Have you ever set a goal and failed to achieve it or missed the target?

Even if you’ve been working hard to reach your financial goals, simple mistakes could jeopardise your efforts or make you less likely to set even higher goals.

In this article, we’ll help you avoid those costly mistakes by showing you how to set money goals and achieve them.

Jump straight to…

What are Money Goals?

A money goal is a desired outcome you envision, plan, and commit to achieve in relation to managing your finances.

It may entail getting a savings account, spending less money, earning more money, or investing to achieve an ideal future.

- A list of financial goals is essential for constructing a budget. When you have a clear vision of what you’re striving for, working towards your financial goal is easy.

That means your financial goal should be measurable, specific, and time-bound.

3 Types of Financial Goals

When planning for financial success, include a combination of the three types of financial goals in your strategy.

Here are the three types of goals we’ll discuss today:

- Short-term Financial Goals

- Medium-term Financial Goals

- Long-term Financial Goals

Let’s go over each one individually to clarify things.

Short-term Financial Goals

A short-term financial goal is something you want to achieve as quickly as possible.

These money goals aresmall financial goals that can be accomplished within a year. This might include saving for a family getaway.

3 Reasons Why Short-term Financial Goals are Essential

1. They serve as pillars for bigger goals. To begin with, achieving short-term financial goals lays the groundwork for long-term success.

Money goals for those in their 20s, for example, can focus on the short term to provide the foundation for long-term financial prosperity.

2. They give motivation from “quick-wins”. Achieving short-term financial goals also provides motivation to keep moving forward.

3. Regular review of short-term goals keeps you on-track. Checking your short-term objectives frequently helps you consider your priorities and daily spending habits that can lead to achieving your money goals.

At the end of the day, it’s all about living intentionally, investing in what you value, and living in the present moment.

After all, now is all we have, and tomorrow is not certain.

However, we must plan for the future. And so, we also have to look at our mid-term and long-term financial goals.

Mid-term Financial Goals

Mid-term financial goals are a little more involved than everyday goals, but if you are disciplined and work hard, you can still achieve them.

- Mid-term goals include paying off a credit card debt, a loan, or saving for a car.

In order to reach our medium-term financial goals, we have to think further ahead and plan for important things that will happen in our lives in the not too distant future.

They are far enough away that you can use your money to do big things. But not so far away that they feel like a dream.

So, how long will it take to reach a mid-term financial goal?

Try to reach your mid-term financial goals in more than a year but less than five years.

Long-term Financial Goals

Long-term financial goals typically take much more than 5 years to achieve.

Achieving long-term financial goals, such as a funding a uni degree, retirement, or a new home, leads to a big-time compounding effect on your wealth.

Now…

Let’s look at the three kinds of financial goals as a whole. Most importantly, we want to consider our short, medium, and long-term goals collectively.

Why?

Ideally, your short-term and medium-term financial goals are based on your long-term goals. Think of this as the “big picture” when it comes to overall personal finance goal setting.

- You can set your long-term money goals first, then work backwards to set short-term and medium-term goals for a cohesive financial plan.

Examples of Financial Goals

Still unsure what you want to aim for?

Here are some personal financial goal examples to help you achieve financial success sooner rather than later.

Set a Budget

A budget is absolutely necessary. If you don’t have one yet, consider creating a budget as one of your short-term financial goals.

It doesn’t have to be complicated. A pencil and paper will suffice. A spreadsheet or free web-based budgeting tool will also do the job.

Then, when creating your budget, be sure that your spending is within your income. Look for strategies to generate as much extra income as possible with your income exceeding your expenses.

As a result, you’ll know how much money is coming in and where that money is going.

Budgeting personal finances on your way to financial success can be difficult if your expenses are greater than your income.

To live within your means, consider your spending on the following 4 big-ticket expenses:

- Housing

- Transport

- Food and Drinks

- Leisure Activities

Then, think about ways you can cut expenses and save money. Establish a monthly amount to lower these costs as part of your financial goals.

Ask yourself:

- Can I cut my expenses by 5% or even 10%?

Next, set savings goals for the amount you saved.

Make the savings goals worthwhile to ensure that you stay motivated to stick to your budget.

Build Your Emergency Fund

- Building an emergency reserve is another worthy financial goal.

Why?

In life, things happen.

People are made redundant without warning, medical expenses can come up, and accidents occur. Also, cars can break down and may require costly repairs.

One rule of thumb in creating an emergency fund is to save 3-6 months of living expenses.

Set aside this money in a low-risk, high-interest savings account.

Then, unless you have an emergency, don’t touch that money.

Eliminating or Reducing Debt

Depending on your financial situation and how much debt you carry, the goal to get out of debt can be a short-term, mid-term, or long-term goal.

Getting your debt under control is a major factor in avoiding money difficulties.

A sensible short-term financial goal is to pay off your high-interest debt, which only works if you stop borrowing and avoid taking on additional debt.

Do you know what high-interest debts could be causing “leaks” in your budget?

An example here is credit card debt.

Credit card debt carries very high interest rates. There is no better way to spend your extra money than to pay off your credit card balance.

Paying off your credit card debt as quickly as possible is a great example of a short-term financial goal.

The rule of thumb in eliminating debt is easy to remember:

- Pay off the highest interest debt first, then move onto the next highest.

So, once you’ve eliminated your credit card debt, look to pay off your car loan and other personal loans (if you have one).

After paying off your credit card and car loan, look to settle your student loan and other education-related debt incurred.

There are two options for repaying your Higher Education Loan Program (HELP) debt through the Australian Taxation Office (ATO):

You begin to pay back your HELP debt through the tax system once you earn above the compulsory repayment threshold.

Finally, there are people who tend to put off repaying their mortgage.

Paying off your home loan early is a great long-term financial goal which you can fulfil before retiring.

The Process of Eliminating Debt

| Short-term Goal | Pay off high interest debt first: Credit Cards |

| Mid-term Goal | Settle your Car Loan before your Education Loan |

| Long-term Goal | Settle Your Mortgage Before Retirement |

Do you have each of these types of debt?

If so, this is a sensible short-term financial goal:

Just pick one kind of debt and settle it this year.

If you need help to become debt-free and stress-free, you can speak with an expert for free, and they’ll connect you with the right financial advisor who can help get your money sorted.

Retire Early

Ready to leave the grind and retire early?

Set a goal for financial freedom.

Everybody’s goal for financial independence is different depending on your yearly expenses, at which age you decide to retire, and the lifestyle you want to lead.

Here’s the good news:

- Living off your investments and retirement savings is possible.

Yes, you read that right.

But to set things straight:

To save money for retirement is, of course, a long-term financial goal. Unless you are in your 60s, we are talking about a time frame of 5 to 40 years.

There are a few things you need to think about now even though retirement planning may be a long-term endeavour.

Contributing to your super is one avenue to be successful in the future.

Your money can be invested before any taxes are taken out and your investment grows with compound interest.

This is a great way to stretch your investment dollars today, while trying to achieve your long-term goals.

Do you need help creating a plan for early retirement or financial freedom? Hit your retirement goals with the help of your trusted financial adviser.

Savings Goals

Saving infrequently or insufficiently may become one of those financial errors you grow to regret.

The trick to growing your money and building wealth is to save money on a regular basis. You can achieve this by saving for something you value and saving for something fun.

Earlier we mentioned one savings goal – saving for an emergency fund. It’s an important goal to prioritise so you don’t get into debt in case of an emergency.

- Saving for a family holiday is a fun savings goal. You get to visit family and friends, and see new places.

Saving for a holiday is a short-term goal that generates positive energy when you think about the upcoming trip.

We also mentioned saving for retirement, which is a valuable long-term goal.

Some of the things you may also value outside of retirement are a child’s education and home ownership.

Also, the type of financial goal you choose is determined by the age of your children. So, saving for your child’s education may be a short-term, medium-term, or long-term financial goal.

Not preparing for their education can be a costly financial mistake.

First of all, if they are in their pre-teen or early teen years, the rising cost of university is a significant barrier.

This may be the only way to ensure that your child receives the education that you desire.

Set a mid-term financial objective and get started on your child’s education fund right away.

Saving for a deposit on a home, apartment, or unit in a desirable neighbourhood is also a worthy goal.

But before you locate your dream home and reside in that ideal spot, you must save up money for a deposit.

Following your purchase, the deposit becomes equity in your property.

Instead of paying rent, your mortgage repayments each month increase the equity of your property. And, hopefully, the value of your home will rise over time.

How Do You Set Money Goals?

Now that we’ve discussed the three types of money goals and some of their examples, it’s time to dig deeper and discuss how to set financial goals.

To do so, we need to understand what goal setting is.

Goal-setting is the process of taking active steps to obtain your desired goal.

Perhaps you dream to be a millionaire, own a home, or retire early.

Each of these dreams entails setting and achieving large goals. Each of these large goals can be broken down into smaller, more manageable goals that can move you towards accomplishment.

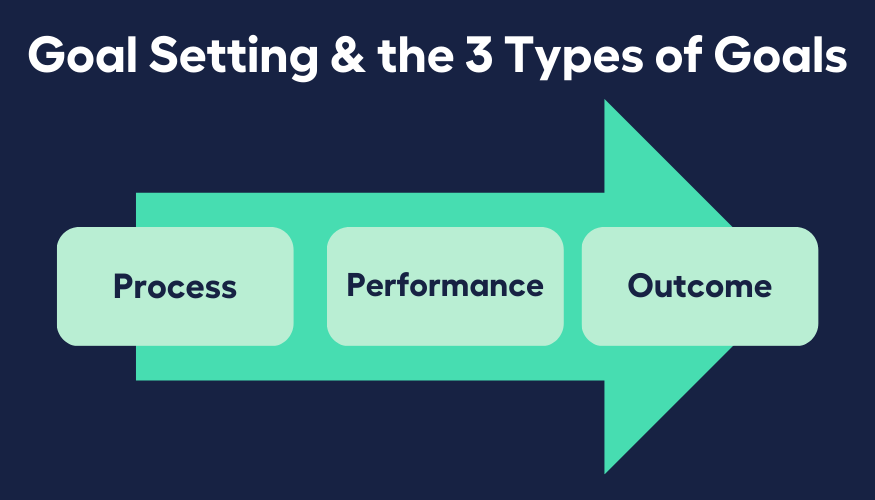

The 3 Types of Goals

Setting goals involves three types of goals:

Process, Performance, and Outcome goals.

Setting financial goals based on outcome, performance, and process goals originated in athletics but is equally applicable to business and personal development.

Whether you are an athlete, the CEO of a corporation or someone in between, this process of setting goals will offer you the tools you need to start preparing like an athlete.

There is a direct relationship between process, performance, and outcome goals.

This is significant because if you meet your process goals, you increase your chances of meeting your performance goals.

Similarly, when you meet your performance goals, you have a better chance of achieving your outcome goals.

Outcome Goals

- Your main objective is your outcome goal, which is simply what you are aiming for.

Outcome goals are frequently binary (goal achieved or not achieved) and revolve around success, such as wanting to win a gold medal or retire with a million dollars.

While outcome goals are extremely motivating, you may have limited control over them because they are affected by how others perform.

In the context of sports, this could refer to someone outperforming you on the playing field.

Or, in terms of retiring with a million dollars, market swings and interest rate changes may have an impact on your investments and savings.

Other examples of outcome goals are:

- pay off credit card debt by the end of the year

- save $100,000 for home deposit

- save $3,000 for a one week holiday in Bali

Performance Goals

A performance goal is a benchmark you are attempting to meet.

If you want to progress towards your outcome goal, you must meet certain performance standards that you establish for yourself.

Performance goals accumulate over time to support you in achieving your outcome goal.

Consider the goal of saving $100,000 for a home deposit in 3 years.

- Saving $25,000 after one year can be your initial performance goal.

- Saving $35,000 in the second year can be the next performance goal after adjusting your budget and earning extra income.

- Saving $40,000 in the third year can be the last performance goal after fine tuning your budget and side hustles.

It is possible to track progress towards your final outcome goal by stacking performance goals in this way; they effectively serve as building blocks for your outcome goal.

Examples of performance goals include:

- A $1,000 voluntary contribution into super

- pay $200 fortnightly to a balance transfer credit card

- save $60 dollars a week for one year to fund your trip to Bali

Process Goals

Process goals help you achieve your performance goals by providing you something to focus on as you work towards them.

Process goals are entirely within your control. You can concentrate on or take action on these little things in order to eventually meet your performance goals.

Examples of process goals include:

- pack a lunch for work everyday

- cut back to one Friday night out per month

- Put $10 a day into your savings account

One of the major benefits of setting financial goals with outcome, performance, and process goals is that it allows you to make progress even if the ultimate result was not what you intended.

Make Your Money Goals SMART

So, how can we set financial goals that we can truly achieve?

Setting SMART financial goals is one tried-and-true solution.

You may have heard of the SMART goal formula:

- Specific, Measurable, Achievable, Realistic, and Time-bound.

But did you know that you may use those factors to boost your chances of meeting your financial goals?

Let’s take a look at each of those factors and how you may use them.

Specific Goals

Your goal must be specific, not general or ambiguous.

Be specific about what you want to achieve and consider how this objective would improve your financial situation. If you don’t know what you want, you won’t get it.

Measurable Goals

Make your financial goal measurable so you can track your progress and overall success.

Express your goals in numbers so you know where you stand and when you’ve achieved them.

Achievable Goals

Setting your goals too high is one of the biggest things that can stop you from achieving them.

The best way to improve your finances is to take small steps you feel confident in achieving.

Realistic Goals

When you set the goal, think about the steps you will take to reach it.

Are those steps possible for you to take right now?

Setting goals that are too high or too low usually leads to disappointment and giving up.

Time-bound Goals

Set a time limit for yourself to reach a goal.

This will make you more likely to finish what you started, stop putting things off, and hold yourself accountable.

The Importance of Setting Money Goals

- Setting money goals can help you spend and smartly save money in your personal life.

Long-term, these goals can help you improve your quality of life, pay off your debt, and plan for a comfortable retirement.

By learning more about these goals, you can plan your finances to fit your lifestyle.

You can go through the process of setting money goals using the DIY route, but if you want less stress and more money success, think about this:

What if you could tap into the wisdom of an experienced finance expert instead of taking the all too common ‘hit-and-hope’ approach?

Many people may be unaware of this…but just like you, 41% of Aussies intend to get financial advice rather than going it alone, according to an Australian Securities and Investments Commission (ASIC) report.

Find the right Financial Adviser for you with the help of your My Money Sorted.

When you book a call with your My Money Sorted, you’ll:

✓ get a better understanding of your financial matters

✓ have an idea of the experts you can call on to help you reach your goals

✓ be matched with the right financial adviser who can help simplify your family’s journey to financial wellness

My Money Sorted is your stress-free pathway to getting ahead with your money. Here’s what your journey will look like:

Step 1: Start off with a quick FREE call with a My Money Sorted team member

Step 2: Get matched with a licensed Finance Adviser that’s right for your money situation

Step 3: Take the first step towards your money goals with a clear and sound roadmap prepared by an experienced Financial Adviser.

It’s that easy!

Setting Money Goals & Not Sure What To Do? Chat with us to Learn How Financial Advice Can Help You.