When planning a holiday, would you book a package tour or make your travel plans and book reservations yourself?

Some opt for the convenience a package tour provides — pay the advertised price and let someone else take care of reservations, itinerary, and schedule.

Others prefer to do things on their own and have the chance to be spontaneous — choosing the places they want to visit, handling the bookings, travel route, and schedule.

In each endeavour we get into, we mostly have two preferences to choose from:

Doing it ourselves or hire a professional.

Just like choosing travel arrangements, when looking for the best options for superannuation, we’re also provided with preferences to choose from:

SMSFs vs Industry Funds.

- In a way, self-managed superannuation funds (SMSF) are similar to DIY travel. You get to manage the way your funds are invested and you can be spontaneous with decisions if the need arises.

- On the other hand, industry funds are like package tours. They relieve you of most of the stress involved in investing your money because an industry fund manager takes care of it.

But it’s not that simple.

Choosing the best option for superannuation is more than just weighing options between control and convenience.

Whether investing your money in an SMSF or industry fund, you still need a financial plan that considers your personal and financial circumstances, your retirement plans, your savings, your lifestyle, and many other aspects related to your personal life and finances.

Either way, you’ll probably need sound financial advice to make the most of your investment.

For now, let’s have a look at what makes SMSFs and industry funds unique investment options.

Jump straight to…

What is a Self-Managed Super Fund?

A self-managed super fund, or SMSF, is a private superannuation account into which you or your employer contributes your superannuation and which you directly administer. The investments and insurance options are your choice.

While being in charge of your own super can be alluring, it requires a lot of work and carries risks.

You are the fund’s trustee as a member, or you can hire a corporate trustee. In either scenario, you are in charge of your own SMSF.

There cannot be more than six trustees in your SMSF. Two or more are common in self-managed super funds.

Create your self managed super fund only if you’re fully dedicated and aware of the risks.

What are the Pros and Cons of SMSF?

As of June 2021, there were almost 598,000 self-managed superannuation funds with a little over 1 million members. SMSFs held $822 billion (25%) of the $3.3 trillion in super assets under management.

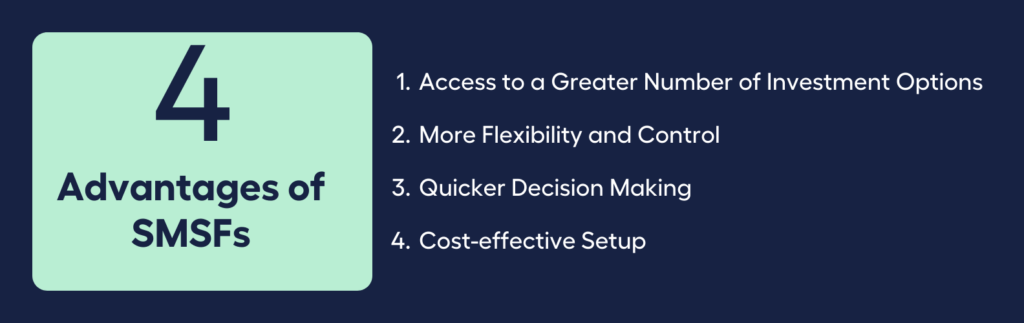

These Aussies clearly saw the advantages of self-managed super funds, such as access to a greater number of investment options, more flexibility and control, quicker decision making, and a cost-effective setup.

Access to a Greater Number of Investment Options

The wide range of investment options available through self-managed super funds is one of the most common reasons people choose them.

A retail or industry super fund may not allow members to access assets such as art and collectibles, stamps and coins, property, or even physical gold. SMSFs, on the other hand, allow for greater access to such investment options.

Among the many different types of assets you might choose to invest in are stocks, managed funds, fixed-interest investments, and residential and commercial property, just to name a few.

More Flexibility and Control

The fact that fund members have control over the portfolio’s management may be an SMSF’s best benefit.

Members who serve as trustees have the freedom to modify the fund agreement to better reflect their preferences. Thus, they have the option of selecting the fund’s investment strategy. When considering whether to seize opportunities that would otherwise seem risky for regular super funds, this can be quite important.

In the event of high market unpredictability, trustees can modify their portfolios to avoid losses.

Quicker Decision Making

Quick decisions can have a significant impact on a self-managed super fund’s performance.

Trustees in SMSFs have unique access to information about the operation of the SMSF and the current performance of the investments.

In contrast, the performance of investments in retail or industry super funds is aggregated and may not be disclosed for several months.

As a result, quicker availability of investment performance data in an SMSF enables timely decision-making, minimising potential fund losses.

Cost-Effective Setup

Self-managed super funds can be a more affordable investment option depending on the fees involved in setting up and managing the fund.

Lower ongoing costs are an advantage of managing your own SMSF. The SMSF’s expected operating expense ratio is 0.5% and the operating cost ratio decreases when the fund size increases according to the ATO.

Managing your own super fund may sound attractive but it isn’t for everybody. Individuals who have a low-risk tolerance may be better off entrusting their money to retail or industry super funds or funds regulated by the Australian Prudential Regulation Authority (APRA).

And this brings us to the disadvantages you need to consider before you set up an SMSF of your own. These include being responsible for decisions, the need to research and be up to date, the inability to access government compensation schemes, and minimal access to dispute resolution bodies.

Higher Responsibility for Decisions

The trustee is placed with a much higher level of responsibility as an unavoidable natural consequence of managing an SMSF.

In contrast to retail or industrial super funds, losses on SMSFs cannot be recouped through any regulatory authority.

In addition, breaking the laws and guidelines for handling a super fund carries serious repercussions. Tax penalties may be applicable in addition to significant fines and/or legal action.

The Need for Continuous Research

The process of finding appropriate investment options and monitoring the performance of your investments is time-consuming.

Taking the plunge and managing your SMSF without considerable preparation and knowledge might not be a good idea since a high level of competence is required for this important task.

It involves comprehension of how the financial markets operate, expertise in documenting transactions and investments, and an understanding of how diversity may help balance a portfolio.

No Access to Government Compensation Schemes

Individuals with industrial or retail super funds may be eligible for compensation if their funds suffer losses.

However, with SMSFs, members (who are also trustees) are solely responsible for the management of their super funds.

In the event that money is lost for numerous causes, including some that are beyond the trustees’ control, SMSFs are typically unable to access government compensation programmes.

Minimal Access to Dispute Resolution Bodies

SMSFs have limited access to dispute resolution bodies, putting the fund at risk if the directors/trustees are unable to obtain competent legal aid.

Using traditional courts to resolve disputes results in higher costs for an SMSF.

Why an SMSF May Not Be Right For You?

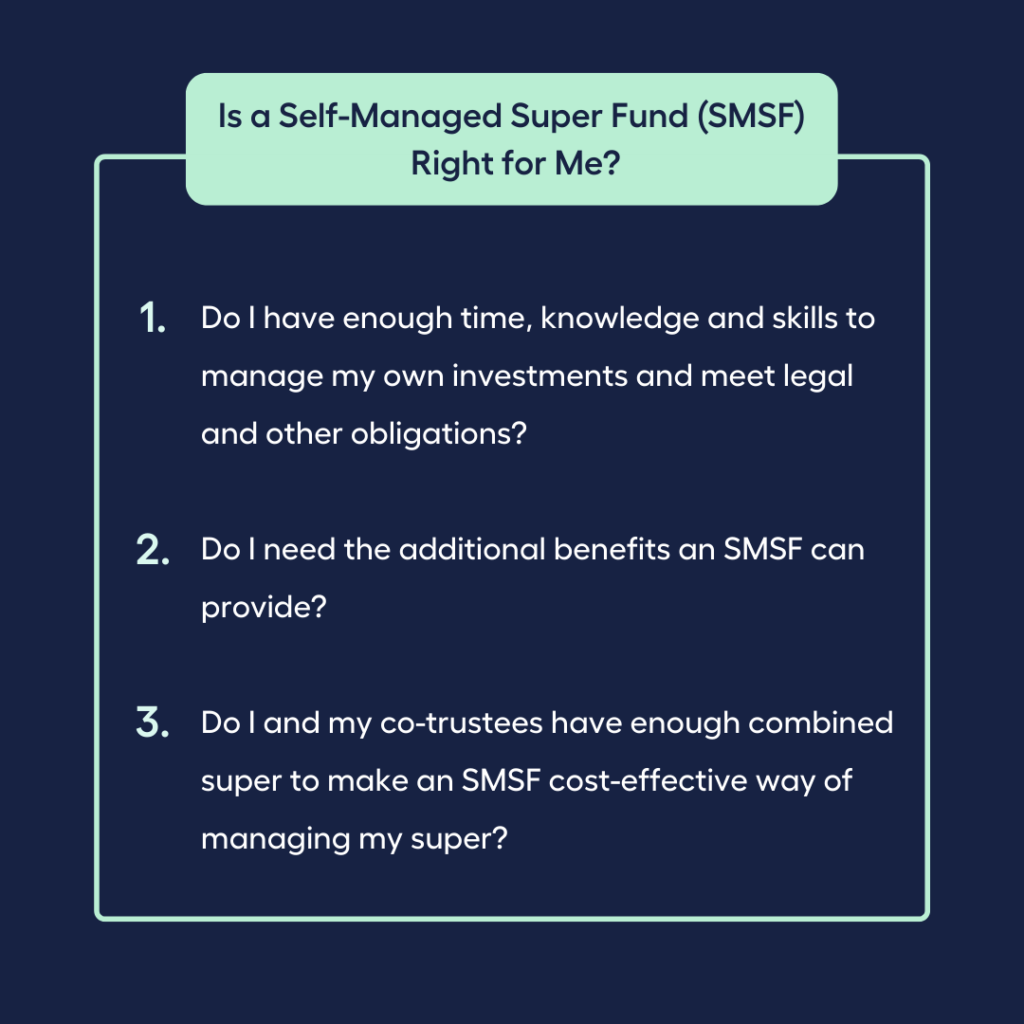

Before you set up an SMSF, it’s important to consider whether running your own super fund is right for you.

Questions to ask yourself:

- Do I have enough time, knowledge, and skills to manage my own investments and meet legal and other obligations?

- Do I need the additional benefits an SMSF can provide?

- Do I and my co-trustees have enough combined super to make an SMSF a cost-effective way of managing my super?

If you answered NO to any of these questions, you may want to consider other super options where you can outsource the responsibility for running the superannuation fund to experts who act in their client’s best interest.

You may consider seeking professional advice or guidance when deciding on the best superannuation solution for you. You may also wish to seek advice from a registered tax agent to determine the tax implications that apply to you.

Where can you find the right professional advice? Get started by booking a complimentary call with our team!

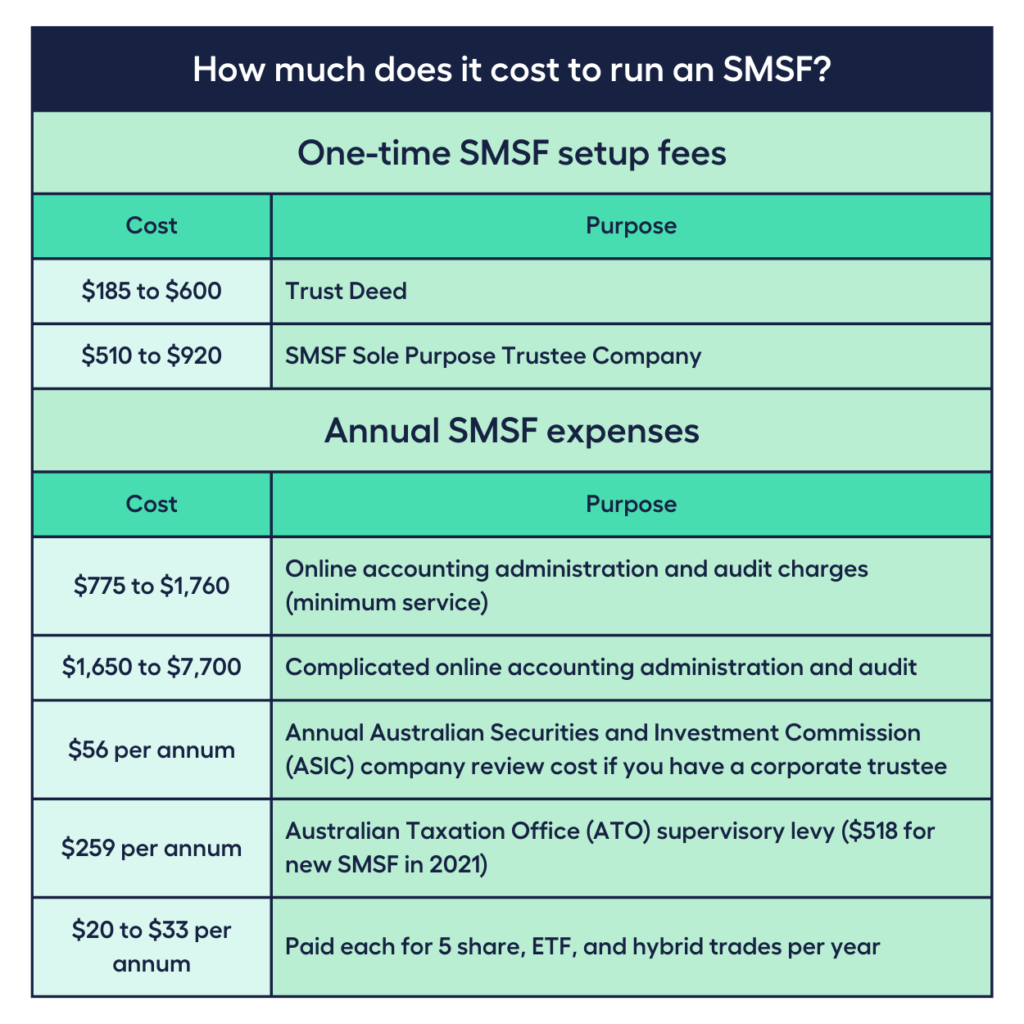

How Much Does it Cost to Run an SMSF?

A self-managed superannuation fund is not, as its name suggests, an entirely self-managed financial investment vehicle.

SMSFs must, at the absolute least, have an administrator and an auditor to help with year-end financials, tax returns, minutes, compliance, and documentation. Additionally, you might want to hire a strategic planner and an investment adviser.

According to the 2020 Rice Warner report, which was commissioned by the SMSF Association, the following are the approximate SMSF establishment and management fees to take into account if you want to handle all of the investments yourself:

One-Time SMSF Setup Fees

- $185 to $600 for a trust deed

- $510 to $920 for SMSF Sole Purpose Trustee Company

Annual SMSF Expenses

- $775 to $1,760 for online accounting administration and audit charges (minimum service)

- $1,650 to $7,700 for complicated online accounting administration and audit

- $56 for the annual Australian Securities and Investment Commission company review cost if you have a corporate trustee

- $259 Australian Taxation Office supervisory levy ($518 for new SMSFs in 2021)

- $20 to $33 each for five shares, ETF, and hybrid trades per year

Whether an SMSF is a cost-effective way of investing and managing your super is a crucial consideration to take into account. It is quite unlikely to be in your best interests if it is not cost-effective.

According to the Productivity Commission’s superannuation analysis of efficiency and competitiveness, SMSFs with balances under $500,000 often have poorer returns after costs and taxes compared to APRA-regulated funds.

However, there are situations wherein your best interests may be served by an SMSF with a starting balance under $500,000.

- One is when the trustee is willing to handle a large portion of the SMSF’s administration and investment management to make it more affordable.

- Another is when, within a few months after the SMSF is established, a sizable asset (such as a company, a property, or an inheritance) or money from another superannuation account will be moved into the fund.

According to the Rice Warner report, someone with an investment balance of $200,000 might still be able to make the running and management of an SMSF cost-effective if they take on a lot of the work.

What is an Industry Fund?

Industry superannuation funds are the largest fund type in terms of assets under management, accounting for $927 billion, or 28.3%, of total superannuation assets as of June 30, 2021.

Industry superannuation funds, also known as profit-for-member funds, are run to benefit members. They’re not owned by a major bank or financial institution.

An industry fund is often a low to medium cost accumulation fund and its proceeds are reinvested in the fund, which has the potential to deliver stronger investment returns to the investor in the long term.

Industry fund members typically operate in a specific field or industry. Many industry super funds were once only open to employees of a particular sector, like the construction, hospitality or retail industries. Today, the majority of sector super funds allow all Australians to join.

Your employer might provide the associated industry super fund as the standard choice for employees if you work in a particular industry. For instance, if you work in the construction industry, your employer’s fund choice will probably be one that caters to construction and building such as CBUS.

However, you are typically not obligated to join the super fund that your employer or your industry has selected, meaning you may be free to join any super fund you like.

What are the Pros and Cons of an Industry Fund?

Industry super funds are a popular choice for many Aussies for a variety of reasons. Some of the advantages of industry super funds over other super fund options are low fees and costs, they support and understand the industries they are associated with, they are run to benefit members, and members don’t bear the responsibility of managing the fund.

1. Low Fees and Costs

Industry funds can generally charge lower fees because they are run for members rather than shareholders.

2. Not-for-Profit Nature

All profits are reinvested into the fund for the benefit of the members, which is why they’re also called profit-for-member funds.

3. Industry Associations and Members Run the Show

Industry funds are typically open to everyone, but there’s an added advantage of investing your money in a fund that is more attuned to your needs.

They can provide members with specialised insurance coverage that is not available in other funds. For example, if you’re a member of a construction fund, your industry fund insurance will typically account for the dangerous nature of construction work.

4. Members Don’t Bear The Responsibility Of Managing The Fund

Members can sleep well at night knowing that the compliance risk is taken on by the professional licensed trustee for industry funds.

As for disadvantages, if you’re looking for a long-term investment and using your superannuation as a retirement fund, then there’s one major disadvantage to consider:

There is less individual freedom in selecting specific investments for yourself.

Why an Industry Fund May Not Be Right For You?

An industry fund may not be right for you if you’re an active investor who is willing to take on risks and manage them in exchange for higher returns.

Questions to ask yourself:

- Do I like to check my fund’s performance on a regular basis?

- Do I prefer to manage investments myself?

- Do I have enough time, knowledge and skills to manage my own investments and meet my legal and other obligations?

If you answered YES to all of these questions, you may want to consider other super options where you can actively take on the responsibility of running the superannuation fund.

Get expert guidance on industry super funds from an experienced financial advisor by booking a complimentary call with our team.

How Much Does it Cost to Run an Industry Fund?

As an individual member, you do not have a hand in managing an industry fund like you do when you have an SMSF.

Industry funds are run like retail funds or funds owned by financial institutions. Both types of funds employ fund managers to invest their funds.

Many of Australia’s largest super funds are either industry super funds or retail super funds. Many similarities exist between industry and retail super funds.

Industry Super Funds and Retail Super Funds Similarities:

✓ Provide options for Australian workers to save for retirement.

✓ Provide members with a variety of investment options and insurance coverage to their members.

However, there are a few distinctions to be made between retail and industry funds, boiling down to a primary distinction that influences their fees and investment returns:

Their ownership structure.

Profits

| Fund Type | How Profits are Distributed |

| Retail Funds Ownership: publicly traded corporations | Distributed to shareholders, investors, executives, and board members |

| Industry Super FundsOwnership: non-profit organisations owned by members | Reinvested in the industry super fund for members’ benefit |

Due to the fact that retail funds are frequently owned by firms that are publicly traded on a stock exchange, the super fund distributes some of its income to shareholders, investors, executives, and board members who work for the financial institution.

Industry super funds are non-profit organisations run to benefit its members. As they are not publicly traded corporations, they also have no shareholders to pay. Profits are reinvested in the industry super fund for the members’ benefit.

Investments

There’s an intriguing area of distinction between industry super funds and retail funds:

Industry super funds tend to have large holdings in assets that are not publicly traded. Roads, bridges, airports, and other forms of public transportation are mostly included in this.

According to some analysts, over the long term, these investments helped industry super funds beat other APRA-regulated funds on average. Industry funds having higher returns is an observation backed by a report by the Productivity Commission.

Can I have an SMSF and an industry fund?

If you find both SMSF and industry funds appealing, you can have both.

There are no laws that prevent people from being members of both a self-managed super fund (SMSF) and an industry fund.

Although having multiple super accounts may result in you incurring unnecessary fees and charges, which has the potential to reduce your overall retirement income.

If you wish to have multiple accounts, make sure to keep track of and manage your super through the ATO’s online services on the myGov website.

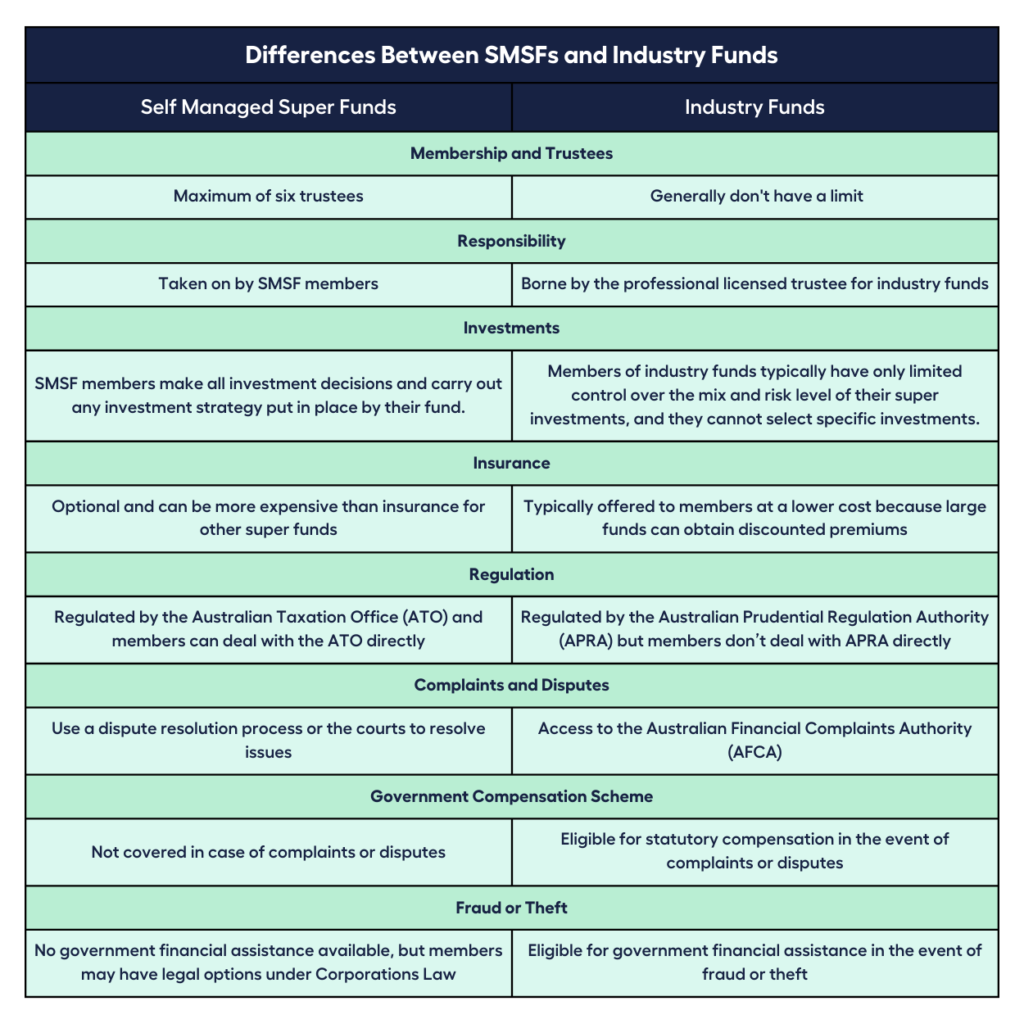

SMSF vs Industry Funds – Which is the Better Option for Superannuation?

SMSFs and industry funds have one thing in common:

Their purpose is to provide retirement benefits to their members.

But they do differ a lot when it comes to membership and trustees, responsibility, investments, insurance, regulation, complaints and disputes, fraudulent conduct and theft.

1. Membership and Trustees

SMSFs can have up to six members. All members are either individual trustees or directors of the fund’s corporate trustee. This means that all members are involved in the SMSFs management.

While there is no limit to the number of members in an industry fund. Professional, licenced trustees are in charge of the fund’s management.

2. Responsibility

SMSF trustees are expected to understand tax and super laws and to ensure that their fund complies with those laws. Compliance risk is borne by SMSF trustees or corporate trustee directors, who can be personally fined if their fund violates the law.

Whereas, the professionally licensed trustee bears the compliance risk for industry funds.

3. Investments

SMSF trustees create and execute the fund’s investment strategy, as well as make all investment decisions.

Most industry funds give you some control over the mix and risk level of your super investments, but you can’t usually choose the specific assets in which your super will be invested.

4. Insurance

SMSF trustees must decide whether or not to buy insurance for their members. Insurance premiums may be higher than those charged by other super funds.

On the other hand, many industry funds provide members with insurance coverage. Member insurance is typically less expensive because large funds can obtain discounted premiums.

5. Regulation

SMSFs are regulated by the ATO. Trustees are required to engage with the ATO to manage their funds.

Industry funds are regulated by the Australian Prudential Regulation Authority (APRA). Generally, members don’t have to engage with APRA.

6. Complaints and Disputes

The ATO is not involved in resolving member disputes. Disagreements can be settled using alternative dispute resolution techniques or in court, at the expense of the members. There is no government compensation plan in place.

Members can lodge complaints with the Australian Financial Complaints Authority (AFCA) and may be entitled to statutory compensation.

7. Government Compensation Scheme

SMSFs are not eligible for government financial assistance.

In the event of fraud or theft, industry fund members may be eligible for government financial assistance.

8. Fraud or Theft

SMSF members may have legal recourse under Corporations Law, but there is no guarantee that they will receive compensation.

Historically, industry funds perform better than other APRA-regulated funds while SMSFs are often unable to match the performance of APRA-regulated funds.

But before deciding which fund type is better, do note that past performance is no guarantee of future results. Your investment decision still boils down to your financial situation. And it’s best to have a financial expert to guide you.

Simplify your super fund options with the help of an experienced Financial Adviser by booking a complimentary call with our team today!

Find the right Financial Adviser for you with the help of our MMS Team.

When you book a call with the My Money Sorted team, you will:

✓ get a better understanding of your investment options

✓ have an idea of the experts you can call on to help you reach your goals

✓ be matched with the right financial adviser who can help simplify your retirement options

My Money Sorted is your stress-free pathway to getting ahead with your money.

Here’s what your journey will look like:

Step 1: Start off with a quick retirement investment alternatives session with an MMS team member

Step 2: Get matched with a licensed Finance Adviser that’s right for your money situation

Step 3: Take the first step towards your money goals with a clear and sound roadmap prepared by an experienced Financial Adviser.

It’s that easy!

Need advice to secure your financial future? Contact My Money Sorted Today to find the right advice!