If you’re someone who loves online shopping and wants to manage your finances better, then this is an article you don’t want to miss!

We’re going to talk about one of the hottest topics in the finance world – buy now pay later (BNPL) apps. These apps are popping up left, right and centre, promising to make our shopping experiences a breeze.

But, have you ever stopped to think about how using these apps could affect your credit score?

In this article, we’ll dive deep into the world of BNPL and explore whether these apps are a friend or foe when it comes to your creditworthiness.

Jump straight to…

What are Buy Now Pay Later Apps and What Do They Do?

First things first, let’s break down what BNPL apps are and what they do.

These apps allow you to buy a product or service upfront but pay for it in instalments over time. Instead of paying the full amount at the time of purchase, you can split the cost into smaller payments, making it easier to manage your budget.

This can make your dream purchase within reach, as long as you don’t go overboard with spending. They offer interest-free deals but be careful because additional fees and charges can stack up fast.

Popular BNPL Apps

BNPL apps are everywhere these days and seem to promise the world.

- But, are they too good to be true?

Let’s take a closer look at some of the most popular buy now pay later apps on the market.

1. Afterpay

Afterpay lets you split the cost of your purchase into four equal payments over six weeks interest-free. Spending caps with Afterpay begin at roughly $600 and only rise progressively with on-time payments.

There’s no interest to pay, but if you’re late on a payment, you’ll be slapped with a fee, and you won’t be able to use Afterpay until you pay off your account. The late payment fee is capped at $68 or 25% of the purchase price (whichever is lower). If your order is under $40, the maximum late fee is $10.

2. Brighte

Brighte provides BNPL options for homeowners who want to improve their homes and make them more energy-efficient, but don’t want to pay for everything upfront.

Brighte offers a way to make home and energy purchases between $1,000 to $30,000 and pay it back in 6 to 60 months. They charge a weekly account keeping fee of $2.70 and a $299 establishment fee. If you miss a payment, they charge a late payment fee of $4.99 capped at $49.90 per calendar year (equal to 10 missed repayments).

You could get a loan with zero-interest from Brighte if you want to install solar panels or a new air conditioning unit but don’t have the money upfront. However, you can only choose vendors approved by Brighte.

3. humm

humm offers customers the option to buy things online or in-store for up to $30,000 and choose from their repayment terms ranging from 2 months to 60 months, depending on how much you’ve borrowed. You can make repayments weekly, fortnightly, or monthly, and you won’t be charged any penalties for paying more than required.

There are no fees for small purchases of up to $2,000 paid back within five fortnights (2.5 months), but for longer periods and large purchases, there may be monthly fees ($8), transaction fees ($2), and establishment fees ($30-$110), and missed repayment fees ($6) if you don’t pay on time.

4. Klarna

Klarna allows you to make purchases now and pay for them later in four interest-free instalments, paid fortnightly.

You can use Klarna to shop at over 200,000 online stores, even if they haven’t partnered with Klarna yet, using the Ghost Card (a virtual Visa card). You can also get a physical Klarna Card to enable you to shop anywhere Visa is accepted. Take note that Klarna cards charge a $4.99 monthly fee whether you shop online or in-store.

If you are unable to meet the repayment deadline, you have two to seven business days to catch up before the fee kicks in using Klarna’s “slack period” feature.

If you forget to pay or don’t update your payment details during the “slack period,” you’ll be charged a late payment fee. The late fee is either $3 if your order was under $100 or $7 if it was over $100.

5. Laybuy

Laybuy is a service that lets you buy things and pay for them interest-free in six weekly payments, without any hidden fees or sign-up costs. You need to pay just 1/6 of the price today and then pay the remaining balance over the next five weeks.

Plus, with the Laybuy Boost feature, you can spend more than your limit by paying the amount in excess of your available limit upfront and the rest of the balance in weekly payments.

Repayments are automatically deducted from your credit or debit card, and how much you can borrow depends on your credit limit. There’s no interest to pay, but if you’re late on a payment, you’ll be hit with a $10 late fee.

6. PayPal Pay in 4

PayPal Pay in 4 is a way to buy now and pay later without having to pay interest. You’ll need to make 4 equal payments, with the first one being right away, and then every 2 weeks after that.

You can split the cost of things you buy online into 4 equal instalments, as long as it’s under $2,000 and at least $30. You can also use it with any currency, not just Australian dollars.

Remember that you’ll have 6 weeks to pay everything off. Your payments will come out of your PayPal account automatically using the payment method you choose.

To use this service, you need to have a PayPal account and be a customer in good standing.

It’s free to sign up for PayPal in 4, and you won’t be charged any fees or extra money if you miss a payment deadline but it might show up on your credit report.

7. Zip Money and Zip Pay

Zip Money is a buy now pay later app that lets you borrow up to $50,000 for larger purchases. You’ll need to pay interest on your purchases, but you can choose how long you want to repay your loan. Zip Pay, on the other hand, is aimed at smaller purchases and offers more flexible repayment terms.

Zip Pay is a way for you to pay for everyday things without having to pay anything upfront. There’s no fee to start a Zip Pay account, and you won’t be charged any interest on your purchases.

When it comes to repayments, you can choose to pay back what you owe weekly, monthly or fortnightly, with the minimum repayment being $10 per week.

To be able to start using the app, Zip Pay will confirm your credit limit after you’re approved, which can be between $350 and $1,000. You will then be charged a monthly account fee of $7.95, but if you pay off everything you owe before the due date, this fee is waived.

Zip Pay claims that they don’t have hidden fees, and you’ll never be charged any interest on what you owe as long as you pay everything back on time.

Zip Money is a way to get a larger credit limit, with up to $5,000 (or even $50,0000 for selected merchants) available to you. There may be a one-off establishment fee of up to $99, depending on your approved credit limit. However, every transaction made with Zip Money comes with a guaranteed 3-month interest-free period.

There is a monthly account fee of $7.95, which is waived if your balance owing is $0 at the end of the month.

How Buy Now Pay Later Works

Buy now, pay later allows you to make a purchase and pay for it over a longer period of time instead of all at once. It’s like borrowing money from a third-party provider that’s available in many stores.

- Let’s say you want to buy a new outfit for an upcoming event. Instead of paying $200 upfront, you can use a BNPL app to split the payment into four equal instalments of $50.

You’ll pay the first instalment at the time of purchase, and then the remaining three payments will be automatically deducted from your account over the following weeks, depending on the repayment terms of the BNPL app you are using.

What is the Application Process?

When it comes to the application process for BNPL apps, it’s typically pretty straightforward.

- You can sign up online or in-store to get your application approved.

You’ll need to provide some basic information such as your name, address, and date of birth. You may also need to provide details about your employment and income to ensure you have the means to make the payments.

Can Buy Now Pay Later Affect My Credit Score?

- Yes, it can. But let’s break it down in simple terms.

Why Does Buy Now Pay Later Affect My Credit Score?

When applicants sign up for a BNPL service, the company will typically check their applicants’ credit scores. This means that they will check your credit history to see whether you are a responsible borrower. You’re more likely to be accepted for the service if you have an excellent credit score.

Now, this is where things might become challenging. Your credit score might rise if you use BNPL wisely and pay your bills on time. Your credit score might be negatively impacted if you skip payments or are late with them.

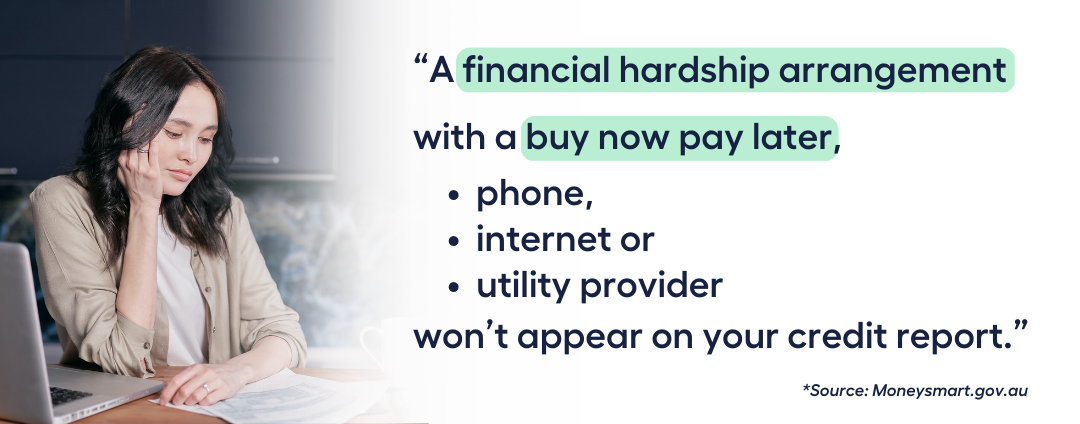

An exception to this scenario is when you have a financial hardship arrangement with your BNPL provider. According to Moneysmart.gov.au: “A financial hardship arrangement with a buy now pay later, phone, internet or utility provider won’t appear on your credit report.”

How Are Buy Now Pay Later Apps Regulated?

ABC News has reported that despite the BNPL companies acting very much like credit providers, it is currently unregulated. However, the Australian government plans to introduce regulations for this market in 2023.

- The government is planning to introduce regulations that will require BNPL providers to be licenced by the Australian Securities and Investments Commission (ASIC).

Under these regulations, BNPL providers will be required to meet certain standards and follow certain rules to ensure that their services are transparent and fair. For example, they will need to make sure that customers are fully informed about the fees and charges associated with their services, and they will need to have systems in place to help customers who are struggling to make their payments.

The Minister for Financial Services, Stephen Jones, wants to make sure that BNPL companies are doing the right checks and not marketing credit to people who might have trouble paying it back. This is to make sure that people are protected and don’t end up in debt that they can’t handle.

Alternatives to Using Buy Now Pay Later Apps

There are a few options to consider if you’re looking for alternatives to buy now, pay later apps.

Using a credit card with 0% p.a. introductory offer is one alternative, which can also offer the ability to make purchases and pay them off over time. However, it’s important to be aware of the fees and interest rates that take effect once the introductory offer expires.

If you’re concerned about overspending, it’s also important to know that you are not required to accept the maximum credit limit offered by your bank or credit provider. It would be wise to reflect on your spending habits and determine how much you can easily repay without causing financial strain by setting a credit limit that you can comfortably afford.

Another option is to save up for the purchase instead of using credit. This may take longer, but it can help you avoid the risk of accumulating debt and paying interest.

To further save costs, you can also hunt for sales or discounts on the item you wish to purchase.

If you need a small amount of money quickly, you may be able to borrow from friends or family. This may be an option if you are unable to obtain a loan from a bank or a credit institution.

The final option is layby, which lets you pay for an item gradually and receive it after the balance is paid in full. If you have a limited budget and don’t want to incur debt, this can be considered as a viable alternative for you.

Remember, it’s important to weigh the pros and cons of each option and choose the one that’s right for your financial situation.

Want to Improve Your Credit Score & Get Your Money Sorted? Book a FREE 15min Call or Send Us Your Questions!

I want to see all my options with the help of a Finance Expert

Call Our Team TodaySOURCES:

Disclosure: Links on this page are affiliate links, which means that if you click on the link or make a purchase using the link, the owner of this website may earn a commission. When you make a purchase, the price you pay will be the same whether you use the affiliate link or go directly to the vendor’s website using a non-affiliate link. By using the affiliate links, you are helping support this website, and your support is genuinely appreciated. Please note that any product or service recommendations on this website are based on personal experience or research.