You have reached a point in life where you’re contemplating retirement plans and how to secure your financial future. You’ve been diligent about saving and investing over the years, including owning an investment property.

However, as you approach retirement age, there’s a burning question on your mind:

“Can you have an investment property and still get the pension?”

In this blog, we’ll discuss the important questions surrounding Age Pension benefits and investment properties. From understanding the impact of rental income on your pension eligibility to learning about the thresholds for income and assets, we will shed light on the rules and regulations governing Australia’s aged pension.

Jump straight to…

Does Having an Investment Property Affect the Pension?

As an Australian resident, understanding the technicalities of the age pension and its relation to investment and property is essential. The age pension, designed to provide financial support to eligible seniors, is subject to specific asset limits as outlined in the age pension asset test.

Pension rates are determined based on an individual’s assets, which include property and investments. For those who fall within the asset limits, they may qualify for a full age pension, while others may receive a part Age Pension if their assets exceed the set asset thresholds.

You may be concerned about how owning an investment property can impact your eligibility for pensions.

There are a few important factors that will affect how owning an investment property will affect your pension. To grasp this better, we’ll explore whether having an investment property affects your pension benefits.

Is Rental Income Considered Income by Centrelink?

Rental income, which refers to the funds you receive from a property you own that is leased or rented out, is indeed considered as income by Centrelink. This income plays a significant role in the income test when assessing your eligibility for the age pension and other Centrelink benefits in Australia.

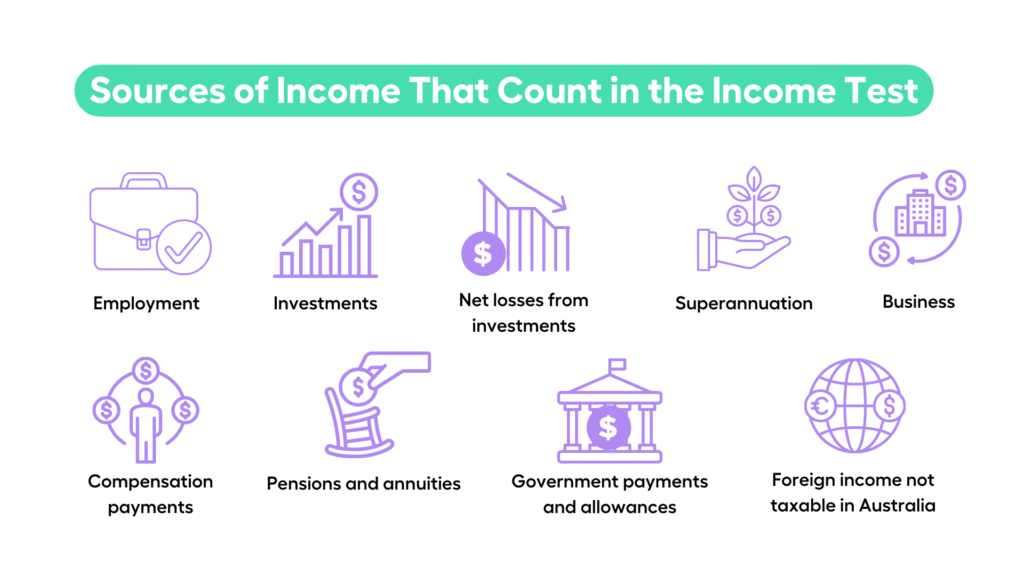

According to Services Australia, income from the following count in the income test: employment, investments (as well as net losses from investments), superannuation, business, compensation payments, account-based pensions and annuities, government payments and allowances, and foreign income not taxable in Australia.

Additionally, the Australian Taxation Office considers several government payments and allowances as income, including age pension, carer payment, Austudy payment, JobSeeker payment, Youth allowance, and Defence Force income support allowance (DFISA). Tax-free government pensions or benefits, such as a carer payment, are also considered income and need to be declared in the tax return.

It’s important to note that there are exceptions to the Income and Assets Test. For instance, government rent assistance is not factored into your income test because it’s considered exempt income.

However, if you are a non-homeowner or a single homeowner and your assessable income, including rental income, falls within the set pension rates and asset limits, you may qualify for the age pension.

The current age pension rates are fortnightly payments, and the maximum rate varies depending on your circumstances.

The age pension assets test is crucial in determining your eligibility, as it evaluates your assessable assets to ensure they do not exceed certain thresholds set by the Australian government. In some cases, your partner’s assets combined with yours are assessed for age pension eligibility payments.

It’s worth mentioning that the Australian government adjusts the age pension rates periodically, often in line with changes in the consumer price index and living and wage increases.

In all cases, it’s advisable to seek professional advice when dealing with age pension entitlements, income tests, and assessable income and assets, as the rules and regulations can be complex.

Understanding the cut-off points, employment income, energy supplements, and how much income is assessable is crucial for age pensioners to navigate the social services system effectively, ensure they receive the support they are entitled to, and forecast their cash flow for a comfortable retirement.

How Much Can you earn from investments and still get the aged pension?

In 2023, the guidelines for obtaining the Age Pension in Australia remain a topic of great interest because they have a direct bearing on retirees’ financial security.

As of July 1, 2023, the pension income-free area is $204 per fortnight for single pensioners and $360 per fortnight for couples living together or apart because of illness, in order to qualify for the maximum Age Pension payment.

But that’s not where the story ends. You may still be eligible for a part-Age Pension even if your income is higher than these limits.

Understanding the complex details of this system is essential because the Age Pension amount gradually decreases by 50 cents for every dollar earned in additional income.

There is even more room for flexibility in 2023 as a result of the most recent adjustment announced in 2022. In conjunction with the pension income free area, a programme called the Work Bonus scheme enables retirees to increase their income without having an impact on their pension.

What Assets Can You Have Before Losing Your Pension?

Assets are items or properties that you, your partner, or both of you have full or partial ownership or an interest in.

Any possessions, real estate, or other interests that you or your partner fully or partially own are considered assets. They might affect the amount of your pension.

Let’s examine the various asset categories.

Financial Investments

These include shares, managed investments, cash, term deposits, bank accounts, and more.

Home Contents, Personal Effects, Vehicles, and Other Personal Assets

Your household goods, personal effects, automobiles, boats, and even licences fall under this category.

Managed Investments and Superannuation

Self-managed super funds, unit trusts, managed investments, and life insurance are all involved. If you are over the Age Pension age or are receiving payments from them, your funeral bonds and superannuation will be assessed.

Real Estate

The majority of real estate assets are subject to the assets test; however, your primary residence and the first 2 hectares of land it occupies are exempt. Properties that you lease out, leave empty, or provide free housing for others are taken into account.

Annuities, Income Streams, and Superannuation Pensions

Payments from accumulated superannuation or items bought with superannuation or other funds are examples of income streams.

There are two primary types: superannuation pensions (paid or purchased from a super fund) and annuities (purchased from life insurance companies).

Shares

Shares held in publicly traded, privately held, and unlisted companies are all taken into consideration.

Gifting

At any time, either you or your partner may donate or gift funds, possessions, or earnings. The maximum gifts that can be made by a single person or a couple combined are $10,000 in a fiscal year and $30,000 over a rolling five-year fiscal period. The effect on your pension will depend on how much is given.

Sole Trader, Partnerships, Private Trusts, and Private Companies

Depending on your level of involvement and control in a business structure, certain assets and income will be evaluated.

Special Disability Trusts

Beneficiaries or contributors to Special Disability Trusts should notify the appropriate authorities in order to take advantage of any applicable concessions.

Deceased Estate

This relates to the possessions that a deceased person had. Any assets or earnings you obtain from a decedent’s estate must be reported within 14 days. You may be legally entitled to the transfer of assets held jointly with a departed partner. Inform the authorities if this occurs.

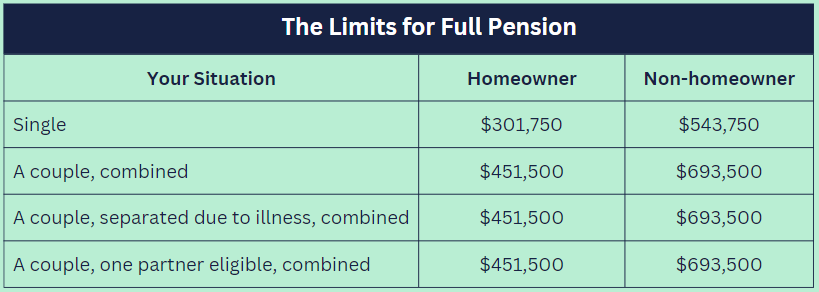

The assets test used in the Australian pension system establishes your eligibility for the Age Pension. Your assets, excluding your principal home, will be valued as part of the assets test to determine whether you qualify for a full or part pension.

As of September 2023, the following asset values are the maximum one may own while receiving a full pension or part pension, whether they be homeowners or non-homeowners, single or a couple.

![What are the limits for a part pension?]](https://lh7-us.googleusercontent.com/ifUpjiYS2jxOya7Gprq2UXHJcHYQ2oXdbIlQDo3EghbWU2OGXAnVOjftWEpVpLTVCDLYQAy3GFOs0QE7ChAF_BqL6b5ONBYIFIcQCE6HnM5PKfNXuB231goLJOJpWZRwOVzGL7BNsFpBOxTf4PsJ6cM)

It’s likely that you are looking for ways to lower your assets in order to pass the age pension assets test if you have begun to consider your retirement income. Your age pension payment might therefore go up as a result of this.

Even though you might not be able to get the entire pension, you might be able to arrange your assets so that you can get a partial pension.

Several strategies can be employed to lower asset levels in order to pass the age pension assets test. which could enable receiving a partial pension or increase the current pension amount.

What is a Principal Home?

A principal home is a place you consider to be your main residence.

The value of your principal home is not assessed as part of your total assets for the purposes of determining your eligibility for the Age Pension because it is exempt from the asset test.

If you once lived in a property and now use it as your primary home, the usual tax exemption for your main residence applies. This means if the property was used to make money, like renting it out, you might only get a partial exemption from capital gains tax (CGT). But if the property was consistently your primary residence, then the regular rules for the main residence exemption still apply.

Income and Assets Test

To determine your eligibility for social security benefits and pension payments, various governmental organisations, including Centrelink, use the Income and Assets Test.

This test is essential in figuring out your financial situation because it considers your income, investments, and possessions. It contributes to keeping the fairness of how government aid is distributed while ensuring that those who need it most receive it.

How Income and Assets Are Assessed

The eligibility for various benefits, including the Age Pension, is determined based on both income and assets. The evaluation of income and assets operates as follows.

Assets Assessment: The assets test takes into account all different kinds of assets. The amount of benefits you may be eligible for depends on the value of your assets and whether you own a home. Real estate (other than your primary residence), investment properties, financial investments, and other assets like cars, boats, and caravans are all taken into account in this assessment.

Income Assessment: One element of the means test used by Centrelink to determine your eligibility for the Age Pension is the Age Pension income test. This income test takes into account your income from a variety of sources, including work, investments, and superannuation. Your income and assets will determine how much Age Pension you are eligible for. It’s critical to understand that your financial assets are subject to a deemed rate of income. Deeming involves a set of guidelines applied to determine the income generated from your financial assets. It operates under the assumption that these assets generate a fixed rate of income, irrespective of their actual earnings.

Taxation of Income: In Australia, the tax system is divided into various income or tax brackets, each of which is connected to a different tax rate. The Australian Tax Office (ATO) and the Federal Government jointly decide on these tax brackets. Australian residents’ taxable income for the fiscal year determines the tax rate they must pay.

Understanding the Value of Assets

When putting assets through the test, all asset types are taken into account. The benefits you qualify for depend heavily on the value of your assets and whether you own a home.

Real estate (other than your primary residence), investment properties, and other assets like cars, boats, and travel trailers are all subject to assessment.

For the purpose of determining your eligibility for the Age Pension, Centrelink evaluates the market value of your assets or those of your partner. If you owe money on assets other than your home, their market value will go down during the assessment.

Assets are typically valued according to their potential market value if you were to sell them. The values of overseas assets are converted to corresponding Australian dollar amounts.

The sale proceeds used for these purposes are not taken into account in your assets test if you sell your house after January 1, 2023, with the goal of using the proceeds to buy, construct, repair, or renovate another primary residence within 24 months. Some assets are exempt from the test, including your primary residence and nearby land (up to 2 hectares on the same title).

Please note that asset assessment guidelines and restrictions are subject to change, so it is best to check with the appropriate Australian government office or a financial adviser for the most recent details.

Life Interest Assets

Assets that give a person the right to use or benefit from a resource for the rest of their lives without actually owning it are known as life interest assets.

Depending on the type of asset and the date of sale, life interest assets are valued differently for social security purposes. Life interest assets are typically not considered to be assets for social security purposes unless they fall under one of the exceptions.

Life interests in granny flats, properties that aren’t the primary residence, and life interests in sold properties are examples of exceptions to the exempt asset rule. The asset exemption period for homes sold after January 1, 2023, is up to two years from the sale date.

Furthermore, a life interest is a provision made in a Will that establishes a Trust with the beneficiary having access to the asset while the executor maintains legal control over it. A life interest can come with important conditions, such as the life tenant’s right to ask that the property be sold in order to buy another one or to pay for a refundable accommodation deposit should they need to enter an elderly care facility.

Retirement Villages as Assets

Retirement villages are a particular kind of housing for senior citizens who can typically live independently but may need some help with basic daily tasks. They are private contractual arrangements in which residents pay all associated costs on their own dime without government assistance.

Both the land and the building in the retirement community are owned by the operator, and residents typically sign a lease or licence agreement to obtain the right to occupy the space.

Retirement communities are governed by state law, so the regulations differ from state to state. The state-based Retirement Villages Act does not regulate fees charged for services and instead focuses more on issues relating to contracts and consumer protection.

In order to improve transparency regarding the upkeep and cost-recovery of the village’s assets, the NSW Government has proposed a reform. The proposal seeks to guarantee that residents have a voice in how their village is run and that they are not unfairly charged for upkeep and repairs.

For social security purposes, a person’s former principal residence is assessable if they are residing in a retirement community. A person must pay an entry contribution (EC) amount to secure housing in a retirement village, which is the sum of all payments made to the community unless they can demonstrate that a particular payment had nothing to do with acquiring the right to housing.

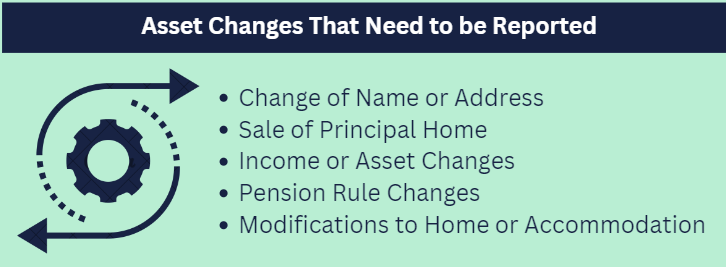

What Changes You Need to Report

It’s critical to report any changes that might affect your age pension payments if you own investment property and will be receiving a pension. What you need to report is as follows.

Change of Name or Address

Immediately inform Services Australia of any changes to your name or address. Reporting changes to your name or address guarantees that government payments and correspondence find you correctly. If this information is not updated, communications may be delayed or misdirected.

Sale of Principal Home

For the accurate evaluation of your assets, you must report the sale of your primary residence. Your pension eligibility and payment amounts are consequently impacted by this. If this change is not reported, the pension calculations might be off.

Income or Asset Changes

Your pension benefits may be significantly impacted by changes in your income or assets. Age Pension payments are distributed according to need using the income and asset tests. Failure to report changes could lead to overpayments or underpayments, which could necessitate repayment or have an impact on your capacity to manage your finances.

Pension Rule Changes

It’s important to stay up to date on pension rule changes in order to understand how they may affect your payments. Unexpected reductions in pension benefits or missed opportunities for additional support could result from a failure to adapt to these changes.

Modifications to Your Home or Accommodation

If you own an investment property, it is accounted for in the asset test’s asset test and the income test’s income test, and any rental income is accounted for. Failure to report changes to your home or lodging may result in incorrect assessments, which could have an impact on your pension payments.

Disclosing these changes guarantees the fairness and accuracy of your pension payments. It assists governmental organisations in making accurate calculations based on your current situation, avoiding overpayments, underpayments, and potential future monetary difficulties.

Ultimately, navigating the complex interplay between financial assets and age pension entitlement requires careful consideration of specific circumstances and regular monitoring of policy updates.

This is where consulting with a financial adviser can be crucial. A financial adviser can help you make the most of your financial investments and age Pension too.

Need a Retirement Plan or Estate Plan? Book a FREE 15 min Call or Send Us Your Questions to Get the Right Help!