Compared to many other investment types, houses and units appear to be simpler to understand.

After all, we’ve been living in houses all our lives.

How complicated can property investment be?

Property investment is frequently regarded as less risky than other types of investment. While it may appear to be simpler, there are several hazards to be aware of.

Investors may not have a crystal ball to predict the future of their property investment, but wise investors make informed decisions about their investments.

In this article, we’ll discuss what information you need to know before investing in real estate to help make better decisions about what options are right for you.

Jump straight to…

- Understanding the Value of Location

- 4 Things To Consider When Evaluating a Location

- Research Before Investing In Property

- Investment Loan Options

- Expected Cash Flow and Long-Term Appreciation Projections

- Available Tax Benefits

- Find the right Financial Adviser for you with the help of My Money Sorted.

- Wanting to Invest in Real Estate? Chat to My Money Sorted to Find Out More

Everything You Need to Know Before Committing to Real Estate Investing

There are various factors that influence whether or not an investment property is suitable for your financial situation and personal objectives.

Understanding these factors can potentially limit your costs and even help make the most of your investments to increase your profits from real estate investment.

Here are a few of the most important factors in real estate investing to consider if you intend to invest in the property market.

Understanding the Value of Location

“Location, location, and location!”

This has long been the mantra of those who choose property investing over other forms of investments.

It’s often repeated for a reason:

Location is an important factor when investing in real estate. This is true for both investors and prospective tenants.

So it’s best to conduct thorough research when evaluating the location of a potential real estate investment.

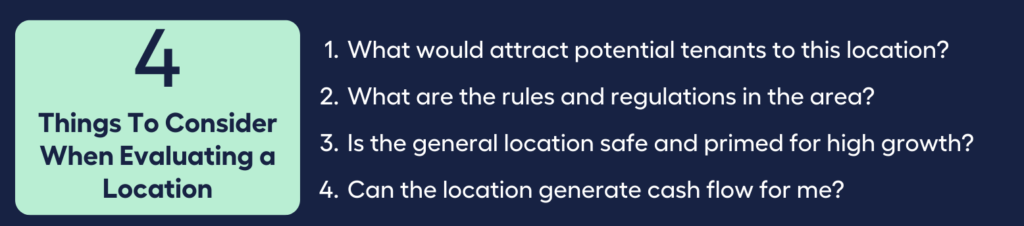

4 Things To Consider When Evaluating a Location

1. What would attract a potential tenant to this location?

Think about what potential tenants would want in a rental property by putting yourself in their shoes.

The property will be more appealing to tenants if it is accessible. That means it is close to public transportation, schools, and other things that are important to most people, like shops and restaurants.

2. What are the rules and regulations in the area?

There are a number of other things going on in every region that can affect your profit in different ways.

For example:

- A region’s laws about short-term rentals can limit potential profit through platforms like Airbnb because of licensing requirements and other regulations.

- There is a chance that rent control laws in the area will limit the number of days per year the property can be used as a short-term rental.

- The socio-economic profile of a neighbourhood has a big effect on the traditional rental market (which can greatly affect rental income).

3. Is the general location safe and primed for high growth?

In a broader sense, the safety and general vibe of a neighbourhood are both important things to consider when figuring out how much the location can grow.

For example, if the area is likely to be redeveloped and get more shops and cafes, or if there are big infrastructure projects that could bring more jobs to the area and attract potential tenants, these things may make the location of the property more desirable since it can foster capital growth.

Capital growth is essentially the increase in the value of a property over time. Evaluate the long-term growth indicators for the property you want to invest in.

Ask:

What is the median sale price in the suburb?

Has it increased in recent years?

Websites like realestate.com.au can give you a clear picture of Australian property and suburb trends, including previous sales in the region, demographic information, neighbouring schools, and median rental income.

This information can help you project your capital gains (i.e., how much money you gain based on the capital growth of the property) for the investment property.

4. Can the location generate cash flow for me?

- The value and rental income of a property investment is heavily influenced by the neighbourhood in which it is located.

Location also dictates the type of property in demand and the cash flow it can generate.

A house with a backyard, for example, will likely be more attractive and have higher perceived value to tenants in a family-friendly neighbourhood than a compact apartment.

While a modern apartment may be in higher demand in neighbourhoods near universities and public transport, where there is typically a significant amount of students and single occupiers looking to rent.

Remember:

It is critical to understand the demographics of the area and make appropriate choices.

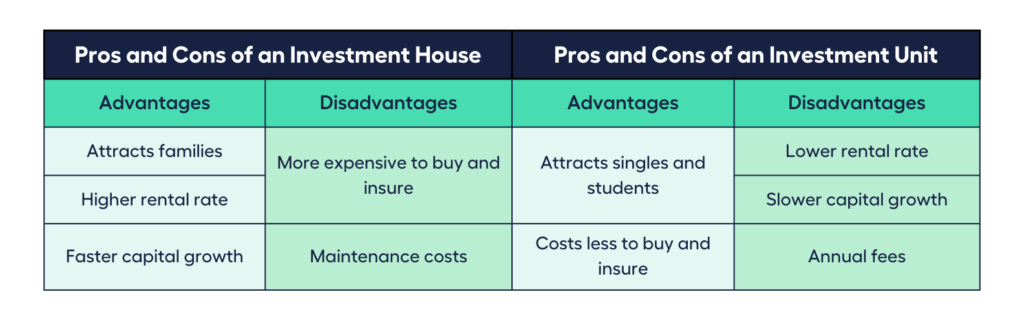

Houses are normally more expensive to acquire and insure, and they may necessitate more maintenance, but they can also command higher average rental income and have faster capital growth than units.

On the other hand, units often start at a cheaper price range and require less maintenance, but there may be other costs to consider that will eat away at the rental income you receive, such as strata fees.

In reality, strata fees are simply one of a number of ongoing costs to consider when considering whether to buy a house or an apartment.

The main goal of an investment property is usually to grow wealth and generate a passive income.

This means you need to consider other factors aside from location to ensure your rental property will generate income that will meet your investment goals.

Research Before Investing In Property

Once you’ve narrowed down the location in which you want to buy an investment property, it’s time to scope out the properties in the area, begin assessing them for fit with your investment criteria, and crunching your numbers to determine what kind of cashflow you can expect.

Maintenance Expenses

One of the things you need to consider is how much it would cost you to keep the investment property in good condition.

Let’s start with the fundamentals of property maintenance.

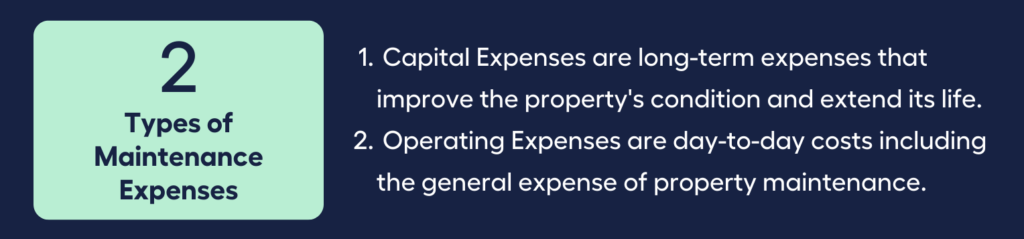

The 2 Types of Maintenance Expenses:

1. Operating Expense

2. Capital Expenses

Understanding this simple split will help project future income outflow from your rental property.

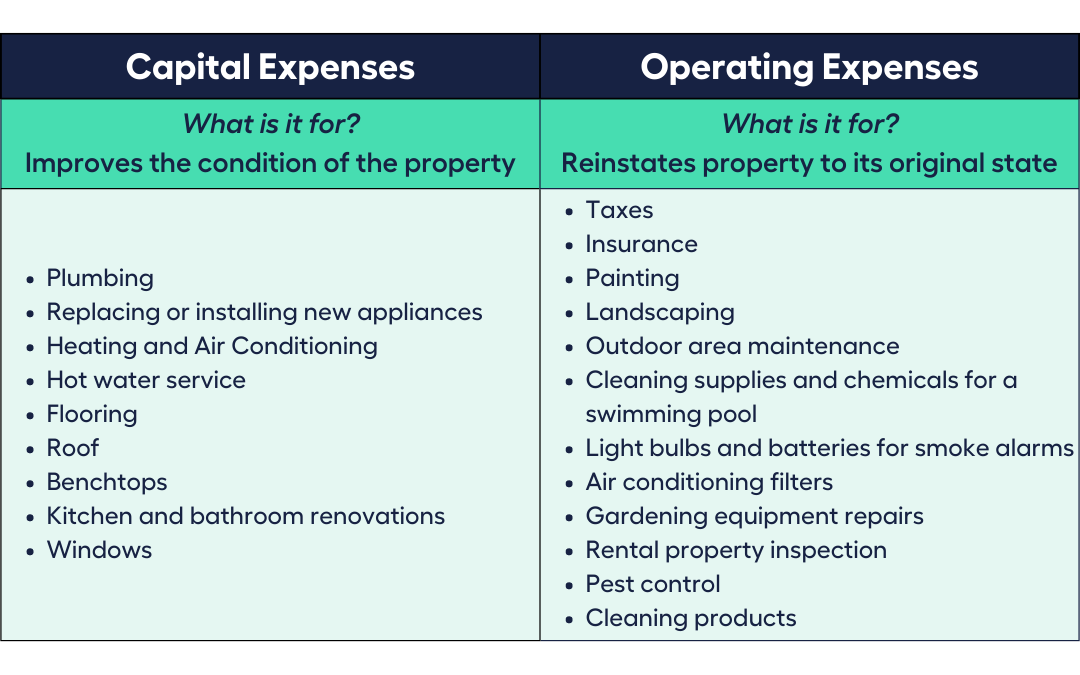

Capital Expenses

Capital Expenses (CapEx) are major long-term expenses made to enhance the investment property’s condition and extend its life.

The value of the property may decline if it is not properly maintained. As a result, you should see CapEx as an investment rather than a property maintenance bill that affects your revenue.

Tenants prefer a well-maintained property than one in desperate need of repairs and replacements.

Capital expense items include:

- Plumbing

- Replacing or installing new appliances

- Heating and Air Conditioning

- Hot water system

- Flooring

- Roof

- Benchtops

- Kitchen and bathroom renovations

- Windows

Based on the age and existing condition of the property, you’ll be able to assess how long each of the above items may last. You’ll be able to tell when it’s time to replace or improve them.

Operating Expenses

Operating Expenses (OpEx) are day-to-day costs that include general property maintenance as well as taxes and insurance.

Some of these costs need to be taken into account once a year or twice a year, while the rest may come up without warning. So, it’s smart to do regular inspections to find problems before they get worse.

Here is a list of the maintenance costs associated with maintaining a rental property that you should keep in mind:

- Painting

- Landscaping

- Outdoor area maintenance

- Cleaning supplies and chemicals for a swimming pool

- Light bulbs and batteries for smoke alarms

- Air conditioning filters

- Gardening equipment repairs

- Rental property inspections

- Pest control

The cost of property maintenance is determined by a variety of factors, including the property’s size, condition, and age.

The type of property, whether it is a single-family home, townhouse, unit or apartment, also influences the amount of upkeep required.

Larger houses, for example, with extensive landscaping and additional features, may necessitate a higher maintenance budget.

Estimating Operating Expenses

There are a few different ways to estimate annual maintenance expenses. Let’s have a look at some of them.

Ways to Estimate Annual Maintenance Expenses –

- The 1% Rule: The 1% rule assumes that the cost of maintaining a residential property for one year is equal to 1% of the property’s value. If you own a $500,000 home, maintenance is expected to cost $5,000 each year.

- The 5x Rule: The 5x rule assumes that annual maintenance costs are typically equal to 1.5 times the gross monthly rent. So if the monthly rent is $1,000, the maintenance budget is $1,500 per year. If you’re stuck on how to estimate your annual operating expenses, it can help to speak with a property manager who has experience managing rental properties similar to the one you are considering investing in. Now that we’ve identified maintenance expenses and how to budget for them, it’s time to look at the overheads of owning an investment property.

Overheads of Owning Property

Before deciding to purchase an investment property, it is critical to understand not only the initial costs and maintenance expenses, but also the recurring costs outside maintenance expenses.

Home loan/Mortgage repayments and fees

This might include the interest paid on your home loan as well as any associated bank and loan maintenance fees, depending on the type of loan you’ve taken out.

For the first few years of owning an investment property, it’s customary for investors to pay only the interest on their loan (also known as interest only instalments), rather than principal plus interest repayments.

Check with your lender if you can make interest only payments on your home loans for up to ten years on your investor home loan.

Council rates

Council rates vary according to location but these are commonly required annually and are often due every quarter to cover essential services such as garbage collection and the upkeep of community amenities such as parks, roads and footpaths.

For additional information, see the website of the council where you intend to purchase an investment property.

State government taxes

These vary by state and territory, but the majority levy an annual land tax which may be applicable unless you meet the land tax exemption criteria. Always seek the advice of a taxation accountant to ensure you have an accurate picture of your tax obligations.

Strata or corporate fees

If you own a property that is on shared land or title, such as an apartment or townhouse, you may be required to pay these fees on a quarterly or annual basis.

Utilities

Depending on your rental agreement, you may be responsible for utilities such as water rates.

Property management fees

Property managers look after leasing and managing properties on behalf of owners. Should you choose to engage one rather than manage the investment property yourself, you will need to pay property management fees.

Landlord and tenant protection insurance

In addition to the other types of insurance you’ll generally take out to secure your investment, you may want to consider landlord insurance to protect your property from unforeseen expenditures associated with renting it out, such as vandalism.

Advertising fees

You will almost certainly have to pay these if your property requires new tenants, especially if your current tenants vacate unexpectedly, in which case you may face a period without rental income.

Taxes

The government levies land tax on land you own if the total taxable value of the land exceeds the land tax threshold set by your state or territory.

You won’t have to pay land tax on a home you reside in, but you will with an investment property if it exceeds the land tax threshold.

Your income tax responsibilities will be determined by whether your property is positively or negatively geared; that is if you’ve earned more than you spent or you’ve spent more than you earned. We’ll discuss more of this below…so keep on reading.

Now that we’ve covered the areas of expenses and taxes, let’s move on to the next topic.

Profits and Property Taxes

We mentioned earlier that the main goal of an investment property is usually to achieve capital growth and to generate a passive income.

Your passive income or rental income has a corresponding income tax, while capital growth has a corresponding capital gains tax if you sell your property investment.

Let’s discuss both briefly.

Income Tax

The Australian Taxation Office (ATO) considers rental income from renting out a portion or all of your property to be assessable taxable income.

This means that rental income is taxed at your marginal tax rate and must be reported on your tax return.

The marginal tax rates for 2022-23 are shown here, and they indicate how much tax you may have to pay after adding your sources of income including your rental income and factoring in your deductions.

| Resident tax rates 2022–23 | |

| Taxable income | Tax on this income |

| 0 – $18,200 | Nil |

| $18,201 – $45,000 | 19 cents for each $1 over $18,200 |

| $45,001 – $120,000 | $5,092 plus 32.5 cents for each $1 over $45,000 |

| $120,001 – $180,000 | $29,467 plus 37 cents for each $1 over $120,000 |

| $180,001 and over | $51,667 plus 45 cents for each $1 over $180,000 |

Source: ATO Individual income tax rates for 2022-2023

A property is said to be positively geared when its rental income is more than its total expenses.

Negative gearing on the other hand means your total expenses for your investment property is greater than your rental income.

The key benefit of negative gearing is that it allows you to offset net rental losses against other income, such as your salary. This reduces your taxable income and the tax you have to pay.

However, from an investment perspective, a negative gearing strategy may not be a good fit for your situation. A negatively geared investment property will cost you money each year to hold rather than generating a net income for you.

Capital Gains Tax

When you sell your investment property, you either make a capital gain (selling the property for more than you paid for it) or a capital loss (selling for less than you bought it for).

Capital gains tax is a tax levied on investment profits, with the capital gain being added to your taxable income in the same way it is done with rental income.

Therefore, a capital gain has the potential to significantly raise your taxable income.

However, if an investor holds on to a property for more than one year, a capital gains discount may be applied in certain scenarios.

According to the ATO, the capital gains tax discount is now 50%, so if you made $80,000 on the sale of your property, in certain circumstances you would only pay tax on $40,000.

Investment Loan Options

An investment home loan is a form of mortgage used by investors to acquire investment properties.

Investment loans are similar to owner-occupier home loans (the mortgage you get to buy your own home), but their interest rates are often higher. This is because lenders regard investors as relatively riskier borrowers.

While every borrower benefits from acquiring a loan with a cheaper interest rate, an investor’s priorities may differ from those of an owner-occupier. Investors consider investment loan options that could help meet their cash-flow and capital growth objectives.

| Investment Loan Options | Investment Mortgage Repayment Options |

| Fixed Home Loans Variable Home Loans Split Home Loans | Interest-only Principal-and-Interest |

You can get an investment loan with a fixed interest rate, a variable interest rate, or a split loan.

Fixed Home Loans

A fixed home loan is a type of mortgage where the interest rate is fixed (meaning it will not change) for a given length of time, often one to five years, however some lenders may provide longer fixed term durations of up to ten years.

Fixed loans are advantageous if you wish to lock in your repayments at a fixed interest rate, giving you repayment certainty during the first few years of ownership.

Variable Home Loans

A variable home loan is a type of mortgage where the interest rate fluctuates over the loan period. Interest rate variations can occur at any moment at the lender’s discretion, but they most typically occur in response to changes in the RBA’s official cash rate.

Split Home Loans

A split home loan is a loan in which a portion of the rate is set and the remainder is changeable. This isn’t always a 50:50 split; it may be an 80:20 split or a 60:40 split, depending on what you and the lender agree on.

Additionally, investment mortgages have two repayment options:

- Interest-only Repayment

With this repayment arrangement, you only pay off the interest portion of the loan, so your overall instalments are lower than with a principal-and-interest loan.

Because the interest is tax deductible (it is considered an expense), interest-only loans are attractive for investment properties.

Interest-only loans are typically provided for one to five years before reverting to principal-and-interest repayments.

2. Principal-and-Interest Repayment

With this repayment method, you pay off both the borrowed amount (the principal) and the interest.

Principal-and-interest (P&I) repayments help to pay off your debt faster because you are repaying both the principal and the interest.

The principal portion of the repayments are not tax deductible.

Now that we’ve tackled all the expenses associated with a property investment, let’s move on to making money from an investment property.

Expected Cash Flow and Long-Term Appreciation Projections

After researching an attractive location, taking on an investment loan, and calculating expenses as a property investor, we now have to ask the million dollar question:

How do you make money from an investment property?

There are two ways to make money from an investment property:

Through rental income (cash flow) and selling the property (long-term appreciation).

Let’s drill down into the details…

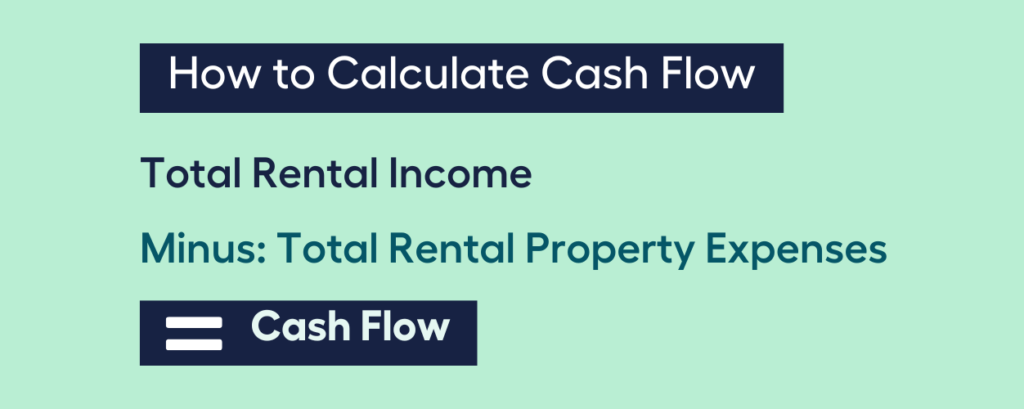

Cash Flow

Investing in real estate requires knowledge of how to calculate rental property cash flow before diving into the rental property market.

After all, cash flow is the lifeblood of any investment. Fortunately, calculating cash flow is easier than you would think.

The difference between the rent received and the expenses paid on an investment property is referred to as real estate cash flow. Calculating the cash flow is simple using this concept:

When you understand how cash flow is calculated, you’ll realise that a positive cash flow indicates a healthy cash flow.

The profitability of a rental property for the period of time you own the property is directly proportional to the amount of positive cash flow it creates.

Long-Term Appreciation Projection

Property values in Australia have increased 382% in the last 30 years, or 5.4% per year on average since July 1992, according to CoreLogic.

So how many years would it take for your investment property to double in value at 5.4% per year?

We can use the Rule of 72, a useful technique to estimate how your investment will grow over time.

If you know the projected rate of return on your investment, the Rule of 72 can tell you how long it will take for your investment to double in value.

Simply divide 72 by the estimated rate of return on your investment (just drop the percent sign).

Note that the rule of 72 is most effective when capital growth rates are between 6% and 10%.

| Estimate Years For a Property’s Value to Double | |

| Rule | 72 |

| Divide by interest rate | 5.4 |

| Value doubles in | 13.33 years |

The rule, of course, isn’t exact science as property values are influenced by many important factors such as inflation, legislation, geography, and buyer sentiments to name a few.

It does, however, give you an indication of how many years it may take a property to double in value based on the historical performance of an area.

Note: historical performance cannot be relied upon as an accurate indicator of future performance.

Available Tax Benefits

Remember the two tax benefits – negative gearing and capital gains tax discount – that we mentioned earlier?

Let’s start off with those two tax benefits and stack on the rest of the available tax benefits for property investors.

Negative Gearing

If the earnings from your rental property do not cover the costs and you are losing money overall, your property is negatively geared. However, negative gearing isn’t all bad; you may be able to utilise that loss to offset other sources of income, thus lowering your taxable income.

Capital Gains Tax Discount

The ATO states that when you sell or dispose of an asset, you can lower your capital gain by 50% through a CGT discount dependent on how you own the property (eg. in your own name versus owning the property in a company) and if both of the following conditions are met:

- you possessed the asset for at least 12 months, and

- you are a tax resident of Australia

Claims for Depreciation

The assets (such as a hot water service) you purchase for your rental property will eventually lose value as they age and succumb to natural wear and tear.

This is known as depreciation, and you can stretch the tax deduction (also known as tax depreciation or capital allowances) throughout the asset’s effective life.

Check out the ATO’s information on the effective life of an asset to see how long you might be able to claim depreciation on assets used at your rental property.

Capital Improvements

You may be eligible to deduct expenses for capital improvements made to your rental property, such as building and renovating. Capital improvement deductions are often spread out over a 25 to 40-year period, depending on:

- when construction began

- when the property was purchased, and

- how the property is used.

Interest Payments and Holding Costs

There are numerous expenses associated with purchasing and owning an investment property, including interest payments, renovations and maintenance, council rates, and property management fees.

The good news is that you may be able to use some of these expenses as tax deductions if your property is rented or available for rent.

Property investors frequently claim mortgage interest on a rental property as a tax deduction. Management charges (such as real estate agent fees), land tax, and maintenance costs are also common tax deductions (like cleaning, gardening, insurance and repairs).

But wait…you can’t claim deductions for these cost and expense items ALL the time, okay?

Take note:

- You can only claim deductions for your property during times when it was rented or really available for rent.

- You can only claim the part of a cost that was used for income generating purposes, and you have to keep records to prove it.

If you need more information or someone to bounce ideas with, talk to My Money Sorted for free!

Many people may be unaware of this…but just like you, 41% of Aussies intend to get financial advice rather than going it alone, according to an Australian Securities and Investments Commission (ASIC) report.

Find the right Financial Adviser for you with the help of My Money Sorted.

When you book a call with My Money Sorted, you’ll:

✓ get a better understanding of your home loan options

✓ have an idea of the experts you can call on to help you reach your goals

✓ be matched with a property expert who can help develop the best investment strategy for your situation

My Money Sorted is your stress-free pathway to getting ahead with your investments.

Curious what happens during a call with My Money Sorted?

Watch this video!

It’s that easy!

Wanting to Invest in Real Estate? Chat to My Money Sorted to Find Out More