If you don’t have a big amount of money saved up for a deposit, purchasing a home can feel like an uphill battle due to the significant financial commitment involved.

But don’t jump ship just yet!

Those looking to enter the real estate market without incurring a hefty up-front expense have options such as the low deposit and no deposit home loans that could enable Australian homebuyers to jump on the property ladder.

In this post, we’ll explore no deposit and low deposit home loans, how they work, and whether they could be the right choice for you.

Continue reading to learn more about these alternative lending options if you’re considering buying your first home or upgrading to a new one.

Jump straight to…

Is it Possible to Get a Home Loan Without a Deposit?

While it may seem like a mountain to climb, there are home loan types that make it easier for homebuyers to get into the property market.

Let’s dive in and find out how you can make your dream of owning a home a reality, even if you don’t have a large sum of money saved up

Low or No Deposit Guarantor Home Loans

So, you’re thinking of buying a house but don’t have any savings for a deposit?

When it comes to getting a home loan with low deposit or no deposit, you do have a few options.

Low Deposit Home Loan

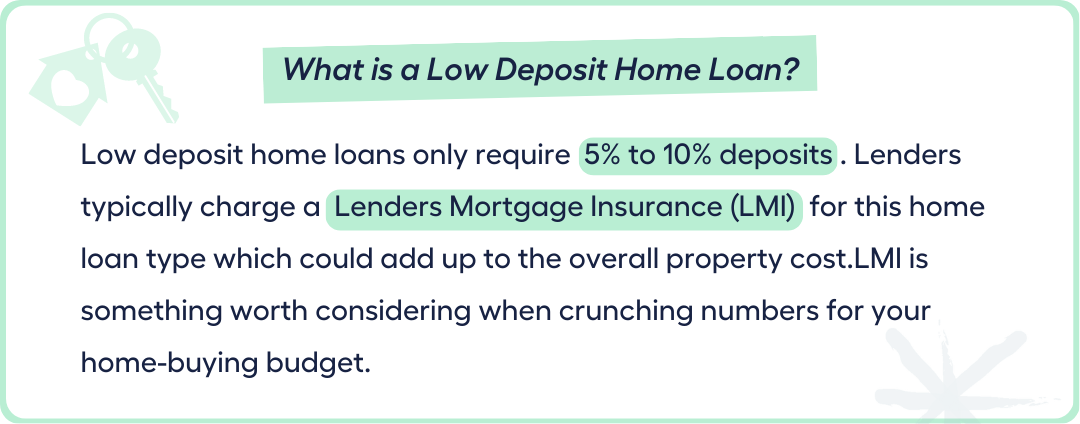

In Australia, the usual deal when buying a property is to put down a 20% deposit. But, let’s be real, that’s a pretty big chunk of change to save up, especially with how pricey houses are these days.

This is where low deposit home loans come in. This home loan type only requires 10% or even just 5% deposits. That means you may be able to save up less, borrow more, and get into your own place sooner.

Nevertheless, there is a slight catch:

Lenders charge you with what is known as a lenders mortgage insurance (LMI) premium if your deposit amount is less than 20%. The LMI could increase your property purchase costs by thousands of dollars. So, it’s worth keeping that in mind when you’re weighing up your options.

Saving for a 20% deposit can feel like running a full marathon, leaving prospective buyers feeling like they’ll never make it to the finish line. That’s why some turn to low deposit loans, even if it means shelling out extra cash for LMI costs.

While it may not be the ideal solution for everyone, it can be a tempting option for those who are eager to get their foot in the door of their dream home and the property market.

And why is this so?

Here are some of the advantages of a low deposit home loan:

1. You can enter the property market sooner with a low deposit.

For example, a 20% deposit on a $600,000 home would cost $120,000, compared to a 10% deposit of $60,000 and a 5% deposit of only $30,000.

With a smaller deposit, you can save it up quicker and get on the property ladder sooner.

2. No more fear of missing out (FOMO) on good deals. Rising property prices won’t be a concern once you’ve bought in.

3. If you’re already a homeowner, you can focus on home loan repayments and building equity instead of just building up a deposit.

However, like what was mentioned earlier, keep in mind that low deposit home loans come with more costs like LMI.

The amount of LMI premium you’ll need to pay can vary widely, depending on factors like the size of your deposit and the overall cost of the property you’re eyeing. This could end up being anywhere from a few thousand to tens of thousands of dollars, so it’s definitely not something to take lightly when crunching the numbers for your home-buying budget.

No Deposit Guarantor Home Loans

If most lenders won’t allow you to borrow 100% of the value of your house and would typically just lend up to 95% and require a minimum 5% deposit, is there a workaround for this if you have zero savings for a deposit?

Yes, there is:

- A no deposit guarantor home loan.

With a guarantor home loan, you might be able to use your parents’ (or another family member’s) property to secure a loan.

Basically, your parents are offering their property as additional security for your home loan.

- This means you can potentially borrow 100% of the property’s purchase price. The majority of the loan (80%) will be secured on the property you’re buying, and the remaining 20% will be secured on your parents’ property.

It’s an option worth considering if you’re struggling to get the cash together for a deposit.

However, it’s important to remember that if you can’t repay the loan, your parents could potentially lose their property.

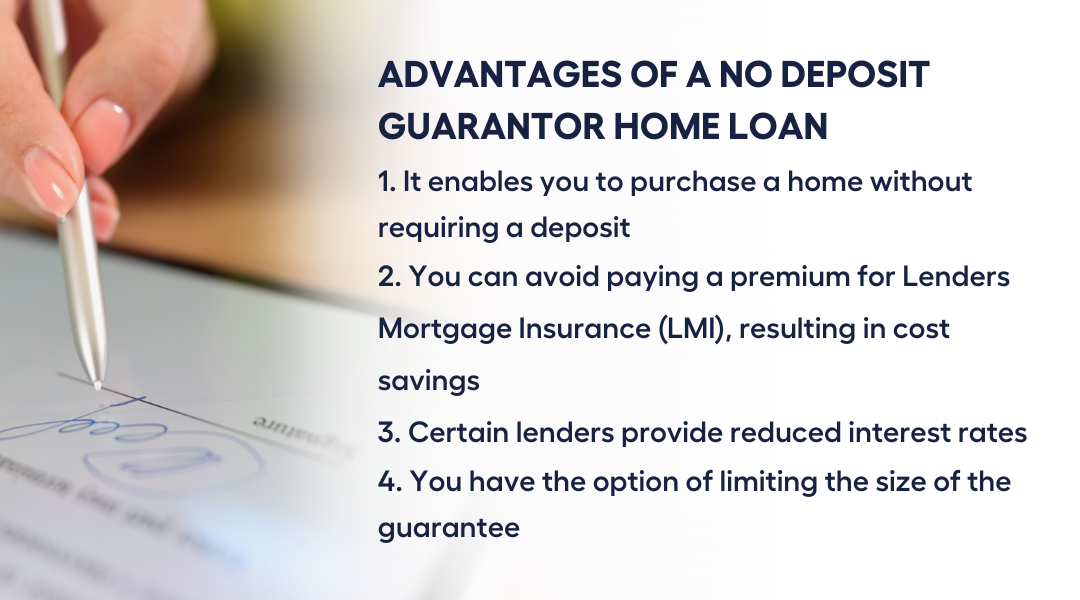

What are the advantages of a guarantor home loan?

- It enables you to purchase a home without requiring a deposit

- You can avoid paying a premium for Lenders Mortgage Insurance, resulting in cost savings

- Certain lenders provide reduced interest rates

- You have the option of limiting the size of the guarantee

While a guarantor home loan could benefit a homebuyer with no capacity to shell out cash for a deposit, it is also worth considering if the prospective guarantor is in a good position to provide additional security to a home loan.

Here are some important things to keep in mind before agreeing to become a guarantor:

1. Check your finances

It’s crucial to understand your own financial situation and that of the person you’re guaranteeing for. You don’t want to end up paying someone else’s mortgage. So, take a good look at your finances before making any commitments.

2. Consider your relationship

The closer you are to the person you’re guaranteeing, the better it is for you. If anything goes wrong, you may have a better chance of recovering your money.

3. Keep the loan size in check

You can further reduce your risk by ensuring that the loan doesn’t exceed 90% of the property value. This way, you won’t have to worry about paying more than you can afford if something goes wrong.

4. Seek professional advice

It’s always a good idea to speak with a professional, such as a financial or legal advisor, before making any guarantees. They can give you valuable advice on how it will affect your finances and help you make an informed decision.

- Remember, being a guarantor can be a big responsibility, so take the time to weigh all your options before making any commitments.

Limited Guarantee

If your guarantor is willing to help secure a home loan but would like to reduce the risk as a guarantor, there’s the option of limiting the size of the guarantee (mentioned as one of the advantages of a guarantor home loan).

Here’s how a limited guarantee works:

Instead of securing the entire loan amount like in a standard guarantor loan, the guarantor only guarantees a portion of it.

Like with a regular guarantor loan, the guarantor needs to offer up their property as extra security for the lender. The difference is that the guarantor is only responsible for a portion of the borrower’s mortgage, not the entire thing.

That way, if something goes wrong, the guarantor’s only responsible for a smaller amount and not the whole amount. This can give the guarantor some peace of mind while still extending help to the borrower to secure a loan.

Sounds pretty good, right?

But keep in mind that limited guarantees can be a bit complex, so it’s important to fully understand how it works before committing to anything.

Overall, a limited guarantee can be an option if you want to help someone secure a loan but don’t want to take on too much risk. Just make sure you do your research and consider seeking professional advice before making any decisions.

Low or No Deposit Home Loan for First Home Buyers and Low Income Earners in Australia

Did you know that there are a number of low or no deposit federal and state grants and schemes available for first-time homebuyers?

Even so, numerous polls have revealed that first-time homebuyers frequently are not aware of these programmes.

Let’s dive into these grants and schemes that will still be available to first-time homebuyers in 2023 which could help you embark on your home ownership journey.

Government Home Loans

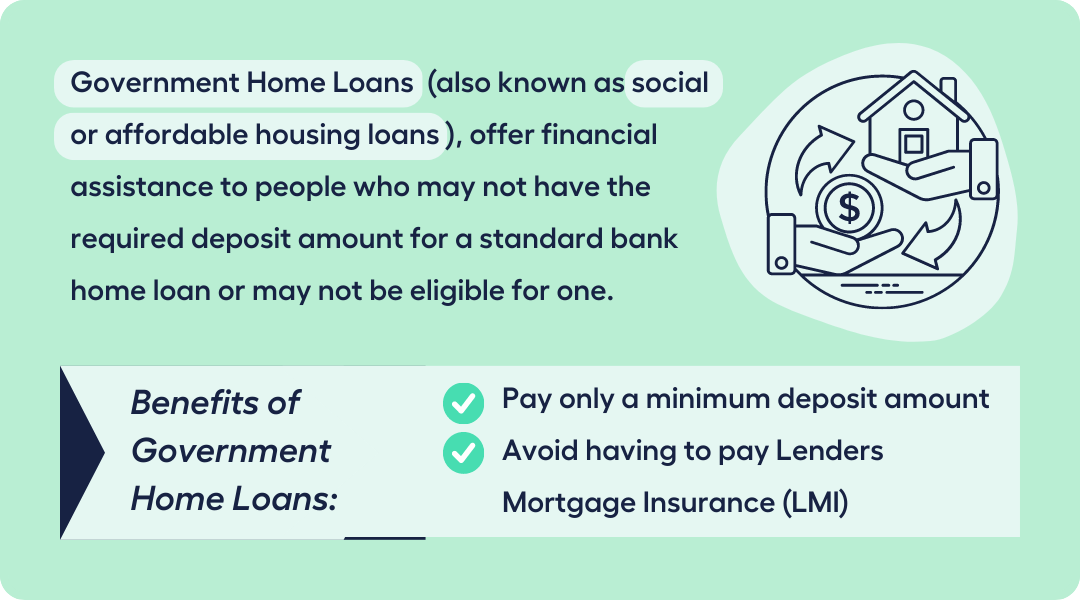

Government Home Loans (also known as social or affordable housing loans), offer financial assistance to people who may not have the required deposit amount for a standard bank home loan or may not be eligible for one.

The great thing about these loans is that eligible homebuyers can benefit from various government help options, including federal and state government home loan assistance, as well as indigenous home loans.

With any of these schemes, homebuyers can generally count on 2 benefits:

1. Paying a minimum deposit amount

2. Avoiding having to pay lenders mortgage insurance (LMI).

These features can be a huge help to those who are struggling to come up with a large deposit or who may not have the financial resources to cover the LMI costs associated with a traditional home loan.

Basic Requirements for a Government Home Loan Program

The government home loan programs vary in terms of their specific requirements depending on the type of product and the state offering it. However, there are some common requirements that all these programs share.

In order to qualify for these programs, borrowers typically need to meet certain criteria:

- Be a citizen or permanent resident

- Be a first-time homebuyer

- Meet income and asset limits

- Purchase a residential property within certain price limits

Apart from meeting these requirements, borrowers will also need to show that they can repay the loan by providing evidence of their income, employment, and credit history. These requirements are put in place to ensure that borrowers are financially capable of repaying the loan and to mitigate the risk of default.

Federal Government Home Loan Assistance

The National Housing Finance and Investment Corporation (NHFIC) is in charge of overseeing the Australian Government’s Home Guarantee Scheme (HGS), which aims to speed up the home-buying process for qualified buyers.

These are the schemes designed to assist specific groups of first home buyers with access to financial support and government-backed guarantees to help them purchase a home sooner and with greater ease:

First Home Guarantee/First Home Loan Deposit Scheme

Qualified first-time homebuyers can benefit from the First Home Guarantee Program (FHBG), formerly known as the First Home Loan Deposit Scheme (FHLDS), which involves the NHFIC providing a guarantee on a portion of their home loan obtained through a Participating Lender.

- The NHFIC guarantees up to 15% of the residential property’s assessed value by the lender

- Eligible buyers may be able to purchase a home with as little as a 5% deposit without having to pay LMI

- Available from 1 July 2022 until 30 June 2023, 35,000 available FHBG places

Family Home Guarantee

Eligible single-parent borrowers with at least one dependant child can take advantage of the Family Home Guarantee.

- Limited to a maximum of 18% of the residential property’s assessed value by the Participating Lender

- Purchase a home with a minimum deposit of just 2% and avoid paying Lenders Mortgage Insurance (LMI)

- For the period of 1 July 2022 to 30 June 2023, there are 5,000 FHG places available

Regional First Home Buyer Guarantee (RFHBG)

The Regional First Home Buyer Guarantee (RFHBG) is an initiative designed to support eligible first-time home buyers in regional areas. Under this scheme, the NHFIC guarantees a portion of their home loan from a Participating Lender.

- Limited to a maximum of 15% of the residential property’s assessed value by the Participating Lender

- Purchase a home with just a 5% deposit and avoid paying Lenders Mortgage Insurance (LMI)

- From 1 October 2022 until 30 June 2023, there are 10,000 RFHBG places available

State Government Home Loan Assistance

Home loan assistance programs are available in various states, and they typically involve shared equity schemes. Under such schemes, the buyer and the government share the cost of making a deposit.

However, the government receives a portion of the residential property’s value as part of the agreement. It’s worth noting that not all state government home loan assistance programs involve shared equity schemes.

Keystart (Western Australia)

Founded in 1989 by the Western Australian government, Keystart aims to assist residents of Western Australia who are unable to meet the deposit requirements of traditional lenders. Keystart provides Low Deposit Home Loans to those who earn below a specific income threshold.

- In metropolitan areas, a deposit of 2% is required

- In rural areas, 10% deposit is required

HomeStart Finance (South Australia)

In 1989, the Government of South Australia created HomeStart to accelerate the home ownership process for South Australians. HomeStart offers various advantages, such as increasing borrowing capacity and reducing the amount required for a deposit. HomeStart home loans replace the need for Lenders Mortgage Insurance (LMI) with a less expensive loan provision charge.

- Offers loans to specific customer groups at a 97% LVR

- Offers a Shared Equity Option, which covers between 5% and 25% of the home’s value

Queensland Housing Finance Loan

The Queensland Housing Finance Loan provides eligible residents of Queensland with an opportunity to purchase or construct a home with a low deposit. The loan is structured in a way that makes repayments more manageable by considering borrowers’ income when calculating repayment amounts, in addition to loan size, term, and interest rates.

- Initial monthly payments are set at 30% of the borrower’s income and capped at 35% of that amount

- Just a 2% deposit requirement and no Lenders Mortgage Insurance (LMI) needed

Victorian Homebuyer Fund

The Victorian Homebuyer Fund is a shared equity scheme that involves the Victorian Government contributing funds towards the purchase of a home and receiving an equity share in the property that can be repurchased by participants over time.

- Eligible participants in the scheme can receive up to 25% of the purchase price of the home from the Victorian Government

- Participants are required to contribute at least 5% of the purchase price and cover any acquisition costs like conveyancing fees and stamp duty

- Remaining balance is secured through a home loan obtained from a partner lender

Indigenous Business Australia Home Loans

Indigenous Business Australia (IBA) offers home loan assistance to Aboriginal or Torres Strait Islander home buyers through the Indigenous Home Ownership Program. Eligible borrowers can qualify for loans with low deposits under this program.

These low or no deposit government home loans might completely change the game for eligible first home buyers. You may want to consider these alternatives to turn your aspirations of owning a home into a reality.

Can I Use My Super for a House Deposit?

While investors can purchase investment properties through a self-managed super fund loan, first home buyers can indirectly use their extra super contributions towards a deposit through the First Home Super Saver Scheme (FHSSS). This allows them to minimise tax and potentially increase their savings for a deposit.

- Eligible first-time homebuyers can take advantage of the FHSSS, a scheme established by the Commonwealth government to increase their savings by making additional contributions to their super fund.

The contributions made under this scheme are taxed at the lower superannuation tax rate instead of the original income tax rate.

By using the extra voluntary contributions, some first home buyers may be able to save up for their home deposit more quickly.

Do you want to determine how much money you can potentially borrow from a lender based on your income, expenses, and other financial commitments?

Check Your Borrowing Power with MMS Loan Calculator

If you want to understand how different loan terms and interest rates can impact your borrowing power and monthly repayments so you can make informed decisions when comparing loan products and finding a loan that suits your financial situation and goals, give our team a call.

Want to Know More About Home Loan Opportunities? Book a FREE 15min Call or Send Us Your Questions!

I Want to See All My Options with the Help of a Finance Expert

Book a FREE Call TodaySOURCES:

finder.com.au/low-deposit-home-loans

homeloanexperts.com.au/no-deposit-home-loans/

homeloanexperts.com.au/guarantor-home-loans/

mozo.com.au/home-loans/resources/guides/zero-deposit-home-loans/163

homeloanexperts.com.au/guarantor-home-loans/limited-guarantee/

homeloanexperts.com.au/first-home-buyers-guide/government-grants-schemes-new/

homeloanexperts.com.au/low-deposit-home-loans/help-to-buy-new/

nhfic.gov.au/support-buy-home/family-home-guarantee

nhfic.gov.au/support-buy-home/first-home-guarantee

qld.gov.au/housing/buying-owning-home/financial-help-concessions/qld-housing-finance-loan

dtf.vic.gov.au/funds-programs-and-policies/victorian-homebuyer-fund