Imagine waking up one day and realising you can finally quit your job and retire early.

No more alarm clocks, no more commuting, no more dealing with office politics. You can now spend your days doing whatever you want, whether it is travelling the world, pursuing hobbies, or simply relaxing and enjoying your newfound freedom.

If you are interested in retiring early, you are not alone. Almost anyone dreams of retiring early. But what does it take to make that dream a reality?

We will cover all you need to know about retiring early in Australia in this guide. So if you are ready to start your journey to early retirement, read on!

Jump straight to…

Strategies to Retire Early: What does it take to retire sooner rather than later?

Here is some good news. Retiring early is not as impossible as it seems. With smart planning and discipline, it is something that anyone can achieve.

But in order to start living your dream life sooner rather than later, it is important to be familiar with the basics.

The Basic Rules of Retirement

By following the basic rules of retirement, you can increase your chances of achieving your early retirement goals.

These rules form a strong base for your retirement plans, guaranteeing financial security and peace of mind in your golden years.

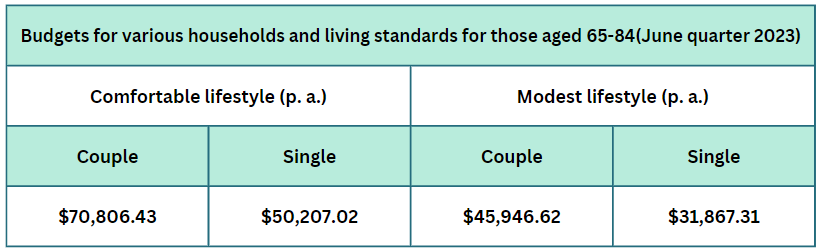

The Association of Superannuation Funds of Australia Limited (ASFA) currently estimates that the budget of various households with a comfortable lifestyle can range from $50,207.02 for a single person to $70,806.43 for a couple.

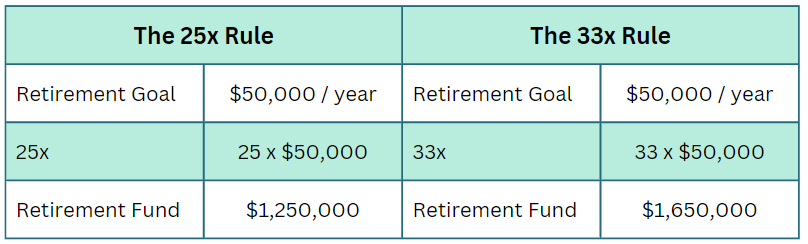

What is the 25x rule for retirement?

Retirement is a phase in life we all look forward to, the time when you finally get to relax and do what you love. But how do you know if you have enough money saved up for it? That is where the 25x rule comes in, and this ‘rule of thumb’ can make it super simple.

Think of the 25x rule as a magic number that tells you how much money you’ll need for retirement. It is like a savings goal.

Let’s say for example you want $50,000 a year to live comfortably in retirement. To figure out how much you need to save, just multiply $50,000 by 25. That gives you $1,250,000.

But here is the thing: the 25x rule assumes your money will grow by 4% each year.

It is like your savings making more money on their own. This way, you can take out $50,000 each year in retirement and still have money left over.

However, in the real world, your money might not grow that fast, especially if you are playing it safe with your investments.

If your money only grows by 3%, then you need to follow the 33x rule. So, in this case, you would need $1,650,000 instead of $1,250,000.

Both the 25x rule and the 33x rule help determine your retirement fund, but the 33x rule considers a lower interest rate in its calculation. Do keep in mind that these rules are used as a guide only.

Also, retirement is not just about money. It is about finding a balance that suits your retirement lifestyle and lasts as long as you do.

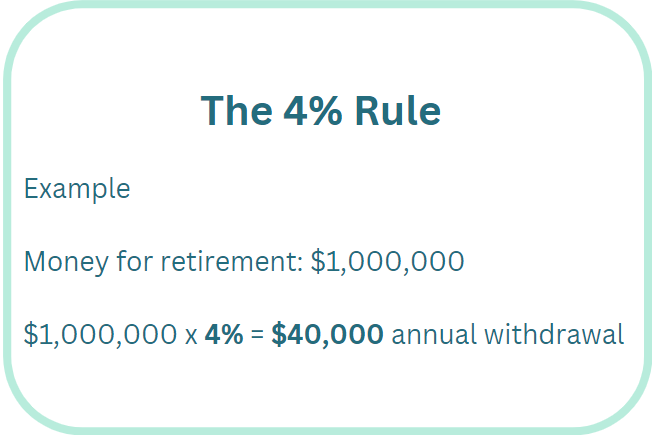

What is the 4% rule for early retirement?

The 4% rule, in its essence, suggests that you can comfortably retire by withdrawing 4% of your total investment portfolio during each year of your retirement.

The 4% rule is like a savings plan. If you have $1 million for retirement, you can take out $40,000 in the first year.

This pattern continues each year. You recalculate your withdrawal based on your updated retirement savings balance and the current inflation rate.

However, the 4% rule was made for people retiring for 30 years, not those who want to enjoy 40-plus years of retirement. The 4% rule might not work for such a long retirement. Plus, it sticks to a strict plan, which might not be flexible enough for early retirees who want to change their spending as life goes on.

If you dream of retiring early, you should think about other ways to manage your money or talk to a financial expert who can help you create a plan that fits your needs. Early retirement is your unique journey, so your financial plan should be tailored just for you. Let us explore your options and get you on track for your early retirement dreams.

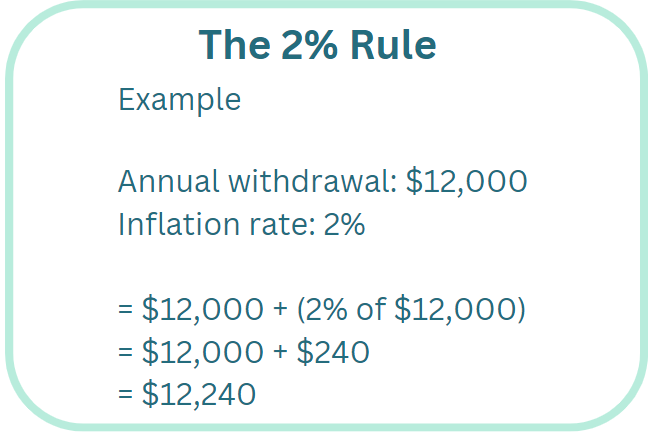

What is the 2% rule for retirement?

The 2% rule is a safe way to spend your retirement savings. It suggests that you should only take out 2% of your savings each year when you retire. This helps make sure your money lasts a long time by being extra careful.

Imagine you are approaching retirement. You have diligently saved $600,000 in your retirement account. With the 2% rule, you will withdraw only 2% of your retirement savings each year.

To keep your purchasing power intact, you will adjust your annual withdrawal for inflation. Let us assume an inflation rate of 2% per year. In the second year, you will need a bit more than $12,000 to cover the rising costs of living.

Similar to the 4% rule, this pattern stays the same every year. The updated retirement savings balance and the rate of inflation are used to recalculate your withdrawal. It ensures that your money remains sustainable throughout your retirement journey.

Understand the financial streams that will support you & maximise them

Think of your money like a river that splits into different streams. These streams are your various sources of money, and they can make a big difference in your life.

To make the most of your finances for retirement, let us get to know these money flows better.

Passive Income Streams

Passive income is the money you earn without being actively involved in their day-to-day operations. It is the financial equivalent of setting up a well-oiled machine that generates cash while you are out enjoying the beach or pursuing your passions. Think of it as your money working for you, rather than you working for your money.

Passive income provides a safety net during uncertain times, such as a global pandemic or economic downturn. Additionally, passive income can create a source of income that is not tied to the traditional 9-to-5 job, allowing you to enjoy more flexibility in your life.

Whether you are considering retiring early, going on that dream vacation, or simply reducing financial stress, passive income streams can make it a reality. The key is to start early, be patient, and diversify your income sources.

Some passive income streams are shares, managed funds, property, ETFs, index funds, and REITs.

Let’s discuss some of the passive income ideas that you may consider.

Superannuation

Superannuation is more than just a financial term; it is your financial passport to a worry-free retirement. Think of it as a partnership between you and your employer, working in tandem to secure your golden years. This mandatory contribution is known as the Super Guarantee (SG), currently set at 11% of your income.

If you are not ready to retire, working a bit longer can help your super money grow more. It is like waiting for a cake to bake properly. If you can afford it, you can also put voluntary contributions into your super account.

The earliest age at which you can access and remove your superannuation is known as the preservation age. The Transition to Retirement (TTR) option lets you keep working full-time, part-time, or casually while having restricted access to your super once you reach preservation age.

When you retire, you can convert your superannuation savings into an account-based pension. This means your superannuation money is moved into an account, and you receive regular payments from it, typically on a monthly, quarterly, or annual basis.

Assets

One way to create a sustainable retirement income stream is to capitalise on your assets. Your assets can include anything from your superannuation savings to your home equity to your investment portfolio.

In preparing for retirement, capitalising on your various assets is essential. You can utilise home equity through downsizing, renting out space, or reducing your mortgage. Small business owners can use their profits to invest in income-producing assets like dividend stocks or rental properties.

Some investments can amplify income by investing in funds that use borrowed money to increase market exposure. Additionally, pension plans can employ leverage and derivatives to manage asset-liability risks, covering interest rates, inflation, currency, and equity risk. These strategies offer valuable ways to enhance your financial security as you approach retirement.

Investments & Dividends

Investing might sound intimidating, but it is simply putting your money into different assets like shares, property, or bonds, with the hope of getting more money back in the long run.

This strategy is like planting seeds; you invest today and let your money grow over time to build wealth. You can choose to invest directly in companies that will help you achieve your investment goals or use managed funds that pool your money with others for a diversified approach.

Through strategic investing and dividend income, you can supplement your income and take greater control of your finances.

Understand financial expenses and minimise them

Sometimes it seems like there is a never-ending game of trying to keep money in your pocket when managing your finances.

Gaining financial freedom begins with having a clear understanding of your out-of-pocket expenses. Never forget that every dollar you save counts towards your financial objectives and affects your retirement journey.

Live below your means & avoid lifestyle creep

As your income grows, it is natural to want to enjoy a better quality of life. However, if you are not careful, you may increase your spending without realising it. This is called lifestyle creep.

For instance, if you have more money to spend, you might start going out to eat more frequently. Alternatively, now that you have more money, you might start purchasing more costly clothing.

When you think about retirement, you are essentially planning for a future where you will not have your regular income from work. Instead, your financial well-being will rely on savings, investments, and possibly government benefits or pensions.

To make the transition to retirement smooth and secure, living below your means and fending off lifestyle creep are vital strategies.

Debts: Mortgages, Personal Loans, Credit Cards, & Buy Now Pay Later Schemes

Retirement ought to be a period of calm and relaxation, but debts have the potential to cloud this experience. Debts come in various forms, and each has its unique implications for your retirement.

Mortgages

Many people have outstanding home loans when they retire. Even though it may seem overwhelming, this debt is manageable. To access your property’s value without having to make monthly payments, think about whether it’s in your best interests to employ an alternative strategy such as downsizing to a smaller, more affordable house.

Additionally, if you have a lump sum of money available, you might want to think about how it can be strategically used to pay down or manage your own home loan, thus easing your financial situation in retirement.

Personal Loans

Personal loans can be more difficult at times. The interest rates on these loans are frequently higher. To save money each month, think about making debt repayment a top priority or combining debt into a loan with a lower interest rate.

Credit Cards

High-interest credit card debt can be sneaky. It is advisable to pay off your credit card debt in full each month when you are retired to avoid paying high interest rates. Keep your spending in check and stay away from unnecessary purchases.

Buy Now Pay Later Schemes

While the popularity of buy-now-pay-later schemes has simplified the purchasing process, it can also result in unforeseen financial strain. In retirement, keep a watchful eye on your buy-now-pay-later obligations because nonpayment can result in late fees.

In retirement, it is important to exercise caution when it comes to taking on new debts or giving in to impulsive spending. It is a time to manage what you have wisely, so you can enjoy a stress-free retirement.

Taxes on Property & Other Investments

Retirement should be a time of relaxation, not worrying about taxes. By understanding what you have, you can make your retirement more comfortable and pay fewer taxes.

If you own an investment property, you need to be aware of Capital Gains Tax (CGT). When you sell an asset like property, you may incur CGT. It is important to check the specific rules that apply to retirees, as they can sometimes offer significant tax concessions and benefits.

The tax rules in retirement can be a bit tricky, and everyone’s situation is different. So, it is a good idea to talk with a financial advisor who can help you figure out the best plan for you.

Pre & Early Retirement Preparation

Retirement might seem far off for some, but taking the right steps early on can make it a reality sooner than you think.

Prior to starting your retirement journey, you must establish specific objectives. For you, what does retirement mean? Age is not the only factor to consider; your desired lifestyle also matters.

Estimate Life Expectancy: How much will you need to remain comfortably retired?

Estimating your life expectancy is a vital part of retirement planning. In your golden years, how long do you think you will live and how much money will you you need to live comfortably in retirement?

Once you have a rough estimate of your life expectancy, it is time to consider the financial implications. The goal is to ensure you have enough money to sustain your desired lifestyle throughout retirement.

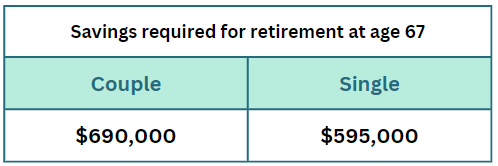

An average person might think that having a million dollars would be enough for a comfortable retirement, but that’s not always the case.

In fact, the Association of Superannuation Funds of Australia Limited (ASFA) estimates that the savings required for a single person to retire at 67 is only $595,000, and $690,000 for a couple.

The reality is that you can achieve a happy retirement without needing millions of dollars.

The amount you need for retirement depends on factors such as how much income you earn, lifestyle choices, healthcare expenses, household income, economic issues, relationship status, and the impact of inflation over time.

As part of a larger financial plan, setting aside a certain amount of money is a smart place to start when planning for retirement.

More importantly, determine what a comfortable retirement means to you. Once you know that, you can figure out how much money you’ll need to meet your goals for your income in retirement.

Strategy & Budget for Pre-Retirement

Pre-retirement is the important time just before you retire when you need to make sure you have enough money to enjoy your retirement. This phase usually starts 5-10 years before you stop working.

During this phase, the way you handle your money and make plans will greatly impact how comfortable and secure your retirement will be.

Aggressive Strategy: FIRE

The FIRE (Financial Independence, Retire Early) movement is centred around the idea of achieving financial independence as soon as possible. The fundamental idea behind FIRE is that by making substantial sacrifices in your early career, you can wave goodbye to the 9-to-5 working hours at a much younger age.

The daily grind includes spending as little as possible and saving all you can. The earlier you start investing, the longer your retirement. To cut expenses, you can reduce high-interest debts, lower low-cost debts like mortgages, and save a big chunk of your salary. Those who are committed to FIRE check their monthly budget, manage daily expenses, and skip non-essential expenses like fancy clothes and luxury.

Moderate Growth Strategy

A moderate growth strategy is an investment plan that aims to keep your retirement savings growing while also being careful with risks and protecting your money.

When you are getting ready for retirement, this approach involves investing your savings in a way that finds a middle ground between making money from your investments and keeping your funds safe. This plan usually includes a mix of assets like shares, fixed-income investments, and perhaps some safer retirement income options like high-interest savings or bonds.

Strategy & Budget for Early Retirement Phase

Early retirement is when you decide to stop working and use your savings and investments to enjoy life before the usual retirement age, usually around 65 to 67 which is when one is eligible for the government age pension. It means you leave working life earlier than most, giving you more free time on your own terms.

During this time, you have enough money to support your lifestyle without needing a regular job income. To prepare for early retirement, you need a plan and budget to make sure you can maintain your desired lifestyle throughout your retirement years.

Aggressive Strategy: FIRE

Retirement years are all about freedom, simplicity, and wise money management. First, your investments serve as a kind of financial lifeline by providing income for your daily needs. It is crucial to exercise caution with how much you withdraw each year, typically 2-4% of your savings, to make your money last.

Second, your greatest ally is passive income. It refers to income that you receive from sources other than labour, such as stock dividends or rent from real estate. You do not have to worry about running out of money because these funds help with your living expenses.

Finally, the freedom to live your life how you choose is the true beauty of FIRE. Without the stress of work, you can travel, indulge in your passions, spend time with your family, and unwind. Just keep in mind to monitor your assets, make healthcare plans, and consider your legacy. The main goal of FIRE is to enjoy retirement with financial security.

Don’t forget to factor in inflation

When it comes to managing your money, one essential factor to always keep in mind is inflation. Now, I know it might sound a bit fancy, but it is basically the silent thief that eats away at the value of your hard-earned dollars over time.

Simply put, inflation is the tendency for prices of goods you regularly buy to rise, decreasing the future value of your money. You are therefore losing out if you keep your savings in a low-interest account or tucked away under the mattress.

If you want to beat inflation, think about investing in assets like shares or real estate that can increase in value over time. In this manner, you can make sure that your money does not depreciate over time. Make your money work for you and avoid being taken by surprise by inflation.

FAQs from our MMS Community Members

This is your go-to guide for your questions about early retirement. Let’s get started on your early retirement journey!

What is the best way to retire early?

The best way to retire early is by following a tailored financial plan. Start by saving consistently and living within your means. Invest your money wisely in suitable assets to make your money work for you. It is important to keep track of your expenses and cut down on unnecessary spending. Pay off high-interest debts as soon as possible. Once they are paid, you have more money to invest.

Having a clear goal and timeline for your early retirement is crucial. It is also a good idea to seek advice from a financial advisor to help you create a solid retirement plan. In Australia, taking advantage of superannuation (super) can be a valuable tool in your early retirement strategy, as it provides tax benefits and long-term savings. Remember, early retirement requires discipline and patience as well as the right approach that is on the same page as your financial situation.

Should I leave my super in accumulation when I retire?

When you retire in Australia, you have a choice about what to do with your super. Leaving it in accumulation is one option. It means your money stays invested, and you can keep adding to it if you want. The benefit is that your super fund can potentially continue to grow over time.

However, there are rules about when you can access your super, so you may not be able to use it immediately. It is a good choice if you want to let your money grow and are okay with waiting a bit to access it. But remember, it is essential to consider your financial needs and goals before making a decision and getting advice from a financial advisor can be a wise move to ensure you are making the right choice for your retirement.

What should you expect when you first retire?

When you first retire, there are some key things to expect. Firstly, you will likely have more free time, so think about how you want to fill your days. You will also have a change in your annual income. Your regular paycheck will stop, but you might have income from sources like your superannuation or other investments.

You may also be eligible for benefits like the Government Age Pension. It is important to budget your expenses and adapt to your new financial situation. Healthcare may become more critical, so understand your health insurance options. And lastly, consider how you will stay socially connected and find purpose in retirement. It is an exciting phase of life, but planning and adjusting to these changes will help you enjoy your retirement to the fullest.

What is the golden rule of retirement saving?

The golden rule of retirement saving is simple: Start early and save consistently. The sooner you begin saving for retirement, the more time your money has to grow through the power of compounding. Aim to save a portion of your income regularly, whether it is from your paycheck or other sources.

Don’t dip into your retirement savings unless it is absolutely necessary. Be disciplined and avoid high-interest debts. Diversify your investments to spread the risk, and consider seeking advice from a financial expert. By following this rule, you can build a solid financial cushion for a comfortable retirement.

Can I retire with $1 million dollars at 55?

Retiring with $1 million at 55 is possible, but it depends on your lifestyle and financial goals. The amount you can comfortably retire with varies for each person.

A good rule of thumb is the 4% rule, which suggests you can safely withdraw about 4% of your savings each year without running out of money. So, with $1 million, that’s $40,000 per year.

It’s essential to consider your expenses, any other sources of income, and how long you expect retirement to last. Also, keep in mind the cost of living in Australia, which can vary.

Talking to a financial advisor can help you make a more accurate plan based on your specific situation and ensure a comfortable retirement.

Talk to our team today to stress less about the future with solid retirement planning advice!

Book a FREE 15 min Call or Send Us Your Questions.