Are you a homeowner looking for ways to make the most out of your property’s equity?

One option that could be worth exploring is cash-out refinancing. While some may perceive it as risky or complicated, cash-out refinancing can actually offer a variety of benefits, such as lower interest rates, improved cash flow, and the ability to consolidate high-interest debt.

In this article, we’ll take a closer look at the advantages of cash-out refinancing, as well as some potential downsides to consider before making a decision. So if you’re curious about how you can leverage your home’s value to achieve your financial goals, read on to learn more.

Jump straight to…

What Does it Mean to Cash Out on a Refinance?

Cash-out refinancing is a process where you replace your current mortgage with a new one, taking out a larger loan than your existing balance. The difference between the new home loan and your existing home loan is paid out to you in cash.

- You can look at it as a way to tap into the equity you’ve built up in your home.

When you refinance your mortgage, you’re essentially getting a new loan with a new interest rate and payment terms.

Why Would You Do a Cash Out Refinance?

Refinancing, in general, can offer several benefits to homeowners by providing borrowers with the opportunity to negotiate more favourable terms, such as:

- lower interest rates,

- monthly payments,

- or changes in loan obligations.

In the case of a cash-out refinance, the homeowner can access the equity they have built up in their home and receive cash in hand, which can be used in different ways.

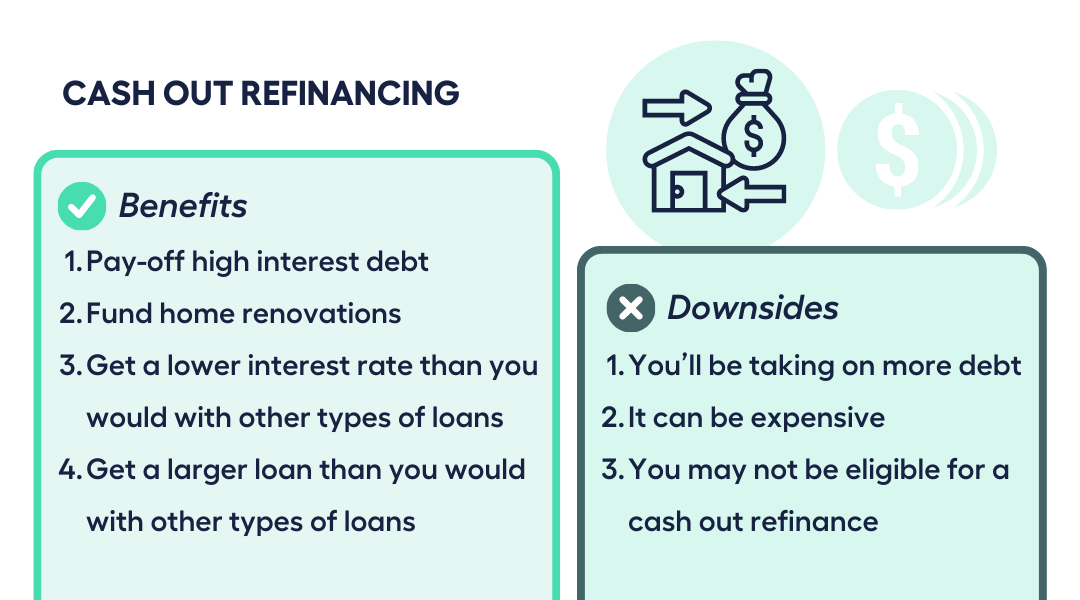

Benefits of Cash Out Refinancing

1. Pay off high-interest debt

If you have credit card debt or other loans with high interest rates, you could use the cash from a cash-out refinance to pay them off. This can save you money in the long run, since mortgage rates are usually lower than credit card rates.

How can you save money in the long run?

Debts with high interest rates and fees can make it harder to pay them off. By focusing on paying off the high interest debt first, you’ll owe less in interest and fees, which can help you pay off the debt quicker. This can free up more of your money to pay off other debts or save for other things you need.

- It can also improve your credit score, which can help you get better interest rates and terms for future loans or credit cards.

However, to avoid getting stuck in a never-ending loop of debt, it’s crucial to take the necessary measures to regulate your spending habits if you require the funds to settle your consumer debt.

2. Fund home renovations

Maybe you want to upgrade your kitchen, add a bathroom, or finish your landscaping. These projects can be expensive, but with a cash-out refinance, you can access the money you need to get them done.

Plus, home improvements can increase the value of your home, which could be a good investment in the long run.

3. Get a lower interest rate than you would with other types of loans

Since a mortgage is secured by your home when you do a cash out refinance, the lender is taking on less risk, which means they can offer you a lower rate than with unsecured loans, such as personal loans or credit cards.

In addition, cash-out refinance rates are typically lower than rates for home equity loans or lines of credit, which are also secured by your home but involve taking out a separate loan or line of credit. Cash-out refinances usually have longer repayment terms than other types of loans.

However, it’s important to note that the interest rate you can get with a cash-out refinance will depend on a variety of factors, including your credit score, income, and the current market conditions.

It’s also important to consider any fees and closing costs associated with a cash-out refinance, which can add to the overall cost of the loan. Before deciding to take out a cash-out refinance, it’s a good idea to compare rates and terms from multiple lenders to make sure you’re getting the best deal possible.

4. Get a larger loan than you would with other types of loans

If you need a lot of cash, a cash-out refinance may be a better option than a personal loan or a home equity loan.

You can potentially borrow a larger amount of money than with other types of loans because you are essentially refinancing your existing mortgage for more than you owe, and taking the difference in cash. This means that the amount you can borrow is based on the equity you have in your home, which is the difference between the current market value of your home and the amount you owe on your mortgage.

In contrast, other types of loans, such as personal loans or home equity loans, are typically based on your creditworthiness and income, and may not allow you to borrow as much as a cash-out refinance, especially if you have limited equity in your home.

Downsides of Cash Out Refinancing

While cash out refinancing may seem like a good idea to get some extra cash, it’s important to understand the potential drawbacks that can come along with it.

Let’s look at the downsides of cash-out refinancing so you can make an informed decision about whether it’s right for you:

1. You’ll be taking on more debt

A cash-out refinance involves resetting the terms of your mortgage and may result in:

- a bigger mortgage balance,

- higher monthly payments

- or a longer repayment period,

so it’s important to carefully consider the costs and benefits before deciding if it’s the right option for you.

2. It can be expensive

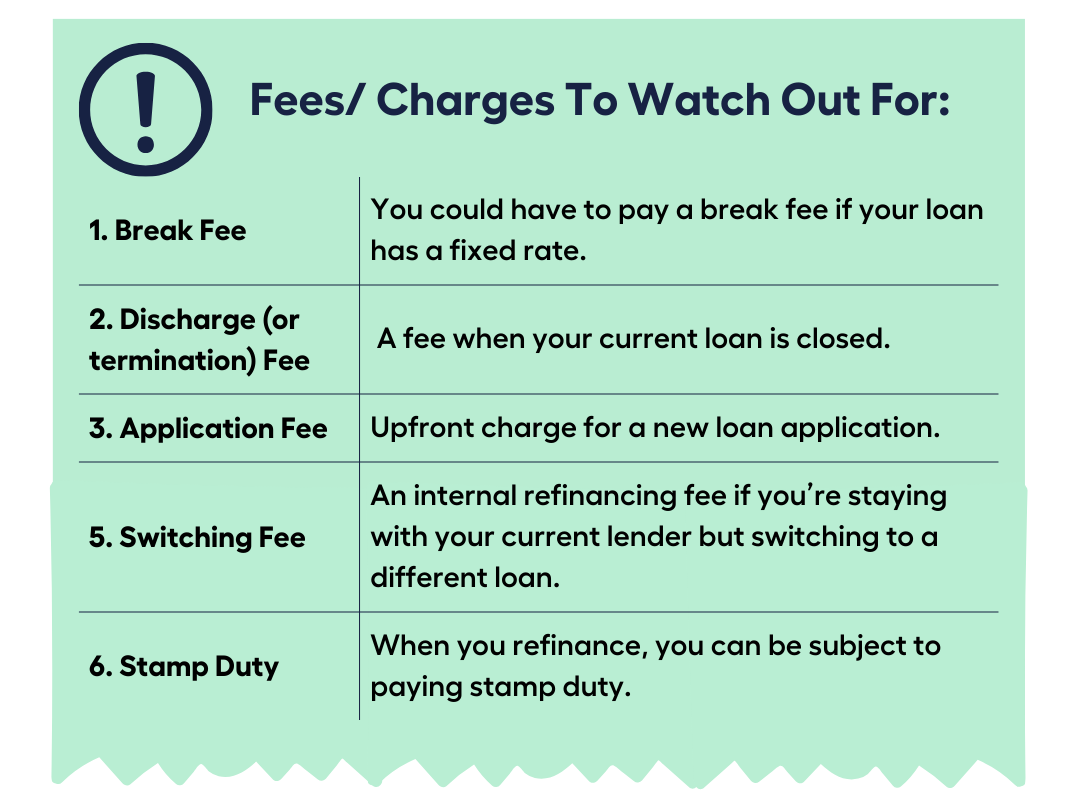

Most cash-out refinance options can have several additional costs and fees associated with them, which can add to the overall cost of the loan.

Before deciding to take out a cash-out refinance, it’s a good idea to compare rates and terms from multiple lenders to make sure you’re getting the best deal possible.

3. You may not be eligible for a cash-out refinance

If you don’t have enough equity in your home, or if your credit score and financial history don’t meet the lender’s requirements, you may not be approved for the cash-out refinance. This can be frustrating for homeowners who are counting on accessing some of their home’s equity to pay for expenses or consolidate debt.

How Cash Out Refinance Works

To begin the process, you must apply for a new loan with a lender. They will assess the value of your home, the intended purpose of the funds, and determine your eligibility for any additional borrowing.

If your loan is approved, upon settlement, your previous loan will be refinanced and the extra amount borrowed will be issued to you as cash.

For example:

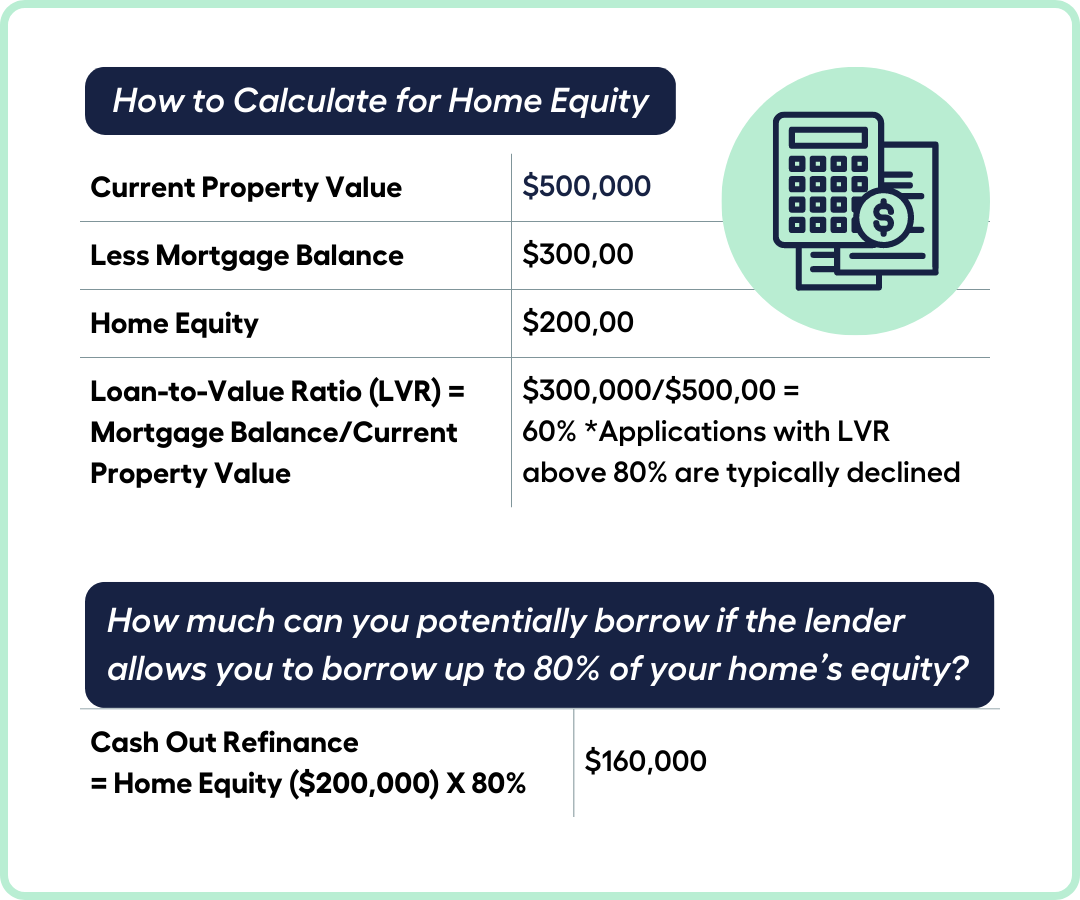

Your home’s current property value is $500,000 and you owe $300,000 on your mortgage, you have $200,000 in equity. With a cash-out refinance, you could potentially borrow up to a certain percentage of that equity, depending on the lender’s guidelines and your creditworthiness.

In this scenario, your Loan-to-Value Ratio (LVR) is 60%, which falls below the minimum threshold of 80% required to apply for a loan. Applications with an LVR exceeding 80% are usually declined. However, if the value of your property has appreciated since your purchase, you may be able to borrow against the capital gains.

Let’s say the lender allows you to borrow up to 80% of your home’s equity, which would be $160,000 in this case. So, with a cash-out refinance, you could potentially borrow up to $160,000 (minus any fees and closing costs) in addition to your existing mortgage.

How Long After a Cash Out Refinance Do I Get Money?

Typically, a cash-out refinance takes approximately 2-4 weeks, which is comparable to other types of refinancing. However, the timeline can vary based on various factors, such as your lender’s processing speed, your personal situation, and the prompt and accurate submission of the necessary documentation.

The required documentation for a cash-out refinance may include:

- your ID

- payslips

- bank statements

- home valuation

- insurance

- proof of how you intend to utilise the funds

How is a Cash Out Refinance Paid Back?

Now, let’s talk about how a cash-out refinance is paid back. It’s important to understand that when you take out a larger mortgage, your monthly payments will likely increase because you’re borrowing more money.

Is it Worth Doing a Cash Out Refinance?

Well, that depends on your individual situation. You may want to consider these things before making a decision:

First, you need to think about how much equity you have in your home. You can access more cash if you have more equity. If your equity is less than 20%, though, you may have to pay Lenders Mortgage Insurance (LMI); if it’s too high, a refinance may not be worthwhile.

Next, you need to determine how much money you’ll need and for what. Paying off personal or credit card debt with cash-out refinancing might be a wonderful choice, but it’s vital to manage the funds carefully.

Moreover, think about how refinancing would affect your monthly payments. Although there are up-front expenses like assessment and application fees, you may well be able to offset these with reduced monthly home loan repayments if you reset your home loan term and negotiate a lower interest rate. Just keep in mind that even if interest rates rise, you still need to make your mortgage payments on time.

If you plan on keeping your home for the long term, cash-out refinancing may be a good option for you. This way, you can balance the closing costs with lower monthly repayments, especially if you were able to refinance at a better interest rate.

In closing, before you make the decision to do a cash-out refinance, do your research and make sure it’s the right choice for you.

Do the maths and make sure you can afford the new monthly payment. As always, consider consulting with a finance expert to help you make the best decision for your individual situation.

Learn More About Cash Out Your Refinancing Options – Book a FREE 15min Call or Send Us Your Questions!

I Want to See All My Options with the Help of a Finance Expert

Book a FREE Call TodaySOURCES:

https://moneysmart.gov.au/home-loans/switching-home-loans

https://www.lendi.com.au/inspire/finance/how-to-refinance-a-home-loan-and-get-cash-out/

https://www.investopedia.com/terms/c/cashout_refinance.asp

https://www.joust.com.au/home-loan-refinancing/cash-out-refinance

https://www.mortgagechoice.com.au/blog/refinancing/2021/07/how-long-does-it-take-to-refinance/