Are you a medical professional looking to purchase a property?

Whether you’re buying your first home or purchasing an investment property, you’ve come to the right place.

Our home loan guide to mortgages for doctors and medical professionals could help you get that property much easier.

Jump straight to…

How Do Mortgages for Doctors Work?

Let’s start by reviewing how mortgages work for any other borrower.

- If you don’t have enough cash to buy a house outright, what options do you have?

You can get a mortgage from a bank or a lender.

As the borrower, you repay the lender with interest and own the property after repaying the mortgage, which typically lasts 30 years.

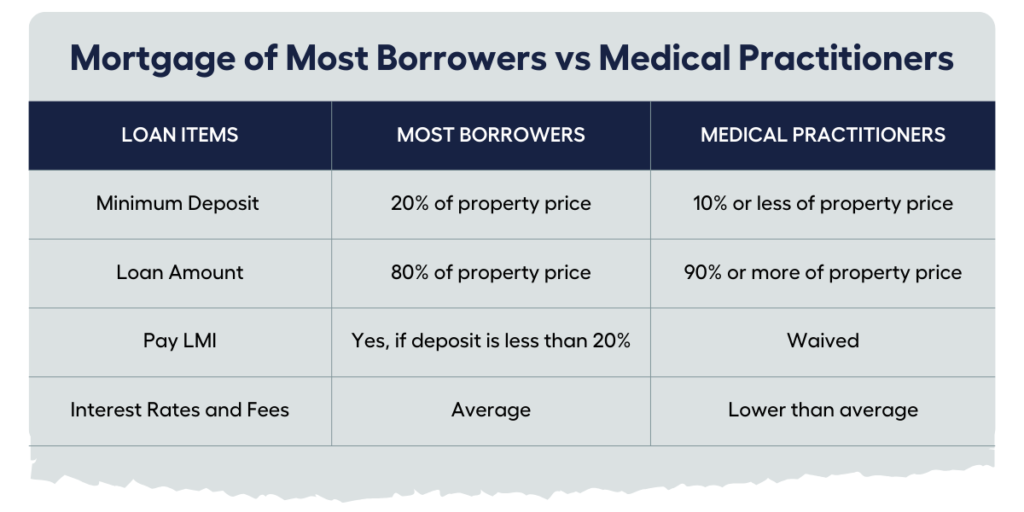

Most Australian lenders require a 20% deposit on a property.

If you’re unable to provide the 20% deposit, you can still get a loan but will have to pay Lenders Mortgage Insurance (LMI).

That’s generally how mortgages work in Australia…

But not for doctors and medical practitioners.

Home loans for doctors are almost the same as with any other profession.

However, due to their higher earning capacity, doctors may be eligible to get a much more favourable offer on their mortgage.

Doctors don’t need to pay a 20% deposit AND may also get the LMI waived.

Benefits of Home Loans for Doctors

Lenders such as banks or other institutions generally view doctors and medical professionals as low-risk borrowers.

Doctors are typically well compensated relative to other professions, which is why lenders consider doctors as ‘safe bets’ for home loans.

From a lender’s perspective, this could mean that doctors are less likely to default on their home loan.

Because doctors are seen as safe bets, they could:

- Have the lender waive the Lenders Mortgage Insurance (LMI)

- Pay lower deposit requirements

- Pay lower interest rates and fees

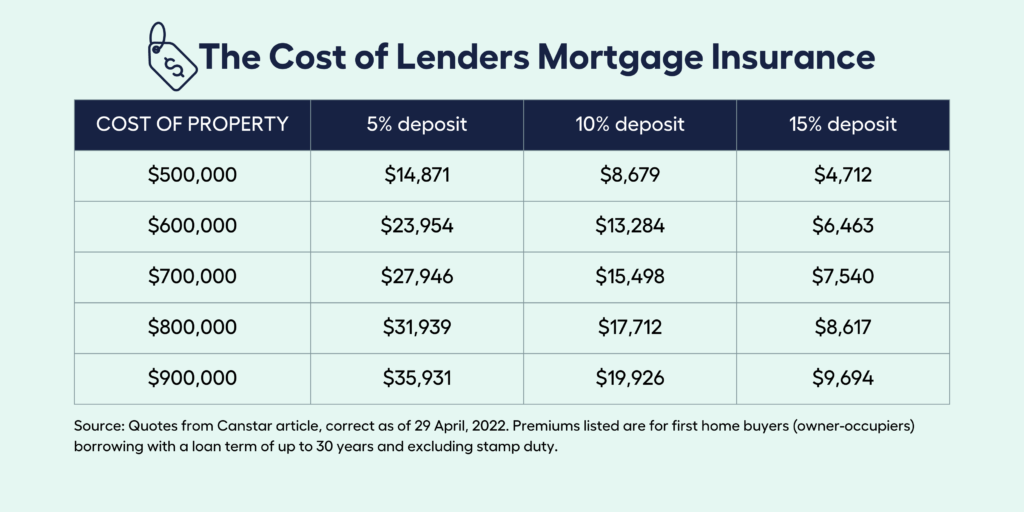

No Lenders Mortgage Insurance (LMI)

Lenders’ Mortgage Insurance (LMI) protects the lender in case the borrower cannot make the repayments on their mortgage.

Most borrowers will be required to pay LMI if lenders see risk in financing the loan and if borrowers need more than 80% of the property price.

This does not apply to doctors.

Lenders tend to waive the Lenders Mortgage Insurance for doctors as they are considered low-risk borrowers due to their higher earnings capacity.

As a result,

- the cost of LMI isn’t added to the mortgage repayments of medical practitioners.

A recent Canstar article posted a table showing an estimated cost of LMI premiums if a typical borrower was to pay a deposit less than 20% of a property’s total value.

If you’re a doctor or a medical professional, the table above shows the amount you save by avoiding LMI premium.

It’s money you can invest to diversify your portfolio or build capital growth.

Lower Deposit Requirements

Hand in hand with waiving LMI for doctors, lenders also allow a lower deposit from doctors compared to most borrowers.

Generally, banks would require borrowers to pay a deposit of at least 20% of the property value, otherwise, the borrowers pay LMI.

Doctors, however, only need to pay a deposit of 5% to 10% (or even less) of the property value and not pay an LMI premium.

Some lenders may even offer no deposit and no LMI for doctors!

- This means you can borrow from 90% to 100% of a property value and not pay LMI.

Better yet, as a doctor or medical professional, a low deposit amount means you can own a house and enter the property market sooner than most people in Australia.

Interest Rates & Fees

Doctors are perceived as good borrowers who rarely miss mortgage payments due to their high salaries and employment prospects, which make them attractive customers for lenders. Thus, lenders tend to offer interest rate discounts for doctors.

- These discounted rates are not advertised, but as doctors, they can negotiate a lower interest rate quite easily compared to others.

Discounted interest rates enable you to save thousands over the long term.

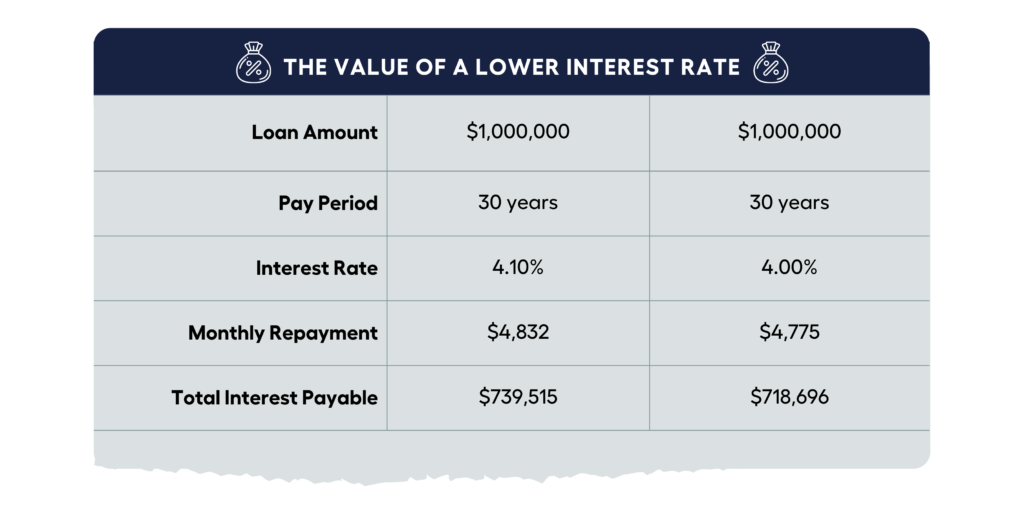

For example, let’s say you want to borrow $1,000,000 over 30 years and your lender’s rate is 4.10%. However, since you’re a doctor, you were able to negotiate a discount of 0.10%. Using the My Money Sorted calculator, here’s the difference:

- Monthly repayments at 4.10% interest rate = $4,832

- Monthly repayment at a discounted rate of 4.00% = $4,775

That’s a difference of $57.00 a month. And you would save $20,819 from the total interest payable over 30 years. A little negotiation in interest rates can go a long way over the long term.

- Also, lenders may waive loan fees such as the application fee or services fee. It could save you a few hundred dollars, but this would vary from lender to lender.

Risks Associated with Mortgages for Doctors

As we’ve seen earlier, being a doctor and medical practitioner has a lot of perks when it comes to getting a home loan.

However, benefits don’t come without a risk no matter how remote they may be.

Here, we’ll discuss the 3 Pitfalls You Must Avoid When Getting a Home Loan:

- Getting a mortgage too soon

- Existing debt affects your borrowing capacity

- Not thoroughly reviewing the terms of the loan

Getting a Mortgage Too Soon

The most considerable risk comes when doctors apply for a mortgage early in their careers. It is because most doctors are still mainly in debt relative to their income right after university.

Remember:

- Getting a mortgage is one of the biggest financial commitments anyone can make.

The inability to commit to your repayments can lead you to:

- Paying late fees

- Damaging your credit score

- Selling your property to pay your obligations

Regardless of your occupation, careful financial planning is essential if you want to obtain a mortgage.

Debt and Borrowing Capacity

Comprehensive credit reporting ensures lenders have ‘shared’ access to all your liabilities across all institutions; including the government.

So Higher Education Loan Program (HELP), Australian Taxation Office (ATO), and credit card debts are liabilities that need to be accounted for when lenders calculate your borrowing capacity.

Your borrowing capacity is the amount of money that a lender will loan you based on your income, expenses, and debts among others.

Higher Education Loan Program (HELP) Debt

Let’s say you make $200k a year but have a $40k HELP debt, that makes your annual repayments at 10% of your salary, or $20,000.

Despite the comparatively little debt, the annual commitment is based on income rather than the amount owed, which greatly reduces your borrowing capacity.

Depending on how your borrowing capacity appears with that annual commitment, it may be wise to get advice from a professional medical tax expert and consider paying the debt out sooner if you want to apply for a loan.

Australian Taxation Office (ATO) Debt

Similar to how back taxes owed to the government show up on tax portals, in some circumstances where payment arrangements have not been made, this debt may also be listed on the customer’s credit report.

Lenders classify monthly repayments made under an ATO payment plan as expenses, therefore they must be recorded and taken into account when determining borrowing capacity.

It can help you to better prepare and even fund your future tax responsibilities if you get foresight from a qualified medical accountant regarding your ATO debt.

Credit Card Debt

A common misconception is that credit cards are not liabilities if you don’t use them or you pay off your credit card balance each month.

However, since you have the option to borrow up to the limits set by your finance company on credit and loans, lenders will evaluate your borrowing ability based on these limits, not the credit or loan balance.

Even if you pay off your $20k credit card balance each month without incurring interest fees, it will still be counted as a $20k obligation when the time comes to have a loan assessed.

What you can do:

- Close credit cards you don’t use before submitting an application for a mortgage.

- For credit cards that you use, consider lowering their limits as much as you can or speak with your lender about it.

The Terms of the Loan

The cheapest loan isn’t necessarily always the best.

Before making a decision, consider the loan’s terms. Some terms will be more appealing than others, depending on your personal circumstances, even though you would be paying more than the cheapest loan.

Carefully consider the following:

- You can save a lot of money over the course of the loan and pay it off faster by having an offset account connected to your home loan or the option to make additional repayments and redraws without incurring fees.

- You may be able to borrow more money but at a slightly higher interest.

- You may be able to get a loan with a shorter pay period and low interest rate but with a higher monthly repayment, or a loan with a slightly higher interest rate and longer repayment period but a lower monthly repayment.

- Lenders have different loan pre-approvals, some take 48 hours while others take 4 to 6 weeks.

Proper planning of your current finances and future finances is a wise move if you intend to get a mortgage regardless of your profession.

- If you feel overwhelmed by money issues, stress less by chatting with an MMS expert for free. We can connect you to the right financial adviser who can help simplify the financial planning process.

Who is Eligible for Medical Home Loans in Australia?

When the term “medical professional” is used, it is either limited to referring to only physicians and registered nurses or it is mistaken with the term “healthcare worker.”

This misunderstanding makes it unclear which professions meet the requirements for medical professionals’ home loans.

The table below lists the medical professionals qualified for medical professional home loans:

The eligibility criteria for a physician home loan is that you must be a member of either the Royal Australasian College of Physicians (RACP) or the Australian Society of Physician Assistants (ASPA).

Other associations from related industries may also be accepted.

Yes, registrars, interns, residents, and staff specialists are all eligible for a loan for medical professionals.

Furthermore, some lenders prefer working with certain types of specialists, including anaesthetists, psychiatrists, obstetricians, and radiologists.

Can Nurses Avoid LMI or Receive Home Loan Benefits?

Nurses don’t automatically avoid LMI or qualify for the same home loan benefits as doctors.

However, with a strong employment history and substantial savings set aside, it can still be possible.

The Lenders Mortgage Insurance can be waived for nurses when borrowing up to 90% of the property’s total value if they can prove that:

- They have stable employment

- Earn over $90,000 per year

- They have good credit rating

If you hold one of the following positions, you are eligible for a nurse home loan deal:

- Registered Nurse

- Nurse Educator and Researcher

- Nursing Support and Personal Care Worker

- Midwife

- Nurse Manager

- Enrolled Nurse

Midwives were previously excluded from benefits that other medical practitioners would be entitled to because they were seen as somewhat high-risk clients.

But that has changed.

- If a midwife earns more than $90,000 annually, they are eligible for an LMI waiver.

Do take note that when evaluating a loan, lenders do not distinguish between nurses and midwives.

How to Choose a Mortgage Broker or Lender for a Doctor Home Loan?

When one of your patients comes in with a unique case, you consult the experts.

Finance is no exception.

Going to a lender directly yourself means you will need to:

- Compare the rates of different lenders

- Negotiate a lower required deposit

- Bargain for interest rate discounts

- Ask for waived fees

A mortgage broker can do all of these for you and save you time. Time you’re better off spending to practise your profession.

Besides, most lenders would rather work with mortgage brokers, which is why you don’t have to pay mortgage brokers because lenders are the ones who pay them commissions for bringing in business.

When looking for a mortgage broker, it’s best to make sure that your chosen broker:

- Has an Australian Credit Licence (ACL) obtained through the Australian Securities and Investments Commission (ASIC)

- Is a member of either the Finance Brokers Association of Australia (FBAA) or the Mortgage & Finance Association of Australia (MFAA)

A good mortgage broker has access to a variety of lenders, ideally also including your bank.

It’s also important that your mortgage broker knows which lenders offer the best deals.

Most lenders do not always advertise interest rate discounts and other benefits publicly, so make sure your mortgage broker knows how far they can negotiate with them.

Best of all, a licensed mortgage broker is mandated by law to work in your best interest, and you don’t have to pay them to do it.

If you need help looking for a mortgage broker that looks after your best interest, talk to your My Money Sorted for free.

Knowing your borrowing power is just the first step. A mortgage is a big investment of both time and money, which is why It’s often best to receive guidance from a financial expert like a mortgage broker. Many people may be unaware of this…but just like you, 41% of Aussies intend to get financial advice rather than going it alone, according to an Australian Securities and Investments Commission (ASIC) report.

to get financial advice rather than going it alone, according to an Australian Securities and Investments Commission (ASIC) report.

Find the right Mortgage Broker for you with the help of our team of experts.

When you book a call with MMS, you’ll:

✓ get a better understanding of your home loan options

✓ have an idea of the experts you can call on to help you reach your goals

✓ be matched with a mortgage broker who can help develop the best home loan strategy for your situation

My Money Sorted is your stress-free pathway to getting ahead with your home loan.

Here’s what your journey will look like:

Step 1: Start off with a quick money matters session with our team

Step 2: Get matched with a licensed Mortgage Broker who can help you

Step 3: Take the first step towards your money goals with a clear and sound roadmap prepared by an experienced Mortgage Broker

It’s that easy!

I Want to See All My Options with the Help of a Finance Expert

Book a FREE Call Today