Housing prices can be unpredictable, and it’s tough to time the property market. So, when you’re really intent on buying a house or on taking the plunge as a property investor, it’s best to focus on having enough money saved for your deposit.

And this brings us to the difficult question:

Do you have enough money saved to pay for a house deposit?

If you’re finding it tough to raise the funds for the 10% or 20% cash deposit needed to get a home loan, there may be a way for you to secure the home loan with a little help from your family.

If your family can’t provide the money to pay the deposit as well, you can look into obtaining a guarantor home loan.

A guarantor home loan is a great way for first time home buyers to purchase their own property and for property investors to get into the property market.

Jump straight to…

How does a guarantor home loan work?

Read on and find out.

Understanding Guarantor Home Loans and How They Work

Most lenders will need you to pay Lenders Mortgage Insurance (LMI) if you do not have a 20% deposit. However, as home prices go up, the amount required for that 20% deposit also increases.

A guarantor home loan, on the other hand, may enable you to purchase a property with a lower deposit and without incurring the cost of LMI. That’s because a guarantor offers equity in their own house as additional security for your loan.

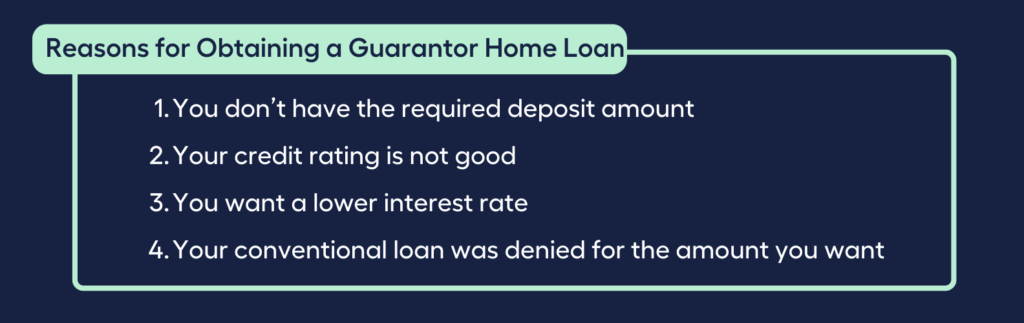

Other reasons you might consider acquiring a guarantor loan, aside from not having the needed deposit amount, are:

- Your credit rating is not great.

- You seek a reduced interest rate with the assistance of a guarantor.

- Your conventional loan was denied for the amount you requested.

Now that we have an overview of what a guarantor home loan is, let’s get into the details.

What is a guarantor in a home loan?

A guarantor home loan works to help home buyers get onto the property ladder sooner than anticipated.

A guarantor home loan enables immediate family members to use the equity in their home to secure a part of or the entire loan amount a home buyer needs.

There are 2 Types of Guarantees:

Limited and Unlimited.

A limited guarantee suggests that the guarantor will cover only a portion of the debt, whereas an unlimited guarantee implies that the guarantor will cover the entire amount of the obligation.

As a home buyer, you still need to repay the money you borrowed from a lender, but the guarantor offers security for the loan, which most borrowers would otherwise provide by paying a deposit.

In certain circumstances, borrowers who use a guarantor can obtain a house loan without the standard 20% deposit requirement, which means they won’t have to pay LMI.

In the event that you are unable to fulfil your home loan repayments, the guarantor will be responsible for the repayments. If the guarantor is unable to make the mortgage repayments, the bank may seize their home in order to reclaim the loss.

Guarantors can choose to provide a limited guarantee or only guarantee a percentage of the loan (say, 20%) rather than the entire amount.

In a limited guarantee, the guarantor’s property is safe once the borrower has settled the guaranteed amount of the loan (even if the borrower misses future payments). The guarantor can then request to be released from the loan.

How much can I borrow if I have a guarantor?

You may be able to borrow up to 100% of the property’s purchase price with a guarantor home loan and avoid paying a deposit. You may be able to borrow up to 110% of the purchase price in some situations.

The amount you can borrow with a guarantor will be determined by:

- The Lender

- The Guarantor’s financial situation

- The loan amount covered by the Guarantor

Even if you have a guarantor, some lenders may still require you to put down a home deposit, often at least 5% in true savings.

Your purpose for borrowing may have an impact on how much you can borrow utilising a guarantor home loan.

You may be able to get a guarantor home loan up to 105% of the property value for a first purchase of a family home, an investment property, or the total value of the land plus construction cost of your home.

You may be able to borrow up to 110% if you plan to do debt consolidation along with the purchase of a home.

If you plan on refinancing, you may be able to borrow up to 100%.

| How Much Can Be Borrowed with a Guarantor Home Loan | |

| % of Property Value | Purpose of Loan |

| 105% | Purchase of first family homePurchase of investment propertyConstruction of a house (includes value of land and cost of construction) |

| 110% | Purchase a home along with debt consolidation |

| 100% | Refinancing |

While there are no limits on the maximum loan amount, other lenders may require the borrower to fulfil additional lending requirements when borrowing more than $1 million.

How much equity does a guarantor need?

Often, the guarantor must have enough equity in their home to cover 20% of the value of the new property. Some lenders permit up to 27% of the loan amount to be used to pay for related expenses such as stamp duty, conveyancing fees, and other tax and legal fees.

Stamp duty is a tax levied by state and territory governments on specific documents and transactions. Stamp duty is required for things like automobile registration and transfers, insurance policies, leases, and the purchase of real estate such as a home or an investment property.

Equity is the amount that a person owns outright in a piece of real estate. Equity is calculated as the difference between the outstanding balance of a home loan and the home’s current value in the property market. Depending on the market, a property’s equity fluctuates.

| Equity = Current Market Value of Property – Mortgage Balance | |

| Property’s Current Market Value | $500,000 |

| Home Loan Balance | $300,000 |

| Home Equity | $200,000 |

How long does a guarantor stay on a mortgage?

Guarantors typically stay on a home loan anywhere between two to five years.

2 Conditions that Determine a Guarantor’s Loan Term

- How soon you pay down the loan

- How quickly the value of your home rises

These two factors help you determine when it’s financially cost-effective to get out of a guarantor home loan.

When it comes to removing the guarantee on guarantor home loans, the majority of big lenders and specialised lenders have similar policies although they may have slightly different requirements.

Once you have satisfied the following broad lending criteria, you may remove the guarantee:

- You should have made all of your payments on schedule throughout the past six months.

- Your loan shall not exceed 80% or 90% loan-to-value ratio (LVR) if you want to avoid lenders mortgage insurance (LMI).

- Your circumstances must comply with the lender’s policy in terms of your credit history, income, employment, and other factors.

Do note that it is ideal to exit the guarantor home loan agreement when you owe less than 80% of the value of your property. This way, you may potentially save thousands of dollars by not paying LMI.

You may also be eligible for a lower interest rate.

Who Can Be a Guarantor

When looking for someone for your guarantor home loan, you should ideally pick somebody that you trust and who, more importantly, trusts you. This is a big factor in what lenders are looking for in a guarantor of a loan.

The major condition for obtaining approval on guarantor home loans is that the guarantor has a strong relationship with the buyer. This usually refers to a close family member, which is why a guarantor home loan is also referred to as a family security guarantee.

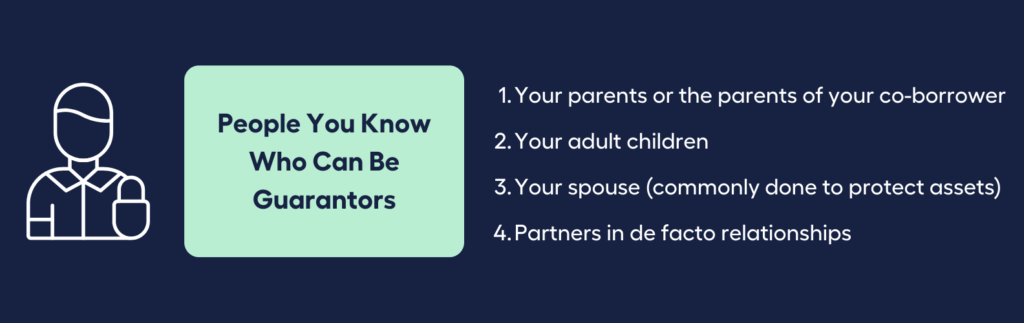

Most banks only accept the following individuals for a guarantor loan:

- Your parents or the parents of your co-borrower

- Your adult children

- Your spouse (this is commonly done to protect assets)

- Partners in de facto relationships

* A de facto relationship is one in which you and your partner share a home for at least two years without separation. Factors that determine a de facto relationship in Australian Law can be found here.

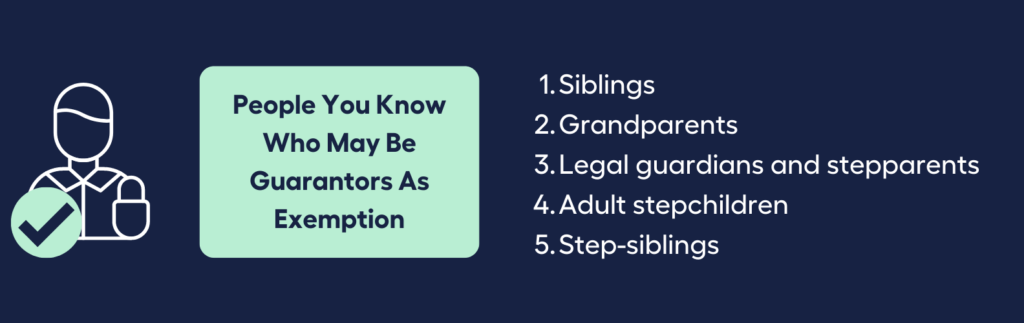

As an exemption to regular policy, the following family members may also be acceptable:

- Siblings

- Grandparents

- Legal guardians and stepparents

- Adult stepchildren

- Step-siblings

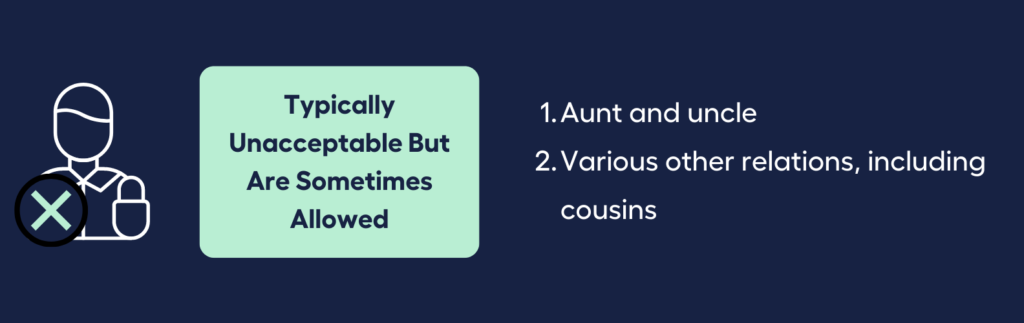

- Aunt and uncle (typically unacceptable but are sometimes allowed)

- Various other relations, including cousins (typically unacceptable but are sometimes allowed)

Seeing that a wide range of people you know can be guarantors, who among the people you know couldn’t be guarantors for a home loan?

Who can’t serve as a guarantor?

Many borrowers ask friends, relatives, or business partners to act as guarantors of their home loan.

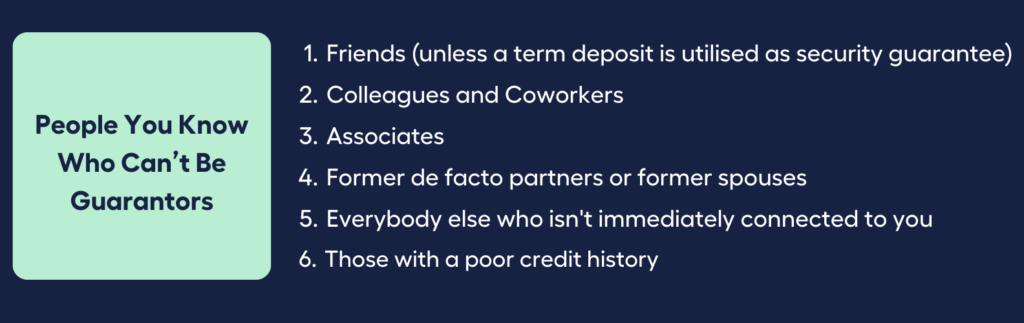

However, the guarantor must have a close relationship with you, hence the following individuals are typically not acceptable:

- Friends (unless a term deposit is utilised as security guarantee)

- Colleagues and Coworkers

- Associates

- Former de facto partners or former spouses

- Everybody else who isn’t immediately connected to you

- Those with a poor credit history

So, does this mean that parents can automatically provide loan security?

Can parents be a guarantor?

Yes, parents typically qualify for a family security guarantee.

But just like any candidate as guarantor, they need to check several boxes in order to help you obtain a guarantor home loan.

The guarantor you select must be in compliance with the lending institution’s standards.

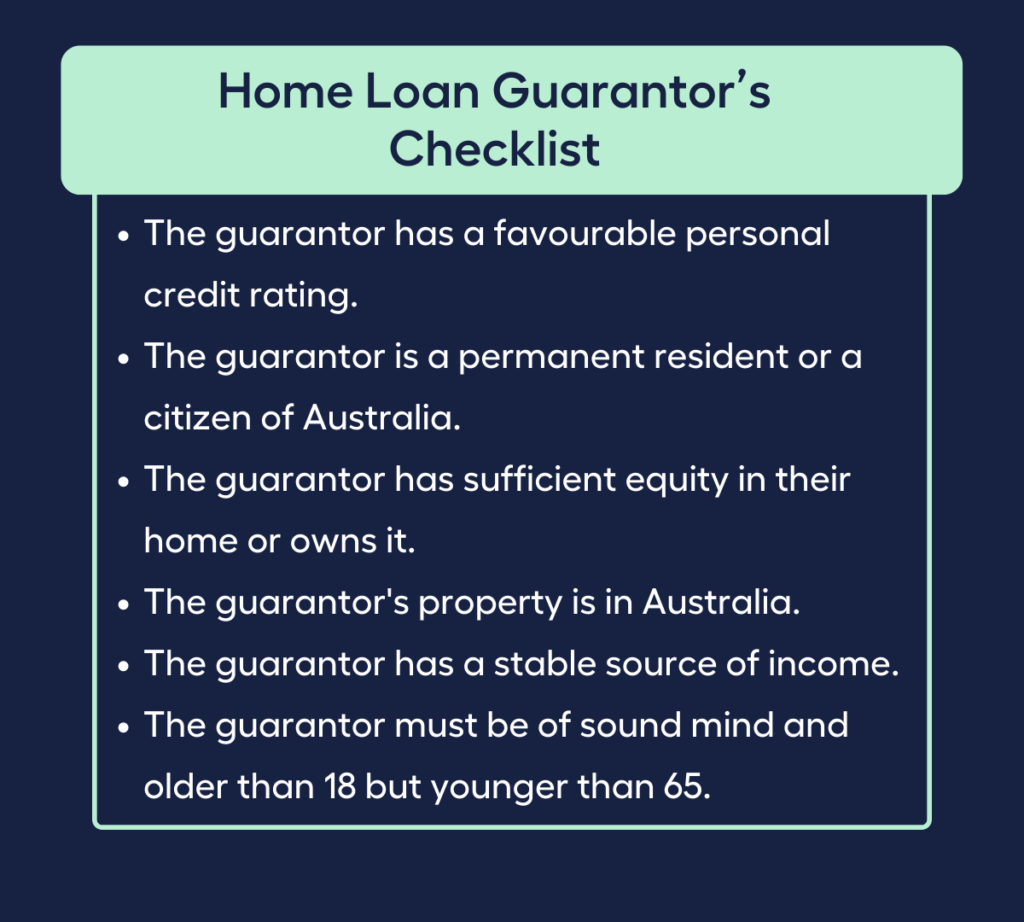

Home Loan Guarantor’s Checklist

1

Favourable Credit Rating

An obvious requirement for a guarantor is that they have a good credit rating. A person who has a poor credit rating offers lenders no security guarantee.

2

Residency

Typically, your guarantor must be an Australian citizen. Most lenders, though, will accept guarantors that reside and/or work abroad.

3

Sufficient Equity

The guarantor must either own their house entirely or owe less than 80% of the property’s value on their home loan.

There is no hard-and-fast rule here, but be aware that the less equity your guarantor has, the more difficult it will be to borrow 100% of the property value plus fees on your home loan in order to avoid paying a deposit and having to demonstrate true savings.

4

Guarantor’s Property Location

The property of the guarantor must be located in Australia. Banks won’t accept a foreign property as collateral for your home loan.

5

Stable Income

A guarantor needs to have a stable source of income but need not be employed or working. Although one with job security is ideal.

Each lender has a different policy, although most Australian banks won’t take a security guarantee from an elderly or retired guarantor.

If your guarantor is over 65 years old, they can be self-funded retirees or even get a pension as long as they seek legal counsel before accepting the loan offer and can demonstrate a viable exit route to the lender.

6

Age and Independent Legal Advice

A person must be older than 18 but younger than 65 in order to serve as a guarantor for a home loan. Older adults and retirees are rarely accepted to guarantee a loan.

Your guarantor must be of sound mind and must seek independent legal advice and financial advice before agreeing to the proposed loan.

Keep in mind that being a home loan guarantor entails a variety of risks and obligations.

What are the risks of being a guarantor?

Make sure you are aware of the risks and obligations in a guarantor home loan before agreeing to guarantee one. Just like if you were getting a home loan for yourself, exercise the same caution because the following scenarios can happen to you.

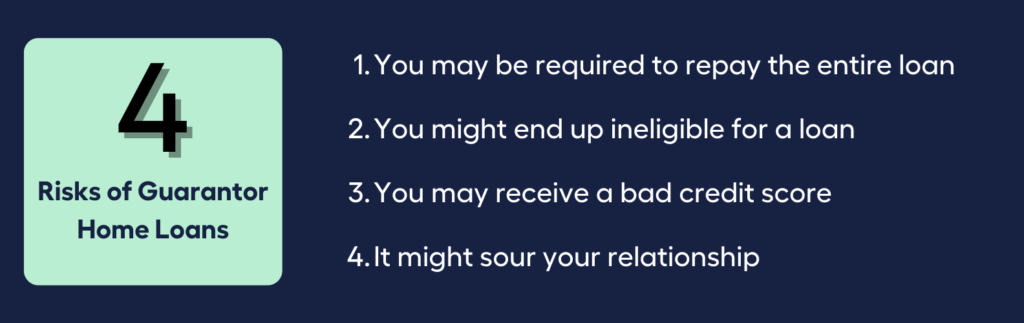

1. You may be required to repay the entire loan

You will be required to return the entire home loan amount plus interest if the borrower is unable to make mortgage repayments. And if you can’t make the home loan repayments, the lender could repossess what you used as security guarantee for the loan, such as your home or car.

2. You might end up ineligible for a loan

If you apply for another loan in the future, you must inform your lender if you are a guarantor on any other loans. Even if the home loan you guaranteed is being repaid, they might opt not to lend to you.

3. You may receive a bad credit score

Your credit report will reflect the guaranteed home loan as a default if you or the borrower are unable to repay it. You will find it more challenging to borrow money in the future.

4. It might sour your relationship

Your relationship may suffer if you act as a guarantor for a member of your family who is unable to repay the debt.

There may be alternatives to guaranteeing a home loan if you don’t feel comfortable doing so, such as helping to pay the deposit on a house.

In conclusion, here’s the key take away you need to remember about guarantor home loans:

A person guarantees or provides security for a home loan for another person in a guarantor home loan. Therefore, the guarantor is liable for repaying the loan amount if the borrower defaults or is unable to make payments.

If you want to know more about guarantor home loans or other types of loans, have a chat with My Money Sorted

Many people may be unaware of this…but just like you, 41% of Aussies intend to get financial advice rather than going it alone, according to an Australian Securities and Investments Commission (ASIC) report.

Find the right Mortgage Broker for you with the help of My Money Sorted

When you book a call with My Money Sorted, you’ll:

✓ get a better understanding of your home loan options

✓ have an idea of the experts you can call on to help you reach your goals

✓ be matched with a mortgage broker who can help develop the best home loan strategy for your situation

My Money Sorted is your stress-free pathway to getting ahead with your home loan.

Here’s what your journey will look like:

Step 1: Start off with a quick money matters session with My Money Sorted

Step 2: Get matched with a licensed Mortgage Broker that’s right for your financial situation

Step 3: Take the first step towards your financial goals with a clear roadmap that makes sense prepared by an experienced Mortgage Broker.

It’s that easy!

Need Mortgage or Home Loan Advice? Chat to My Money Sorted or Try Our Borrowing Power Calculator to Learn More.