Imagine planning for that once-in-a-lifetime getaway, the deposit securing your dream home, or fortifying a safety net against life’s unforeseen surprises.

Yet, a stark truth dawns upon you: the journey to financial security isn’t a straightforward path, but a landscape marked by challenges and uncertainties.

Effective risk management is the key driver towards achieving your financial goals. By managing risks related to investments, cash flow, and market trends, you can create a solid foundation that safeguards your financial future.

In this article, we will cover the fundamentals of financial risk management for personal finance. We’ll look at the various risks that you might encounter regularly, from minor risks to volatile long-term risks.

What is financial risk management and why is it important?

The world is full of ups and downs, and that’s where financial risk management steps in. This process is all about spotting and managing those potential risks, giving them a good once-over, and then doing what’s needed to keep them from raining on your financial parade.

Having a solid financial risk management plan will help you lower the impact of problems and maybe even avoid bad outcomes. This will also let you find the right balance between the risks you’re willing to handle and the opportunities for your money to grow since risks sometimes come with good outcomes too.

You can’t completely get rid of risks, but you can do some research and planning to prepare for potential situations you might face. With this detailed information, you can decide which risks are okay to take, which ones you can reduce, and which risks you’d rather avoid.

Types of Financial Risk

Risks cannot be completely eliminated, but risk mitigation is still possible by consulting a professional and being knowledgeable about the different financial risks you might encounter. There are different types of risks, such as:

Interest Rate Risk

Financial planning must include interest rate risk management in order to lower risks. Interest rate risk refers to the possibility that your capital and investments may experience a decline in value as a result of fluctuations in interest rates. Now, let’s look at an example.

Alex recently acquired a collection of bonds with a fixed interest rate of 3.5 per cent. These bonds were designed to deliver a consistent income stream over the following ten years. The Reserve Bank of Australia, however, decided to lower the official cash rate in response to the economy’s slowing growth as a result of unanticipated economic risk events. The market interest rates for bonds with a similar maturity start to decline as a result of this interest rate reduction.

Market Risk

Market risk refers to the possibility of financial losses brought on by changes in the general market environment. Market risks can impact your investments, retirement savings, and overall financial stability. Here’s a story.

Mark is putting money away for the future as part of his business decisions. He has stock in several businesses. However, due to global and local problems, the economy experiences a rough patch. The stock market declines as a result, which significantly reduces the value of Mark’s shares.

Sector Risk

Sector risk is used to describe potential financial losses that could result from changes in a specific sector or industry.

Imagine this scenario. Sarah has invested a sizable portion of her funds into the real estate sector, as property prices have been steadily rising in her city. However, new regulations caused an abrupt change in the real estate market. As property values begin to decline, so does demand for housing.

Currency Risk

Currency risk is the possibility of financial losses as a result of changes in foreign exchange rates.

Meet Lisa, a stock investor who chooses to place some of her savings in foreign securities. Sarah can purchase more USD with each AUD she converts because the AUD-USD exchange rate is favourable at the time of her transaction. However because of various factors, exchange rates changed, which decreased the value of her money.

Liquidity Risk

Having insufficient cash flow to pay bills and debts as they become due can result in potential financial losses known as liquidity risk.

Think about the case of Ben, who bought a rental house in Brisbane to secure his future. But the economic downturn and a sudden loss of employment resulted in a decline in property value and a threat to rental income. Due to the decreased investment value and uncertain income, he had no choice but to sell his property to meet his financial needs.

Credit Risk

Credit risk is the possibility of financial losses resulting from a borrower’s inability to pay back any kind of debt or loan.

Let’s dive into a case. A businessman named Michael obtains a loan to support his business venture. At first, his business units were successful, but he eventually encountered operational risks. Michael now has trouble paying his financial obligations back due to inconsistent cash flow. With his missed and late payments, his creditworthiness declines. The terms of his loans are tightened by the lenders, who raise the interest rates and impose penalties because they are worried about the credit risks associated with his company, which can also lead to reputational risks.

Concentration Risk

Concentration risk is the term for possible financial losses brought on by a lack of diversification in your portfolio management.

Here’s an example. Alex, an avid property investor, decides to concentrate all of his investment efforts on buying properties for rental. Alex has enjoyed solid rental returns for many years, but he has a sizable concentration in just one asset class: real estate. As the years pass, a series of economic shifts impact the real estate market. Because of the economic difficulties, Alex has more rental vacancies at all of his properties, which affects his rental income and cash flow.

Inflation Risk

Inflation risk describes the potential effects of price increases on the long-term value of investments and the purchasing power of money. Let’s explore with a story.

David plans to rely on his savings and investment income to maintain his desired lifestyle in retirement. However, due to inflation, his income loses some of its real value, making it harder for him to comfortably pay his bills.

Timing Risk

When buying or selling an asset based on future price predictions, there is a risk of timing errors that could result in financial losses. Here’s a situation.

Mark has been diligently saving for a down payment on a property. As he waited for the “perfect time,” the property prices went up instead.

Gearing Risk

Gearing risk is the possibility of experiencing financial losses as a result of borrowing money to invest in securities like stocks, real estate, or managed funds. Consider the following.

Jane obtains a mortgage to pay for a sizable portion of the purchase price of the property in the hope that rental income and capital growth will produce sizable returns. However, if the value of the property drops, Jane’s losses might exceed her initial investment, and she still has to pay the mortgage.

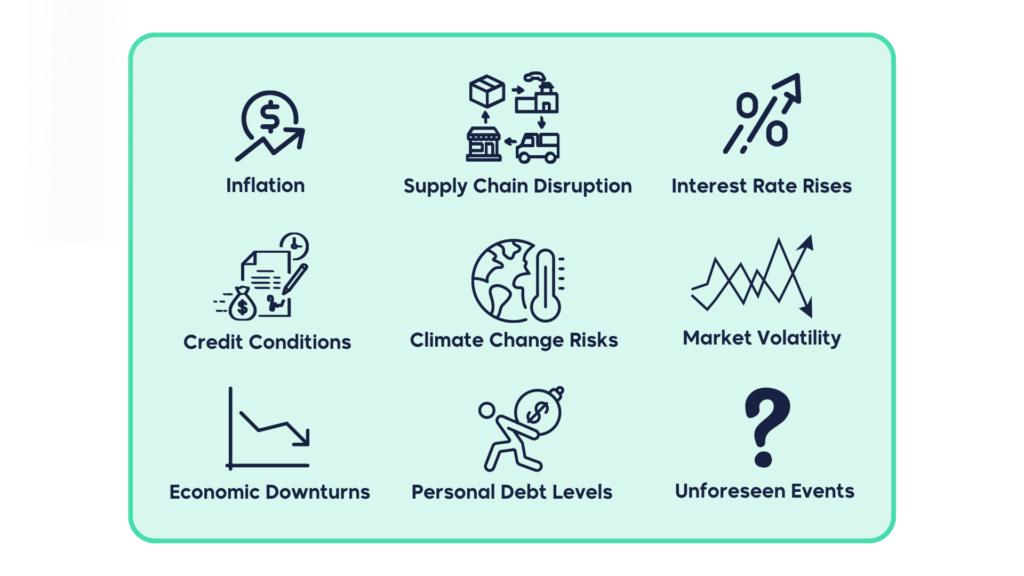

Causes of Financial Risk

The cause of financial risks can be attributed to several key drivers. Here are some of its many forms.

Inflation

Increasing inflation causes financial risk as it can reduce the value of savings and investments and reduce the purchasing power of money.

Supply Chain Disruption

Disruptions in the global supply chain, such as those brought on by calamities or geopolitical events, may raise prices and decrease the availability of goods and services, which can cause financial risks.

Interest Rate Rises

The cost of borrowing may rise as interest rates do, making credit more expensive for both individuals and businesses to access. Risks arise for people and many organisations who must borrow money to maintain their finances.

Credit Conditions

Stricter credit requirements can pose a risk of reduced employment and economic activity. When businesses encounter identified risks or operational risks, they may have a harder time getting credit. This results in trouble getting the money they need for daily operations, expansion, or even just covering expenses. These operational risks lead to fewer hires, failed strategic objectives, job reductions, or even business closures, which would raise the unemployment rate, and slow economic growth.

Climate Change Risks

For financial institutions, climate change brings both opportunities and risks. Financial institutions may be affected by identified risks such as increased weather variability and extreme events, and they may also face transitional difficulties as a result of the transition to a low-carbon economy.

Market Volatility

Financial market fluctuations pose risks by reducing the value of investments and causing losses for investors.

Economic Downturns

Economic downturns or recessions can result in decreased consumer spending, certain strategic risks, company closures, and job losses, which can have a potential impact on people’s financial security.

Personal Debt Levels

High levels of personal debt, such as credit card debt or mortgage debt, may increase financial vulnerability and default risk.

Unforeseen Events

Unexpected occurrences can significantly affect a person’s finances, including natural disasters, medical emergencies, and major accidents.

How is financial risk measured?

Having a thorough understanding of risk related to your finances is essential for navigating the complex world of personal finance. For people looking to protect their assets and reach their financial goals, risk assessments are important. Employing accurate risk assessments and measurement techniques in this situation is essential because it acts as a compass to direct wise decisions and risk management strategies. Here are some ways to measure financial risk:

Debt-to-Equity Ratio

The debt-to-equity ratio is a metric used to assess a person’s financial situation. This ratio sheds light on the relationship between debt and ownership by comparing the total debt to the total equity, or net worth. It’s a useful instrument for determining the level of financial leverage and related risk.

Consider a person who has $200,000 in equity and $100,000 in total debt. They would have a debt-to-equity ratio of 0.5 ($100,000 / $200,000), which indicates that they have $50 in debt for every $1 in equity. The context and standard practices in the industry can affect how this ratio is interpreted. A lower ratio might denote a more conservative financial structure, whereas a higher ratio might suggest increased financial leverage that could increase risk.

Interest Coverage Ratio

An important indicator of a person’s ability to manage interest payments with their income is the interest coverage ratio. This metric provides a crucial indication of financial risk by revealing whether a person’s income is sufficient to meet interest obligations.

One example is a person with a $10,000 annual interest obligation and a $30,000 annual income. Their interest coverage ratio in this case would be 3 ($30,000 / $10,000), showing that their earnings are three times what is needed to pay interest. A higher ratio typically denotes a more stable financial situation because there is enough income to pay off debt. A lower ratio, on the other hand, might point to potential difficulties in covering interest costs and possibly indicate greater financial risk.

Standard Deviation

A statistical tool called standard deviation can be used to measure how volatile or variable investment returns are. It provides information about the size of return fluctuations, with a higher standard deviation indicating higher risk due to higher return variability.

Consider two investment portfolios. Portfolio A’s standard deviation is 10%, with an average annual return of 8%. Portfolio B’s standard deviation is 15%, with the same average annual return of 8%.

Portfolio B has a higher standard deviation than Portfolio A, which suggests that its returns are subject to more significant fluctuations.

Therefore, Portfolio B carries a high risk due to the possibility of more unexpected changes in returns, which highlights the significance of assessing standard deviation when evaluating investment options.

Sharpe Ratio

The return on an investment is compared to its risk exposure using the Sharpe ratio. This provides a way to compare various investments, taking into account their unique risk and return characteristics, by taking into account both the investment’s return and its volatility.

Imagine you’re thinking about two different ways to invest your money: let’s call them investment X and investment Y. Both investments X and Y give you the same average return over a year. But their returns don’t behave the same way. You want to figure out which one might be better for you.

To understand these investments better, we use the Sharpe ratio as a tool that helps us decide if the extra money we might make is worth the extra risk we’re taking.

Beta

The responsiveness of an investment to changes in the market is measured using beta. It demonstrates the extent to which the price of an investment may alter in response to broader market changes. A beta value greater than 1 indicates higher risk because the investment is likely to be more volatile than the market as a whole.

Let’s say there’s an Australian stock with a beta of 1.2. This means that, on average, when the overall Australian market goes up or down by a certain amount, this stock could go up or down about 20% more than the market’s change. So if the market goes up by 10%, this stock might go up by 12%, but if the market goes down by 10%, this stock could go down by 12%.

On the other hand, if there’s a stock with a beta of 0.8, it suggests that this stock tends to be more steady when the market moves. When the market goes up or down, this stock might only go up or down around 8% while the market changes by 10%.

Value at Risk (VaR)

Value at Risk (VaR) is a mathematical tool that estimates the largest loss an investment or group of investments could sustain over a specific period with a specific degree of confidence. It’s similar to envisioning your investments in the worst-case scenario.

VaR acts as a safety net by indicating the maximum loss you could sustain from your investments, assuming a certain level of confidence. It assists you in comprehending the potential downside or risk of your investments, which is a crucial step when deciding where to invest your money.

R-Squared

R-squared measures how much of the ups and downs of an investment can be explained by comparing it to a benchmark index. It’s similar to observing how closely a particular investment’s performance tracks that of the entire market.

Higher R-squared values imply that the investment behaves similarly to the market. This could imply that your investment may experience difficulties if the market does, making it somewhat risky. On the other hand, if the R-squared is lower, the investment may not closely track the market. If the market experiences difficulty, it is less risky.

Solvency Ratios

Solvency ratios are tools for determining a person’s ability to manage their debt. It is a tool that helps you understand if you can manage the money you owe, or if it might be too much for you.

The debt-to-assets ratio is a number that tells us how much of what you own is owed as debt. A higher debt-to-assets ratio means that you are more likely to be at financial risk because you owe more money relative to your assets. An improved balance between what you own and what you owe, indicated by a lower ratio, may indicate a less risky situation.

Financial Risk Management Process

Managing financial risks is a very important part of making smart financial plans. Imagine it like taking steps to avoid risks and protect your money and future.

Determining and Assessing Risks

It is a crucial step to prepare risk management strategies for the types of risks that could affect our money in the same way that we do in our daily lives, such as carrying an umbrella when there is a chance of rain. These unpredictabilities are referred to as “risks,” and they can include things like inflation, job loss, unforeseen health issues, or even shifts in the cost of borrowing money.

Consider the likelihood of a risk occurring as well as the potential amount of trouble they could bring. Losing your job, for instance, carries some risks, but how likely is it to occur? Would it have a negative impact on your plans? We can better understand which risks to plan for by doing this.

We can begin deciding how to protect ourselves once we are aware of the risks and how serious they may be. Similar to using a seatbelt while driving, it keeps us safe. In case of an emergency, we might put aside a little extra cash, purchase insurance, or change our plans to allow for more flexibility.

Risk Acceptance and Risk Avoidance

Risk management is an ongoing process that needs constant attention and adjustment.

Risk acceptance means being ready for unforeseen events while wishing for the best possible financial situation. Consider taking care of your personal finances as you would your house. Even if you are careful with your money, you may face some financial difficulties in life.

On the other hand, risk avoidance means being cautious and avoiding situations that could seriously hurt your finances. It’s like avoiding big financial mistakes so your financial journey is smoother.

Finding the right balance between these two approaches is important to keep your financial well-being in check and avoid risks.

You want to make sure your financial instruments remain strong even during challenging times. Planning carefully for these risks, employing strategic objectives, diversifying your investments, and keeping an emergency fund on hand all help with risk reduction. You can navigate financial risks more successfully by getting expert guidance and managing market and economic developments.

External Risks and Risk Events

External risks and risk events are two crucial considerations when it comes to money management. External risks, such as changes in the economy or natural disasters, are similar to unpleasant surprises that could have an impact on your finances. These events are out of your control and may affect your financial security. On the other hand, risk events are specific things that may occur suddenly, such as losing your job or having unexpected expenses. To be ready, it’s critical to be aware of both these external risks and risk events.

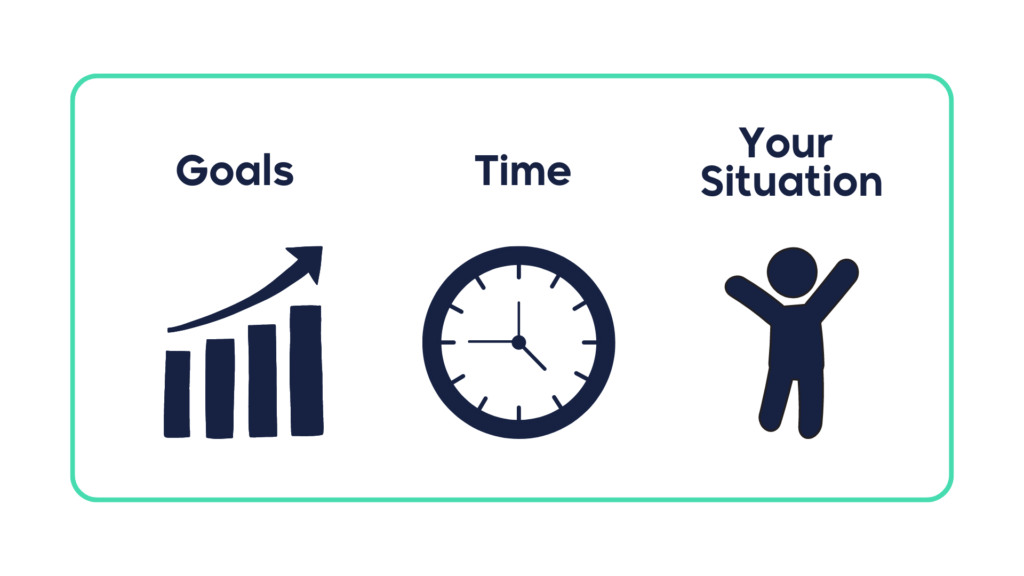

Establishing Risk Tolerance

Consider how comfortable you are with managing finances and taking a chance when making financial decisions, such as when you want to grow your money. This is dependent upon your financial goals, the amount of time you have until you need the money, and your current circumstances.

Goals

Think about your financial aspirations. Are you setting aside money for a specific goal, such as a home purchase or a comfortable retirement? Risk levels may vary depending on the goal.

Time

Consider the amount of time you have before using the money you are investing. If you have a lot of time, you might feel more at ease with your investments experiencing some ups and downs because you’ll have plenty of time to recover if things don’t go your way.

Your Situation

Your own particular circumstances are important. Have you got any additional income or savings? How might a temporary decline in your investments affect you?

Knowing all of these things will help you determine how much risk you can tolerate. Similar to choosing how fast you want to drive on a road, some people are fine going fast while others prefer to go slower and safer.

This makes it easier for you to select investments that are in line with your comfort zone and reduces your anxiety when their values fluctuate over time.

Developing Risk Management Strategies

It’s time to create risk management strategies to address significant risks once you’ve determined the things that could go wrong with your money and how much risk you’re willing to take.

Consider it like getting ready for various weather conditions:

Hedging Strategy

In terms of personal finance, hedging is about having an investment backup plan. To avoid losing all of your money if something goes wrong, it’s like placing a wager on both sunny and rainy weather. This aids in risk management and financial security.

Diversifying Investments

In the same way that you wouldn’t pack your entire wardrobe in a single bag in case it was lost, you shouldn’t invest all of your cash in a single asset class to avoid the risk of losing everything in case something unexpected happens. You can choose to divide your funds among various investments so that if one performs poorly, the others might compensate and keep things in balance – this is known as diversification.

Saving for Emergencies

Savings for emergencies are like an umbrella on a rainy day. It’s a crucial step to save some cash for an emergency fund. This money is set aside in case of potential threats and risks, such as an unanticipated medical bill or an abrupt job loss.

Getting an Insurance Coverage

Insurance can be compared to wearing safety equipment when engaging in risky activities. If something unfortunate occurs, having coverage such as a car accident, health issue, or life insurance means that the insurance will help cover the costs so you won’t have to pay everything out of pocket.

Having a Backup Plan

It’s a good idea to create strategies for unforeseen circumstances to avoid risks. If something goes wrong, this might mean modifying your spending or finding temporary ways to make money.

By taking these risk management processes, you’re ensuring that you’re prepared for potential difficulties and that you have strategies for handling them. You’re being prepared, just like when you buckle up in a car to stay safe or carry an umbrella in case it rains.

Monitoring and Reviewing

It is important to keep an eye on your money and the plans you’ve made to stay safe financially. It is crucial to check if anything in your life has changed, or if some new things or risks could affect your finances. Also, see the market trends. If anything is different, you might need to change your plans a bit to keep everything on track and make sure your money stays safe from risks.

Seeking Professional Advice

Consider seeking advice from a financial planner or advisor who has experience managing risks. They can assist you in determining your risk tolerance, creating a unique risk management strategy, and offering ongoing support and guidance. Collaborating with project teams is also essential as they can help align strategies to confront risks head-on. Getting all of the viewpoints would be ideal for decision-makers.

Understanding and managing potential risks are two crucial aspects of financial risk management. It’s similar to creating sturdy pillars for your financial stability. Learning how to manage risks gives you the ability to safeguard your finances and confidently pursue your objectives.

Incorporating risk management into your financial plans is not only wise but also a way to take control of your future. As you embark on this journey, consider seeking assistance from financial professionals who can help you come up with an effective risk management strategy and risk mitigation.

Keep in mind that planning ahead and making wise decisions are the keys to securing your financial future. What you do today can strengthen and improve your future.

Speak with a Money Guru Today to Get Your Money Sorted Today