If you could choose one of these three perks, which would you pick?

- Boost retirement income

- Save for a home deposit

- Get tax deduction on assessable income and investment gains

It’s a bit of a dilemma if all three were on your wishlist. Fortunately, all three are benefits of salary sacrifice contributions.

In this article we’ll discuss how salary sacrificing into super is a smart way for Australians to increase their retirement savings, save on tax, and improve their retirement outcomes.

Jump straight to…

Salary Sacrifice Explained

Salary sacrifice allows you to use part of your before-tax income for certain benefits of equal value. A salary sacrifice arrangement lowers your taxable income, which means you may pay less tax on your earnings.

There are many types of benefits can be included in a salary sacrifice arrangement; what matters is that the benefits replace the salary you would have otherwise received.

Some of the benefits you can include in a salary sacrifice arrangement are fringe benefits, such as cars, shares, or payment of your expenses for loan repayments and childcare costs. Your employer must pay fringe benefits tax (FBT) on the value of the benefit you get.

Although items that are work-related, such as a tool of trade, computer software, or electronic device, are exempt from FBT.

And superannuation contributions are not only exempt from FBT but also tax deductible for your employer as these are considered employer contributions.

What is Salary Sacrifice in Australia?

Salary sacrifice is also known as whole remuneration packaging or salary packaging.

In a salary sacrifice arrangement, you and your employer agree that you will get less take-home pay in exchange for your employer providing you with benefits of equivalent value. These benefits are deducted from your pre-tax earnings, which lowers your taxable income.

Best of all, salary sacrifice does not affect the superannuation guarantee amount your employer pays.

Any payments that would have been ordinary time earnings (OTE) had they not been salary sacrificed are included in the OTE base.

This means that salary sacrifice cannot be used to lower OTE and cannot be used to calculate super guarantee contributions.

How Does a Salary Sacrifice Arrangement Work?

Salary sacrifice is a mutual agreement between you and your employer.

- Once this arrangement is in place, an agreed-upon amount will be withdrawn from your pre-tax salary to be applied to your benefits over a certain time period.

The agreement can begin when you start a new job or after you’ve been with the same employer for a period of time, however, you can only salary sacrifice a portion of a ‘future entitlement’.

Thus the arrangement cannot include salary and wages, leave entitlements, bonuses, or commissions earned prior to entering the arrangement.

Keep in mind that you will not be able to access the salary amount you sacrifice during the duration of your agreement. If you do not receive a fringe benefit and cash it out, the sum becomes part of your salary and is taxed as standard income.

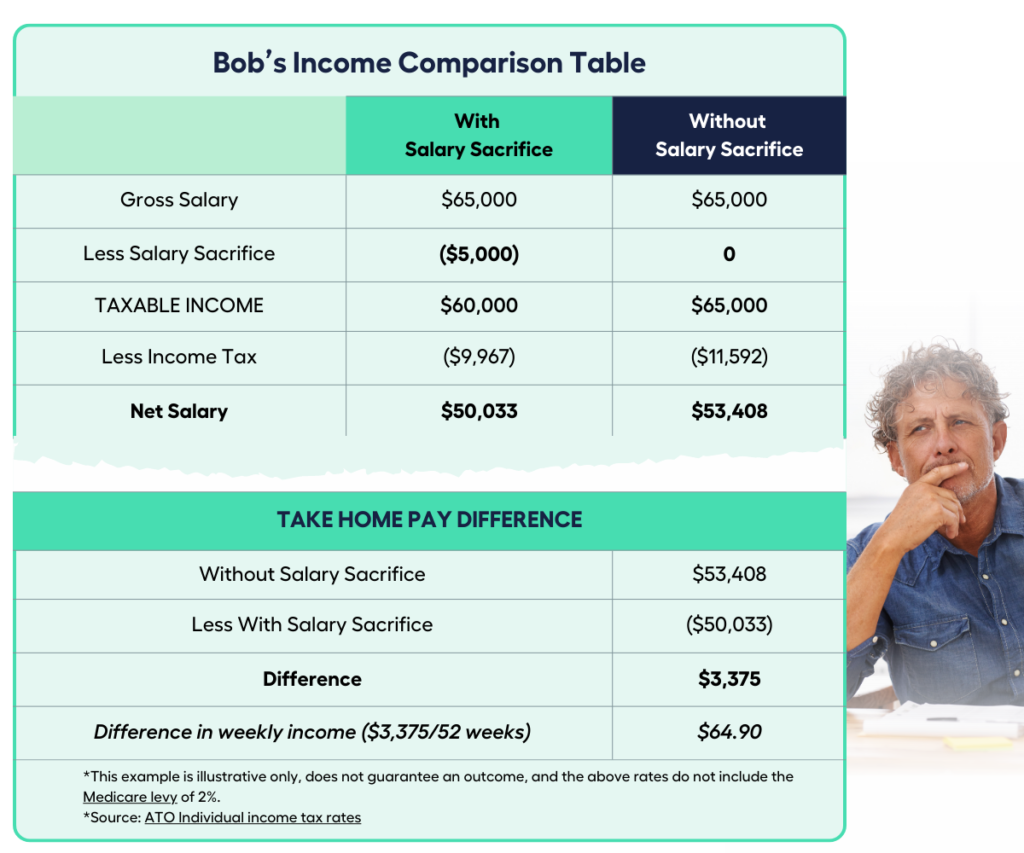

Salary Sacrifice Example

Salary sacrifice could be an effective approach to increase your superannuation contributions and decrease your taxable income at the same time if your annual income is over $45,000 and your tax rate is 32.5% or higher.

Let’s take Bob as an example:

- Bob earns $65,000 a year and decides to make a salary sacrifice of $5,000 a year to his super, and as a result, his taxable income is reduced. His annual take-home pay is $3,375 less while he gets to save $5,000 a year to his super.

*This example is illustrative only, does not guarantee an outcome, and the above rates do not include the Medicare levy of 2%.

*Source: ATO Individual income tax rates

Although the example doesn’t reflect other scenarios such as medicare levy, it gives you a good understanding of how little salary sacrificed super contributions affects Bob’s weekly income.

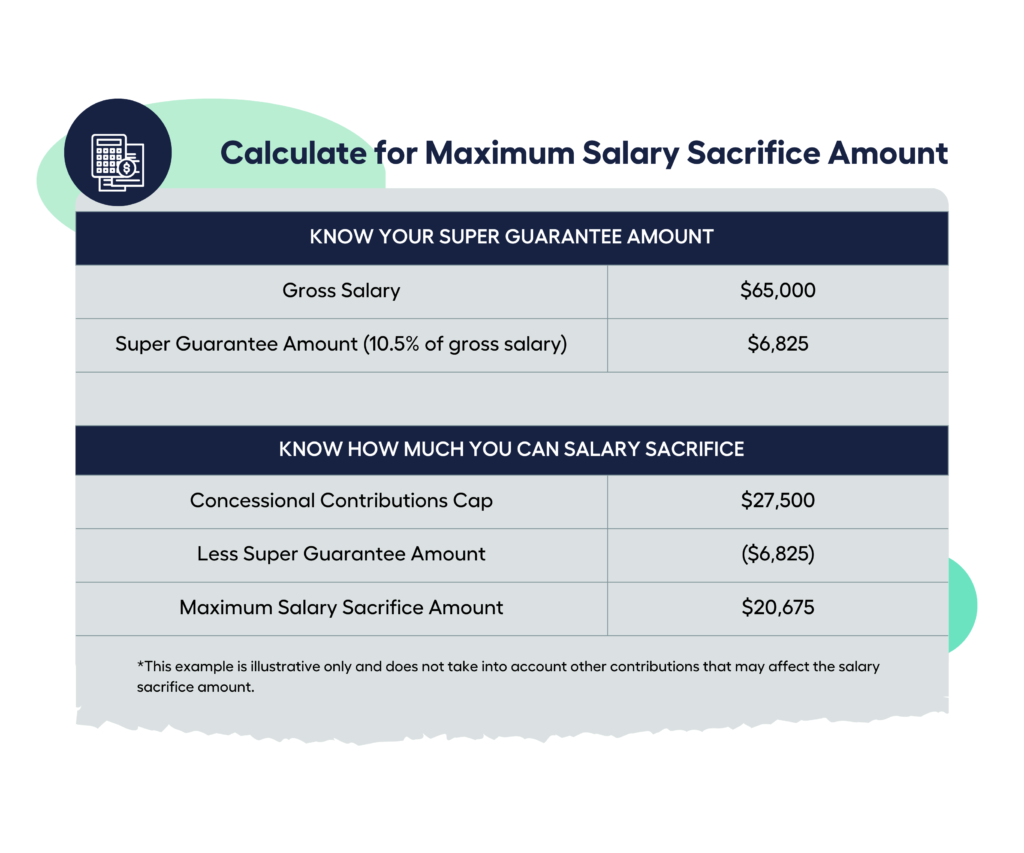

How Much Can I Salary Sacrifice Into Super?

There is no limit on how much employees can salary sacrifice (unless their employment contract or agreement states otherwise). You will, however, pay more tax if your contributions exceed the concessional contributions cap of $27,500 per financial year.

The concessional contributions cap is the combination of your employer and salary sacrificed contributions.

- That means your maximum salary sacrifice amount would be equal to $27,500 less employer contributions or 10.5% of your OTE.

Let’s take Bob again as an example.

- Bob earns $65,000 a year, which means his super guarantee is $6,825 or 10.5% of $65,000. He can make a salary sacrifice of as much as $20,675 a year.

*This example is illustrative only and does not take into account other contributions that may affect the salary sacrifice amount.

- Note that for the fiscal year 1 July 2022 – 30 June 2023, your employer’s minimum super guarantee contribution is 10.5% of your ordinary time earnings.

And for the fiscal year 1 July 2023 – 30 June 2024, your employer’s minimum super guarantee contribution is 11% of your ordinary time earnings.

Salary Sacrifice Benefits

If you salary sacrifice now, you’ll notice that the sacrifice is only for the short term but its benefits will be with you for the long haul. This includes having more money for retirement, saving on taxes, and potentially helping you pay for a home deposit sooner.

More Super Savings for Retirement

If you can afford to lower your take-home pay in the short term in order to contribute more to your super, you’ll have more money for retirement.

- Employers are required to contribute to your super an amount at least equal to 10.5% of your OTE, but if you rely only on it, you may not accumulate enough to cover your retirement lifestyle.

Contributing more to your super savings account now may increase your nest egg in the long run. Not only will your account balance increase, but you will also profit from compound interest (interest on top of interest) while the money is in your superannuation fund.

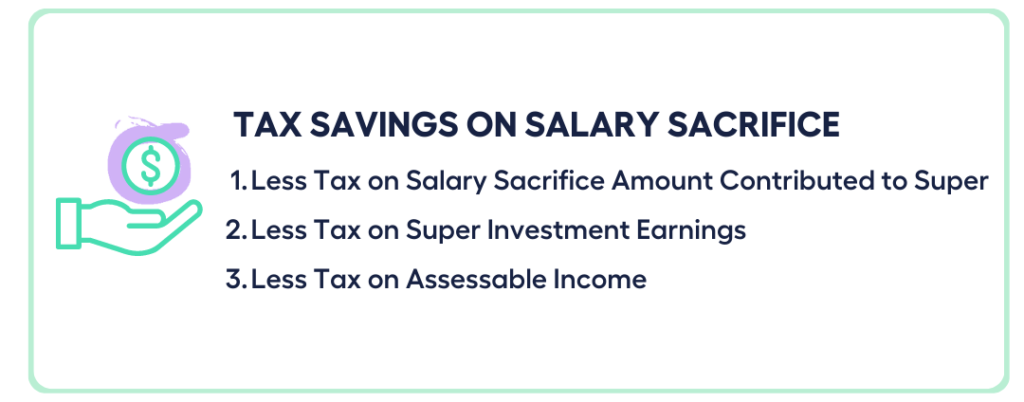

Tax Savings

In general, you can take advantage of three tax benefits when you salary package to your super.

You may pay less tax on the salary sacrifice component of your pay that goes into your super account, less tax on investment earnings while they are in your account, and potentially less tax on your total assessable income.

1

Less Tax on Salary Sacrifice Amount Contributed to Super

The amount you sacrifice is considered an employer contribution and is deducted from your pre-tax income. Employer contributions are taxed at a concessional (discounted) rate of 15%, which is likely less than the marginal tax rate if you earn more than $45,000 a year.

2

Less Tax on Super Investment Earnings

While your salary sacrificed contribution is invested in your super fund, the tax on the income from your investments is 15%, which is likely to be lower than if it was invested elsewhere, if not less complicated.

3

Less Tax on Assessable Income

Your assessable income will be reduced as a result of receiving less take-home pay (with more of your income going into super), which normally implies you will pay less income tax.

Access the First Home Super Saver Scheme

You can take advantage of the First Home Super Saver (FHSS) Scheme if you’re:

- at least 18 years old,

- buying or building your first home in Australia,

- and planning to live in it.

- As a first home buyer, you may make before or after-tax contributions voluntarily under the FHSS scheme.

You are allowed to contribute up to $15,000 annually and $50,000 overall to your superannuation. Just take care not to go over the $27,500 annual concessional contributions cap.

- You can then withdraw as much as $50,000 in voluntary super contributions to put towards your first home.

One of the FHSS key benefits is that it provides a tax-effective option to save for a deposit; when you put money in a super account instead of a savings account, you pay less tax, thus helping you save for a home deposit quicker.

If you’re considering salary sacrifice contributions for your superannuation, but feel like you’re lost in a maze of possibilities and super jargon, consulting a finance expert may be worthwhile to get you started on the right track.

Many people may be unaware of this…but just like you, 41% of Aussies intend to get financial advice rather than going it alone, according to an Australian Securities and Investments Commission (ASIC) report.

Learn how to choose the best super fund for your goals and situation by consulting with qualified finance experts like a financial adviser.

Discover How to Get Your Super Sorted Sooner – Book a FREE 15min Call or Send Us Your Questions