The mortgage market is competitive, with lenders vying for new business by offering better home loans.

In this article, we’ll discuss why you should consider remortgaging a house, and look at how to find a better deal that could help you save thousands every year.

Jump straight to…

What Does It Mean to Remortgage a House?

When you remortgage your home loan, you move the amount you still owe on the loan from one lender to another.

During the process, you pay off your old mortgage early and you get a new mortgage. This gives you the chance to choose a home loan product that is completely different from the one you already have.

Remortgaging an existing loan can be a great financial move if you manage it correctly.

Remortgaging may allow you to do the following:

- lower your mortgage repayments

- shorten the length of your loan

- help you build equity faster

It can also be a useful tool for getting out of debt if it is used carefully.

What happens when I remortgage?

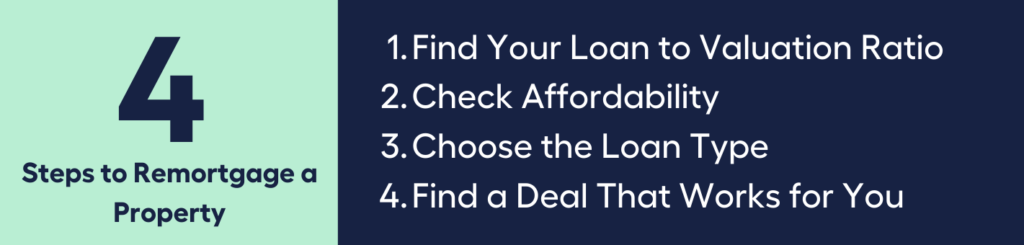

Remortgaging can be intimidating considering that you’re going to move into a new loan, but it may not seem so daunting when you consider there are only four main steps to follow.

1. Find your loan-to-value ratio (LVR)

- Loan to value (LVR) is a ratio a lender will use when assessing how much to loan you based on how much the house you want to remortgage is worth.

For example: if a lender offers a mortgage with a maximum LVR of 90%, it means that they will lend you up to 90% of the value of the property.

LVR is the amount you want to borrow divided by the value of your home multiplied by 100%.

In general, the majority of lenders view an LVR of 80% or above as risky. You can be required to pay for Lenders Mortgage Insurance (LMI) if your LVR is greater than 80%.

2. Check Affordability

Even if you already have a mortgage, that doesn’t mean you’ll be accepted the next time you apply for another home loan. And each lender has its own set of rules.

- A mortgage lender does a check to see how much they are willing to lend you on a home loan. This is called an affordability check.

Affordability checks help lenders determine if you will have the financial capacity to make repayments on your new mortgage. They’ll check how you would meet your repayments if your income went down or your debts got bigger.

3. Choose the type of loan you want

When it comes to the type of home loan you want, you’ll have a handful of options. You might want to opt for a fixed-rate mortgage or switch from a principal and interest mortgage to an interest-only mortgage.

4. Find a deal that works for you

When you know how much you can borrow and what kind of home loan you want, you can start looking for a good deal.

The mortgage market can be very confusing, so it’s best to work with an experienced mortgage broker who can do the legwork for you. It’s especially important if your situation isn’t simple, like if you have a bad credit rating or if the source of your income varies.

What’s the difference between refinancing and remortgaging?

In most places, the only big difference between remortgaging and refinancing is the name. For example, mortgage refinance is a common term in the United States, while remortgage is the more common term in the United Kingdom.

There is, however, a small technical difference between remortgaging and refinancing that should be kept in mind.

A remortgage means the borrower keeps the same lender, while a refinance means the borrower opts to go with a new lender.

Pros & Cons of Remortgaging

If you’ve had your existing mortgage for a few years, you may want to consider shopping around for a better mortgage deal.

- In a competitive mortgage market, there might be lower interest rates than what your existing lender currently offers.

But before you make a quick decision, think about the pros and cons below.

Benefits of Remortgaging

There are many reasons why a homeowner should look into remortgaging their home, here are some of the most common ones.

Obtain a Lower Interest Rate

One of the best reasons to remortgage is to lower the interest rate on your current mortgage deal.

In the past, it has been a good rule of thumb to refinance your home loan if you can lower your interest rate by at least 2%, but these days a 1% saving is enough of a reason to remortgage.

Reducing your interest rate can save you money and speed up the rate at which you build equity in your home. It can also make your loan repayment smaller.

- Use our refinance calculator to see how much you can reduce your principal and interest repayments.

Shorten the Loan Term

When interest rates go down, it can be a good opportunity for homeowners to refinance their home loan for a new one that has a much shorter mortgage term but the same monthly payment.

For example:

A $100,000 loan with a 30-year fixed-rate mortgage, refinancing from 9% to 5.5% can cut the term in half (from 30 years to 15 years) with only a small change in the monthly repayment (from $805 to $817).

However, if you already have a mortgage with an interest rate of 5.5% for 30 years, with a monthly repayment of $568, a mortgage with a 3.5% interest rate for 15 years would make your repayment significantly increase to $715. So figure out what works by doing the math.

Use our refinance calculator to see how much time you can save.

Change the Rate Type

Since interest rates fluctuate, remortgaging can help you take advantage of lower rates by changing your rate type.

Depending on your financial circumstances, you can switch from a variable-rate mortgage to a fixed-rate mortgage (or vice versa) at the end of an introductory period.

Variable-rate mortgages can go up over time, sometimes to a higher level than what you could get with a fixed-rate mortgage.

When this happens, switching to a fixed-rate mortgage gives you a lower interest rate and takes away your worries about interest rates going up in the future.

On the other hand, switching from a fixed-rate loan to a variable-rate mortgage with a lower monthly repayment can be a good financial move if interest rates are falling, especially for homeowners who don’t plan to stay in their homes for more than a few years.

These homeowners can lower their loan’s interest rate and monthly payment, but they won’t have to worry about what will happen to rates in 30 years.

Tap Your Equity

Another advantage of refinancing your mortgage is to get some cash out of your home’s equity.

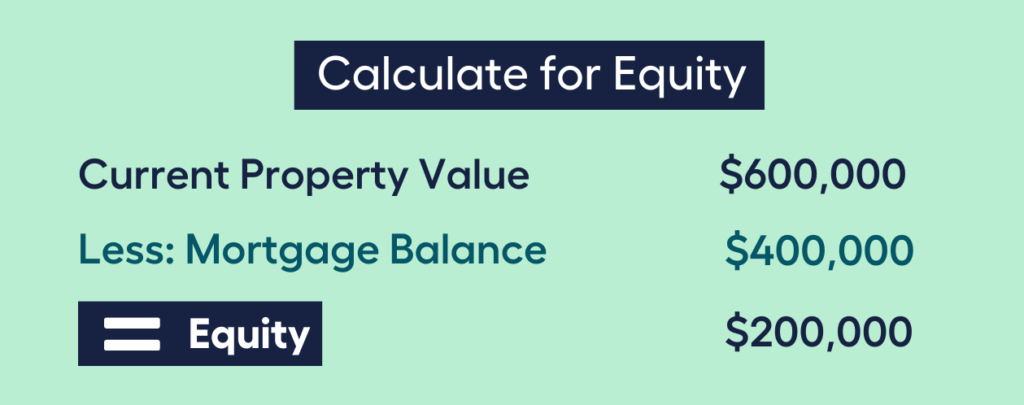

What is equity?

Equity is the difference between your current property value (how much your home is worth) and home loan balance (how much you still owe).

If you’ve lived in your home for a long time and have been making payments on the loan principal, it’s likely worth a lot more than what you owe on it. Your home’s value has also probably gone up since you bought it.

With a cash-out refinance, you basically take out a loan for more than the current balance and get the difference in cash. This is especially advantageous if you own your house outright or if your equity in the house is more than 20%.

Some people use this method to fund a renovation, pay off other debts, start a business, or pay for education costs.

Debt Consolidation

Getting rid of a lot of debt at once is another benefit of remortgaging. The idea is to get a home loan with a low-interest rate instead of having many high-interest personal loans like car loans and credit card debts.

While remortgaging does pack a lot of benefits, it carries some risks as well. Let’s dive in and see what these risks are.

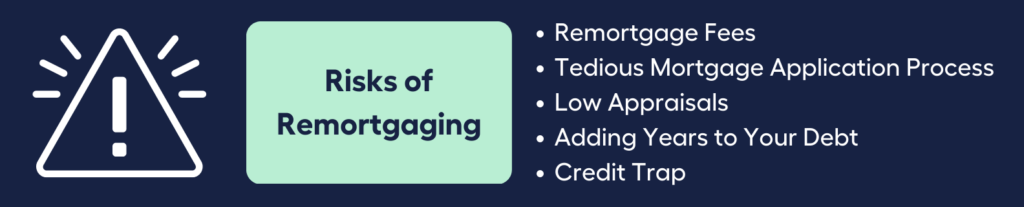

Risks of Remortgaging

Sometimes, getting the best deal can become risky if we fail to manage our finances properly or miscalculate on remortgage deals.

Here are some of the pitfalls you need to be aware of:

Remortgage Fees

Most people have trouble remortgaging because of how much it costs to get a new loan. When you remortgage, it’s important to know all of the fees you might have to pay, such as:

- Mortgage application fees

- Valuation fees

- Discharge fee or early repayment charge

- Break costs

- Settlement fees

- Registration fees

- Exit fees

- Legal Fees

Although low interest rates can seem attractive, you still need to consider if the lower interest rate is enough to offset the total cost of fees and still allow you to save money.

Tedious Mortgage Application Process

It takes time and effort to get a new loan. Also, the process could stop if you have bad credit or your income is reduced.

Here’s why:

- Mortgage lenders will look closely at your credit score and financial situation to see if you’re a low-risk borrower. If your credit score has changed, you might not get the best rates anymore.

Get ready to gather all sorts of paperwork (such as your tax information and a copy of your pay slip) to satisfy your mortgage lender’s questions.

Low Appraisals

If you’ve lived in your home for years, it’s hard to say how much it’s worth. This is why the mortgage lender will order an appraisal to get the current value of your property and find out how much equity you have.

An appraiser will typically use recent sales of similar homes in your location and any information you can give about your home’s size and features to figure out how much it is worth on the market.

When the appraisal comes back lower than expected, there could be issues you have to deal with:

- A low appraisal can make it impossible for you to get a new loan with better terms.

A possible scenario could be the appraiser might say that your home is worth less than what you still owe on it. To avoid this situation, property experts generally recommend refinancing when the value of homes in your area has gone up.

Adding Years to Your Debt

Another risk you need to be aware of is overlooking the cost-benefit of a new mortgage with a lower monthly repayment that may reset your home loan to its original loan term.

If you don’t do the sums and look into the details, you may pay more in interest over the life of the loan than you saved with the lower rate.

Credit Trap

Beware of the credit trap!

Many people who used to rack up high-interest debt on credit cards, cars, and other purchases are likely to do it again once they have the credit to do so after refinancing their mortgage.

This creates an instant quadruple loss:

- Wasted fees on the remortgage

- Lost equity in the house

- More years of higher interest payments on the new mortgage,

- Return of high-interest debt once the credit cards are maxed out again.

This could lead to an endless cycle of debt and eventual bankruptcy.

Now that you’re aware of both the benefits and risks of remortgaging, you’re probably wondering about the next steps you’ll need for a remortgage.

Let’s get right to it!

Do I need a solicitor to remortgage?

You don’t need a solicitor, aka conveyancer, to remortgage because your current lender will usually handle all the paperwork. But you might still want a solicitor to look over the paperwork and explain what it all means.

Most of the time, the fees for a solicitor are lower for a remortgage than for buying or selling a home. This is because there is less to do. It’s a good idea to shop around for a lender because some mortgage deals come with free legal support.

Do you need a deposit to remortgage?

If you’re about to start the remortgage process, you may be wondering if you have to put down a deposit first.

Most of the time, you don’t have to put down a deposit when you remortgage your home loan.

Instead, equity is one of the things that will determine whether or not you can remortgage. It works like a deposit when you first bought your home.

Equity backs up your new loan and lowers the financial risk for mortgage lenders.

- If you have at least 20% equity on your property, you could likely be able to remortgage without a guarantor.

The more equity you have in your home, the less risky you look to a lender. This can help you get that remortgage.

But don’t lose hope.

Even if you have less equity in your home, you can still remortgage. In this case, though, you might need to find a guarantor or pay for a lenders’ mortgage insurance (LMI) regardless of whether you’ve already paid for LMI on your current loan. This is to protect the lender if you don’t pay back the new loan.

If you have to pay LMI when you remortgage, you might want to consider if remortgaging is still the best choice for you.

Once you’ve figured out that remortgage will save you money, make sure to include any LMI you may have to pay on top.

Still not sure if a remortgage is advantageous for you at this time?

Find the best options for your situation by having a chat with My Money Sorted for free!

Many people may be unaware of this…but just like you, 41% of Aussies intend to get financial advice rather than going it alone, according to an Australian Securities and Investments Commission (ASIC) report.

Find the right Loan for you with the help of My Money Sorted.

When you book a call with My Money Sorted, you’ll:

✓ get a better understanding of your home loan options

✓ have an idea of the experts you can call on to help you reach your goals

✓ be matched with a mortgage broker who can help develop the best home loan strategy for your situation

My Money Sorted is your stress-free pathway to getting ahead with your home loan.

Here’s what your journey will look like:

Step 1: Start off with a quick money matters session with My Money Sorted

Step 2: Get matched with a licensed Mortgage Broker that’s right for your money situation

Step 3: Take the first step towards your money goals with a clear and sound roadmap prepared by an experienced Mortgage Broker

It’s that easy!