayments at the higher interest rate, potentially impacting your financial commitments.

Is Property a High Risk Investment?

Investing in real estate has both potential rewards and inherent risks. You are susceptible to inherent property investment risks such as low rental income, vacancy, property slump, and so on, as with any investment. There is also the potential of increased mortgage interest rates.

Before making an investment decision as a first-time homeowner, you must research current market conditions and consider the feasibility of the financial responsibilities connected with property ownership.

A great start is critical for first-time property investors. It is critical to become acquainted with the local real estate market and understand all connected costs. Seeking advice from real estate professionals or financial consultants before making important decisions can be extremely beneficial.

When considering property investment, variables such as location, market conditions, rental possibilities, and ongoing costs must be carefully considered. Maintaining a long-term perspective is critical, as property values fluctuate over time.

To maximise the rewards on your investment, conduct thorough research and seek practical advice. Additionally, completing property modifications or renovations can raise rental possibilities and selling value.

Your needs will determine whether you go it alone or seek the advice of an advisor.

Take your time researching each stage, keeping dangers and potential advantages in mind.

Learn More About Property Investment with My Money Sorted!

Our team works hard to provide a variety of resources to help you build the financial future you deserve:

✓ Our Property Wealth Investment Plan is perfect for would-be property investors!

✓ Our Australian Property Show Podcast is FREE to listen to and shares a a wealth of knowledge every episode!

✓ Sign up to our Newsletter to receive FREE resources, tips and finance updates direct to your inbox each month!

My Money Sorted is your stress-free pathway to getting ahead sooner – if you’re unsure of what you need you can book a FREE call to find out more.

Here’s what your journey will look like:

Step 1: Start off with a quick money matters session with My Money Sorted

Step 2: Get matched with a financial advisor or broker that’s right for your financial situation

Step 3: Take the first step towards your financial goals with a clear roadmap that makes sense

It’s that easy!

Get Your Money Sorted Today by Speaking with a My Money Sorted Team Member