Looking for investments that could help you achieve a comfortable lifestyle in retirement?

One way to grow your money and potentially increase your retirement income is to invest it in passive investments like shares or super.

Did you know that a super fund invests in the stock market, buying shares on your behalf using the money in your super?

You must be thinking:

Doesn’t that mean that putting my money in super will give me the best of both worlds?

So, you could now be considering whether it makes sense to invest more money in your super or to invest in shares outside of super.

Could this be a case where too much of a good thing is a good thing?

Before you decide which you should invest in for a better retirement, let’s take a deep dive into what makes them both unique investment options.

Jump straight to…

Retirement Investment Strategy: Contribute to Super or Buy Shares

While mandatory employer super contributions make up the bulk of superannuation for many Aussies, you can also make personal voluntary contributions to your super. This is an excellent way to save and invest more of your salary.

The Australian Taxation Office (ATO) suggests keeping track of your super and adding to it at least 10-15 years before your target retirement age, so you have time to make up the difference between your retirement goal and your final super fund balance.

Another option is to invest in shares listed on the stock exchange outside of your superannuation just like the 9 million adult Australians who hold investments outside of their super.

According to an Australian Securities Exchange (ASX) study, more than half of adult Aussies have direct share investments, and the number of new investors has increased in the last two years. Furthermore, women account for 45% of all new investors.

A personal share portfolio and superannuation are both investments in shares, and if that’s the case…

- Which is a better investment – super or shares? Is it necessary to have both? Both options have benefits and drawbacks, so you must weigh up a variety of considerations before choosing which is ideal for you.

Investing in Superannuation

There are a variety of strategies for growing your super to improve your retirement lifestyle.

But before you start thinking of growing your super, you need to first know where you stand with your super.

In most cases, if you have a job, your employer is required to contribute to your super fund. This is known as the super guarantee (SG), and it is something the Australian government put in place as a legal requirement.

If you are a contractor who is primarily hired for your labour, you may be able to choose which super fund receives your contributions when you are considered as an employee for super guarantee purposes.

You do not have to pay the super guarantee if you are self-employed as a sole trader or in a partnership. You can save for retirement by making personal super contributions.

How Much Super Guarantee are You Entitled to?

If you are eligible for the super guarantee, your employer must deposit a minimum amount of your regular income into your super. This is deposited at least once every three months depending on the current super guarantee rate, which is 10.5% for this financial year, in order to avoid the super guarantee charge.

| SUPER GUARANTEE CONTRIBUTION QUARTERS | |

| QUARTER | PERIOD |

| 1 | 1 July to 30 September |

| 2 | 1 October to 31 December |

| 3 | 1 January to 31 March |

| 4 | 1 April to 30 June for Q4 |

The quarterly super contributions schedule follows the Australian financial year. Thus, the

- 1st quarter is for the period of 1 July to 30 September,

- 1 October to 31 December for Q2,

- 1 January to 31 March for Q3,

- and 1 April to 30 June for Q4.

So, if your ordinary income was $8,000 for the first quarter of the 2022 to 2023 financial year, your employer would have paid $840 into your super, which is 10.5% of $8,000.

| Computing for Super Guarantee Quarterly Contribution | |

| Period: 1 July to 30 September (Q1) | |

| Ordinary Time Income | $ 8,000 |

| Multiplied by Super Guarantee Rate | 10.5% |

| Super Contribution for Q1 | $ 840 |

Keep Track of Your Super

As of June 30, 2020, Australians had around $13.8 billion in lost or unclaimed superannuation from approximately 6 million lost and ATO-held accounts.

Could some of this be your money?

It’s best to find out if you have some money floating around and claim it. You can look for your missing super by:

- utilising MyGov online

- calling the Australian Taxation Office super lost search line (13 28 65), or

- by filling out a paper form

If either of the following occurs, your super fund will record you as a lost member:

- They have been unable to get in touch with you.

- In the previous five years, they did not receive any contributions or rollover funds for you.

- As a lost member account for which no new address has been found, your account was transferred from another fund.

Although the super fund still has your money, the ATO keeps a list of members who have been reported as missing.

The unclaimed funds the ATO might be holding on your behalf include the following:

- Unused superfunds for:

- a participant who is 65 or older

- an associate spouse

- a late family member

2. Super funds that former temporary Australian inhabitants have not claimed

3. Specific accounts for lost members

4. Lost accounts with less than $6,000 in balance (small lost member accounts)

5. Accounts that have gone missing after five years of inactivity and whose records are insufficient to ever identify their owner (insoluble lost member accounts)

6. Low-balance accounts that are inactive

Growing Your Super

In order to increase your super, you can enter into a salary sacrifice agreement with your employer, make personal super contributions, or you might be qualified for government contributions. You can also contribute to your spouse’s super.

Do note that there are restrictions on how much you can put into your superannuation each year.

1. Salary Sacrifice Arrangement

A salary sacrifice arrangement or salary packaging is an agreement with your employer to forgo part of your pre tax salary or wages and pay it into your super fund.

Called concessional contributions, payments through the salary sacrifice arrangement are taxed at 15%—an amount that may be lower than your marginal tax rate. In this example you benefit because you pay less tax and increase your retirement funds at the same time.

If your income is more than $45,000 annually, paying through a salary sacrifice arrangement may have tax benefits.

However, your salary sacrifice contributions and employer contributions cannot total more than $27,500 each fiscal year.

2. Personal Super Contributions

You may add more than $27,500 to your super each fiscal year if you choose to do personal super contributions, which are paid with after tax income.

Also known as non-concessional contributions since you already paid income tax before making the contribution; you can pay up to $110,000 in after tax contributions for each financial year.

Personal contributions will count towards your after tax contributions cap unless you have claimed a tax deduction for them.

3. Government Contributions

If you’re just starting your journey in the workforce or your income isn’t large enough for a salary sacrifice arrangement or personal super contributions, the government may make additional contributions to your super in certain situations.

You are not required to apply for these government superannuation contributions. If you are eligible and your fund has your tax file number (TFN), the government will automatically pay it to your fund account either via the super co-contribution or the low income super tax offset.

- Super Co-contribution

The super co-contribution assists eligible low or middle-income individuals who make personal after tax income contributions to their super fund.

- The government will match your after tax contributions up to a maximum of $500.

You can request a direct payment if you are now retired and do not have an eligible super account that will accept the co-contribution.

- Low Income Super Tax Offset

The low income super tax offset (LISTO) is a $500 government superannuation payment designed to assist low-income earners in saving for retirement.

- If your annual income is $37,000 or less, you may be eligible for a LISTO payment. This is usually deposited into your super fund.

The LISTO is 15% of the pre-tax super contributions paid into your super fund by you or your employer.

The maximum payment for a fiscal year is $500, and the minimum payment is $10.

You don’t have to do anything to get a LISTO. Simply ensure that your super fund has your tax file number (TFN) – without your TFN, your super fund will be unable to accept LISTO payments.

4. Spouse Contributions

A little known practice is to split your employer super contribution with your spouse. Splitting your contributions means transferring or rolling over a portion of your recent contributions in your super account to your spouse’s super account. You can diversify with different fund types when doing so or go for a balanced option.

You may also be able to claim a tax offset if you contribute to the super fund of your spouse who earns low or no income. The ATO refers to this as super-related tax offsets.

Advantages of Investing in Super

When you consider the many different ways to grow your super, it’s easy to see the benefits of doing so. We came up with eight.

8 Benefits of Investing in Super:

- Pay Less Income Tax

- Pay Less Tax on Investment Returns

- Long-term Growth Benefit from a Professionally Managed Super fund

- Automatic Insurance Coverage with No Health Checks

- Beneficiary Plan

- Protection Against Bankruptcy

- Tax Free Retirement Income

- Ability to Diversify and Invest in Big Assets

1. Pay Less Income Tax

A salary sacrifice agreement with your employer means that your contribution will be taxed at only 15% up to certain limits.

Voluntary after tax super contributions may also deliver added benefit as you may be able to claim a tax deduction for them.

2. Pay Less Tax on Investment Returns

The investment earnings on your super balance while you are in an accumulation phase are generally taxed at the low rate of 15%. Unlike income earned in investments outside super which are taxed at your marginal tax rate.

3. Long-term Growth Benefit from a Professionally Managed Super Fund

Provided you have carefully selected your super fund, you will have comfort in the knowledge that your money is being managed actively by professionals whose job it is to generate the best long term returns on your investment.

4. Automatic Insurance Coverage with No Health Checks

Because super funds can negotiate a better deal on group insurance, the premiums for insurance held within super may be cheaper than those held outside of super. Premiums for insurance held within super are automatically deducted from your super, meaning you avoid paying for premiums with your after tax income.

Most super funds offer new members death and total and permanent disability (TPD) insurance through their super. This can be a cost effective way of securing cover.

5. Beneficiary Plan

Super is the second largest asset for most Australians after their residential home. However, super doesn’t automatically become part of your estate upon your death. A binding beneficiary nomination gives you peace of mind that your super benefit goes to your intended beneficiary when you die.

6. Protection Against Bankruptcy

Investing in a super fund has less risk because bankruptcy will not affect your retirement savings if they are held in a regulated super fund, and your money will be protected from creditors. In a similar vein, any money taken out of your retirement plan following bankruptcy is typically protected.

7. Tax-Free Retirement Income

Depending on the year you were born, you can usually access your superannuation tax-free once you reach the age of 60 and retire. This is available to you whether you withdraw money through a superannuation income stream or as a lump sum, as long as you are a member of a taxed super fund.

8. Ability to Diversify and Invest in Big Assets

Since superannuation is one large investment portfolio in which your money is pooled with the retirement savings of other members, you can invest in assets that you may not be able to access with your savings as an individual.

With so much purchasing power, superfunds can invest in various companies, different industries, and also private assets like airports or even highways. This can provide you with a unique opportunity to participate in investments that are not publicly available.

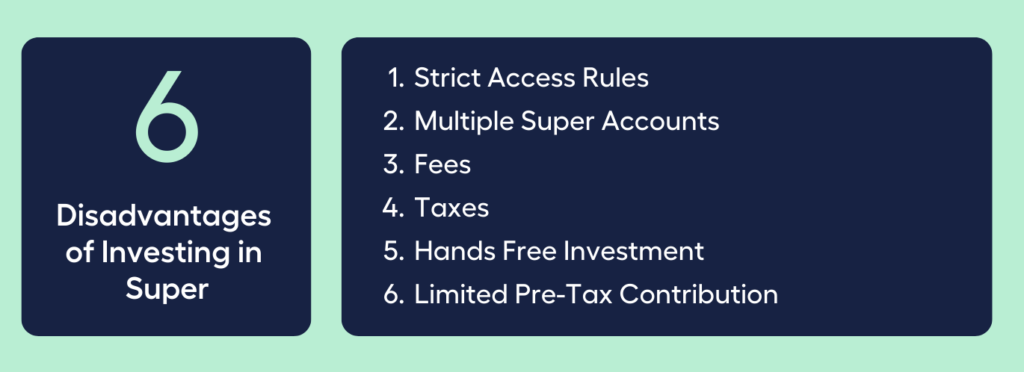

Disadvantages of Investing in Super

With all the regulations set up to protect you and your money in super funds, it’s difficult to find drawbacks, but we managed to identify six disadvantages.

6 Disadvantages of Investing in Super

- Strict Access Rules

- Multiple Super Accounts

- Fees

- Taxes

- Hands Free Investment

- Limited Pre-Tax Contribution

1. Strict Access Rules

Money invested in super cannot be used for emergencies, personal needs, or family goals such as paying for your children’s private education.

Super’s limited access rules are in place to encourage people to only put their super towards long term goals such as retirement.

2. Multiple Super Accounts

Employees changing employers may result in multiple super accounts being opened in an employee’s name as employers typically have different default super funds for the super contributions they make.

Employees who have changed jobs may have to pay multiple fees on multiple super funds.

To avoid paying multiple fees and taxes, make sure to discuss your concerns with your employer

Even if your employer already has a business relationship with a specific super fund, you have the freedom to choose which super fund your contributions will go to.

3. Fees

There may be fees associated with your super fund that offset some of the tax advantages.

It’s critical to consider your super’s fees, as well as risk, returns, and services, to see if you could be getting a better deal. Switching to a lower-cost fund and similar investments can save you a lot of money over time.

4. Hands Free Investment

Another downside to professionally managed super funds like Balanced or High Growth funds is that you cannot invest in individual shares.

5. Limited Pre-Tax Contribution

You’re limited to a pre-tax contribution of $27,500 a year. Should you wish to contribute more to your super, you have to do so with your after tax income.

Investing in Shares

- A single share essentially represents one piece of ownership in a company.

The Australian Securities Exchange (ASX) — also known as the share market or stock exchange — is home to many large corporations. The ASX lists over 2,000 companies, not just large and well-known corporations.

When you buy a small number of shares in one of these companies, you own a small portion of the company.

To conduct the actual transaction of buying or selling shares, you must use a third party known as a ‘broker’ or a share trading platform.

How Do You Profit from Shares?

People make money by investing in shares in one or both of the following ways:

1. An increase in the value of the share.

Known as ‘capital growth’ or ‘capital gain,’ this simply means that you make money by purchasing shares at one price and selling them at a higher price.

In contrast, keep in mind that if the share price falls below the amount you paid and you sell shares at that lower price, you will lose money.

2. A portion of the company’s profits.

These payments, commonly referred to as ‘dividends’, are a portion of company profits distributed to shareholders twice a year. Companies are not required to pay dividends, but many do.

Those are the basics of investing in shares, and before we start looking at companies to invest in, let’s have a look at the risks and benefits of investing in shares.

Advantages of Investing in Shares

The latest ASX profile of investors provides an analysis of the 9 million Aussies who have money invested in shares. This includes next generation investors with an average age of 21 (median portfolio size of $50,000), female investors with an average age of 47 (median portfolio size of $90,000), and high profile investors with an average age of 55 (median portfolio size of $1,200,000).

Investors in all categories clearly see benefits in investing in shares. Here are six benefits of investing in shares in companies listed on the stock exchange.

- Ease of Trading

- Flexibility and More Control

- Capital Growth and High Rate of Return

- Passive Income

- Taxation

- Liquidity

1. Ease of Trading

Investing in the share of your choice is only a phone call or mouse click away, whether you choose a full service broker or do it yourself through an investment platform.

2. Flexibility and More Control

You can change your strategy easily because you are not locked in for a fixed term and will not incur any penalties for exiting, other than typical buy/sell costs. You can choose to invest as little or as much capital as you want in shares and spread that capital across sectors.

You could get as involved personally as you want or need in managing a share portfolio, depending on your skills and available time.

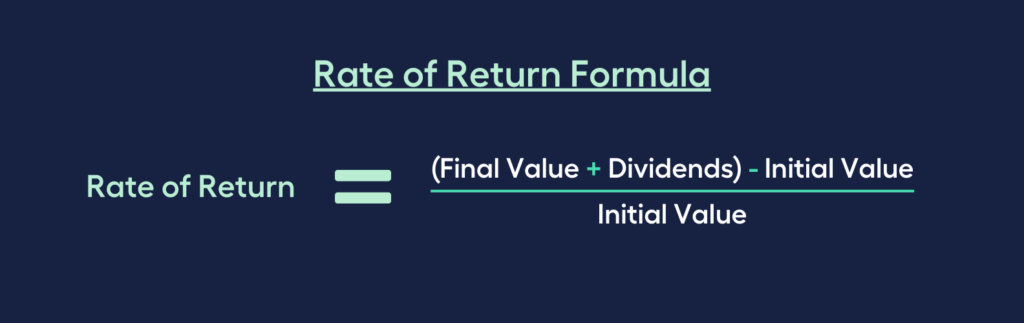

3. Capital Growth and High Rate of Return

Capital growth happens when the value of your investment rises. People buy shares because they have the potential for price appreciation. One method of achieving capital growth is by owning shares of a company with increasing share price.

As a long-term investment, it offers you a respectable rate of return when dividends are taken into consideration. A rate of return is calculated by deducting the initial value from the final value plus dividends, and dividing that figure by the initial value.

4. Passive Income

Some shares offer generous dividends, and they are frequently accompanied by tax credits to reduce or eliminate double taxation. This passive source of income can eventually be adequate to either supplement or even replace a regular salary.

5. Taxation

You may also benefit from the dividend tax credits, lower long-term capital gains tax rates, and legal tax planning by purchasing shares in the name of someone who makes less money than you.

6. Liquidity

The majority of shares are easy to trade. Shares are easily sold on short notice if you require cash for any reason.

Disadvantages of Investing in Shares

Before we wager our hard earned salary into the share market, it’s best to be aware of the risk-reward relationship prior to making investment decisions.

To receive a return on investment, you must be willing to put that money “at risk”. In general, the higher the risk associated with an investment, the higher the rate of return that investors will expect.

Do you see the benefits outweighing these five risks?

5 Risks of Investing in Shares

- Volatility

- Credit Risk and the Risk of Capital Loss

- Timing Risk

- Unexpected Events and Legislative Risks

- Lack of Knowledge

1. Volatility

Share prices can fluctuate significantly and even drop to zero.

Investors must realise that the value of their shares may change by as much as 50% or more in a year since share prices can rise and fall quickly.

A specific industry might be related to general market risk, for instance, mining shares are typically more volatile than industrial shares like bank shares. Individual share performance may be related to a specific risk.

2. Credit Risk and the Risk of Capital Loss

A share market investment is by no means a guaranteed one.

Finding a buyer for your shares at the price you want to sell them for might be challenging when a company isn’t doing well. As a result, the sale price of your shareholding may be significantly less than what you paid for it initially.

What happens if you own shares in a company that fails?

Shares of the company in which you own stock will no longer be tradable on the stock market if it goes out of business.

Shareholders are last on the list of other creditors (such as employees, banks, other lenders, and suppliers) to receive any money that may be realised in the case of an asset liquidation.

As a result, shareholders may only receive a portion of their initial investment or they may even risk losing everything they invested in the company’s shares.

3. Timing Risk

Due to market cycles, some shares are more risky when the general stock market has just gained substantial value and is about to retract. When the market has seen a sharp loss and then begins to rebound after displaying some signs of stabilisation, the converse may be true.

Not all market segments follow the same pricing cycles.

Timing risk can be managed by having a thorough understanding of business cycles within different industries, and studying how various organisations perform at different stages of the cycle.

4. Unexpected Events and Legislative Risks

Share prices can be significantly impacted by unanticipated, out-of-your-control events like unfavourable news about the company you have invested in, a change in government regulations, or a natural or man-made disaster.

A change in the legislation may have an impact on your investing plans or even individual investments.

5. Lack of Knowledge

Learning how to invest wisely takes patience. Not only that, it also takes time to research your investing options, time to decide what to invest in, and time to manage your money afterwards.

Naturally, as you acquire expertise and learn more about the elements affecting your investment, making judgments regarding investments becomes easier.

These are just a few of the dangers that come with investing in the stock market. It is essential to educate yourself on risk and how it affects your assets. Any investment you are thinking about should come with a clear understanding of the potential risks involved.

Generate Passive Income

The money you earn while not actively managing the investment is known as passive income.

Although you often need to wait until you’re close to retirement to access your superannuation balance, the increase of your superannuation balance provides passive income even though it might not be as liquid as cash.

Dividend earnings from your shares are also considered passive income.

A passive income guarantees greater financial freedom and frees you from the 9–5 grind allowing you to invest your time in other things.

What You Need to Consider Before Choosing Super or Shares

| Super vs Shares: Which one is for me? | |

| You’re more inclined to invest in Super if: You’re focused on building long term capital growth and don’t plan to use the money invested in the short term | You’re more inclined to invest in Shares if: You want access to your money before you retire |

| You want to reduce your income tax and you’re okay with a salary sacrifice arrangement | You want to have control over when to buy and sell the shares |

| You want a “deposit-and-forget” strategy instead of being a hands-on investor | You want to earn passive income regularly from dividends You have an appetite for risk |

Generally, you’re more inclined to invest in shares if you check most of these boxes:

- You want access to your money before you retire

- You want to have control over when to buy and sell the shares

- You want to earn passive income regularly from dividends

- You have an appetite for risk

And you’re more inclined to invest in a super fund if you check these boxes:

- You’re focused on building long term capital growth and don’t plan to use the money invested in the short term

- You want to reduce your income tax and you’re okay with a salary sacrifice arrangement

- You want a “deposit-and-forget” strategy instead of being a hands-on investor

However, before you dip into your bank account, there are a few more things to consider.

Contribution Limits and Investment Timeframe

Shares and super are influenced by economic conditions. As investments, their performance returns fluctuate depending on the economy.

Super is a long-term investment that can be highly diversified, making it well-positioned to weather market peaks and valleys. However, super has annual contribution limits whether you choose salary sacrifice ($27,500) or personal contribution ($110,000).

Regarding short- to medium-term share investments, the value of your shares may be significantly impacted by market conditions. Your investment will be better positioned to weather minor market hiccups if you intend to own your shares for the long term, say 7–10 years or more.

Potential for Diversification

A key method investors can use to reduce risk is diversification. Money invested in a Superannuation fund is often invested in a wider variety of assets, such as cash, shares, real estate, and government bonds, making it more diversified.

When investing in shares, you may still create a decently diverse portfolio by making sure your investments are spread throughout a variety of sectors, such as finance, technology, mining, and services.

Personal Risk Tolerance and Investing Experience

In general, the more risk you’re ready to accept, the bigger the potential return is.

The danger of investing in shares is extremely high, especially if you are new to the stock market.

With super, there may be less risk because the fund manages your money and determines how to invest it.

Unless you have a financial adviser on your side, you’ll have to manage the majority of your shares on your own, which can be difficult when you’re first starting out.

Many people may be unaware of this…but just like you, 41% of Aussies intend to get financial advice rather than going it alone, according to an Australian Securities and Investments Commission (ASIC) report.

Looking for the right solution to your money situation but not sure how to find the right finance expert for your unique situation?

Take a load off your mind and start living a richer life by booking a complimentary call with our team.

It’s that easy!

Need advice to secure your financial future? Contact our team today we can help!