How would you like to access money from your super fund tax-free before age 60?

It’s possible by splitting super contributions with your spouse (married or de facto). Yes! Contributions can be split with your spouse.

And tax-free early access to a super fund is just one benefit of superannuation contribution splitting. When splitting super contributions, couples can equalise their superannuation balances, maximise tax benefits, improve retirement income streams, mitigate risks, etc., etc.

Let’s take a deep dive into the advantages of splitting contributions and shed light on how it can help couples achieve their retirement goals.

Jump straight to…

What is super splitting?

Saving for retirement is a key aspect of financial planning, and in Australia, contribution splitting with a spouse is one approach that can help couples optimise their superannuation assets.

Super splitting, also known as spouse contribution splitting, is an Australian practice that allows couples to split and distribute their super contributions between each other’s super accounts.

It’s a strategy intended to assist couples in achieving a more equitable and balanced distribution of retirement savings, optimising tax benefits, and improving their overall retirement security. Splitting contributions are intended particularly for married or de facto couples.

Spouse Contribution Splitting: How Does It Work?

Spouse contribution sharing is based on the ideas of collaboration and equality. It’s meant for situations in which one partner gets to save a lot more for retirement than the other because of differences in income or contributions. The practice lets couples share their super contributions in a way that encourages equality, making sure that both partners benefit from their combined efforts.

Spouse contribution splitting is a way for a member of a super fund to move concessional payments from their own super account to the account of their spouse.

Why consider contribution splitting?

There are several reasons why you and your spouse could consider contributions splitting, especially if there’s an income difference or an age difference between spouses.

Income Difference

Let’s say your spouse spent a significant amount of time at home caring for the kids, and doesn’t have a lot of super. Transferring a portion of your super contribution to your spouse’s super fund may be a good way to increase your spouse’s super account balance.

By contribution splitting, you may balance the asset ledger and have two adequate retirement funds.

Age Difference

Contributions splitting in this scenario, entails the younger spouse transferring super contributions to the older partner.

Let’s say John’s 55 and retiring at 60, while his wife Jane is 45 years old. As the older partner, John gets access to his super after 5 years while the younger spouse will have access to hers in 15 years. By splitting contributions with John, Jane gets access to the money she split into her spouse’s super account after five years.

Super contributions can be split for various reasons. What it requires is for you to look at the broader situation strategically and think about what you want to do with your money.

We’ll discuss those further later on, but for now, we need to identify with whom you can split your super contribution.

Can I transfer super to my spouse?

To qualify for contribution splitting, a couple must meet certain criteria. To start, let’s look at the Australian Taxation Office’s (ATO) definition of a spouse first.

The definition of spouse includes a person (of either gender):

- you are legally married to

- you are in a relationship with (that is registered under the laws of your state or territory)

- who lives with you as a couple on a genuine domestic basis (known as a ‘de facto spouse’).

If you meet the definition of a spouse, you must also meet the following criteria:

- Both you and your spouse must have been Australian residents at the time the donations were made.

- The receiving spouse must be younger than 65 years old.

- The spouse making the contributions must not be of preservation age or have fulfilled a condition of release.

A condition of release means you have accessed your super account due to either of the following:

- reaching preservation age and retiring

- reaching preservation age and starting an income stream for the transition to retirement

- terminating employment at or after the age of 60

- being 65 years old (even if you haven’t retired)

- extreme financial hardship

- on compassionate grounds

- terminal illness

- temporary or permanent disability

- leaving Australia (for some Visa holders), or

- death

Your preservation age is determined by your birth year, as shown in the table below.

To recap, you can transfer super to your spouse if you meet the ATO definition of a spouse, your spouse is below age 65, and you haven’t reached your preservation age or haven’t accessed your super fund.

How much can you super split?

Before we discuss how much of your super can be split, we need to point out that not all types of super contributions can be transferred to your spouse’s account.

The two main types of contributions that can be split with your spouse are:

- untaxed splittable employer contributions, and

- taxed splittable contributions.

Untaxed splittable employer contributions

If you are a member of a public sector super scheme, the employer contributions made for you may be untaxed splittable employer contributions.

You can transfer to your spouse 100% of untaxed splittable employer contributions made for you in a financial year if the amount is less than the concessional contributions cap for that financial year.

For example, the concessional contributions cap for this financial year is $27,500. You can transfer any amount less than $27,500. Thus, if you’re a member of a public sector super scheme and your super contribution amounted to $26,000 for the financial year. You can transfer all of that to your spouse.

However, splitting contributions is not possible for many public sector plans. Before submitting this application, you should get advice on dividing untaxed contributions from your super fund.

Taxed splittable contributions

If you are a member of a private sector super scheme, you can direct your super fund to send up to 85% of your taxed splittable contributions for the financial year to your spouse.

Only taxable contributions are eligible for super contribution splitting. Taxable contributions, aka concessional contributions, are before-tax contributions made into your super. That is, these are not included in your income tax. Rather these are taxed in your super fund and are payable by the fund at a rate of 15%.

Concessional contributions can be a tax-effective strategy to increase your super contributions while lowering your taxable income, especially if your annual income exceeds $45,000 and your tax rate is 32.5% or higher.

The most common concessional contributions are:

- employer superannuation guarantee,

- salary sacrifice,

- personal deductible contributions.

An employer superannuation guarantee is paid in addition to salary and wages. The minimum amount is 11% of one’s income but your employer can pay more. This also includes the super guarantee charge—an adjustment when an employer fails to pay the correct super guarantee amount by the due date.

Salary sacrifice contributions are a type of superannuation contribution agreement in which an employee agrees to have a portion of his or her before-tax pay transferred into a superannuation fund. Salary sacrifice contributions are made before income tax is calculated, resulting in lesser taxable income and, as a result, lower income tax responsibility for the employee.

Personal deductible contributions, aka personal concessional contributions, are personal contributions made to a superannuation fund from after-tax earnings (non-concessional contributions). However, you can choose to claim a tax deduction for these contributions when filing your tax returns. Thus your after-tax contributions are effectively converted into concessional contributions.

You can apply to split up to 85% of the concessional contributions for that financial year OR the concessional contributions cap for that financial year for the maximum amount of taxed splittable contributions.

So how much super fund can you split?

The most you can apply for contribution splitting is the lesser of:

- 85% of your concessional contributions for that financial year, or

- the concessional contributions cap for that financial year.

![Concessional contributions caps]](https://lh5.googleusercontent.com/FK0LRAinYZEwbf0RAW-K9fLr1BEK_RKNm6I921BwSTATTFdHIVpc79CoOlaNaM8rGtLQb1SCHLavgxDAtSgmJNXQQK3m1Tf1XAU882Gx3m-wNWzUKtysTMJLdcl0FlTUYTHRxWzlD-eTwpq1CofiriU)

Why only up to 85% of your concessional contributions?

Remember, your super fund contribution is taxed at 15%. The ATO gets the 15% and you invest the 85% whichever way you want.

Let’s have an example.

In the 2020-2021 financial year, James received a $10,000 contribution from his employer into his super account. Deciding to share this with his spouse, who has a part-time job, James discusses the possibility with his super fund. They inform him that he can make the request after June 30, 2021.

Afterward, James completes the Superannuation Contributions Splitting Application and submits it to his fund in August 2021. He specifies that he wishes to split $7,000 of his employer contributions, which are eligible as taxed splittable contributions.

Upon review, his super fund deems the application valid as the $7,000 amount is less than:

- 85% of the $10,000 contributed by his employer, and

- James’s concessional contribution cap.

Consequently, in September 2021, his super fund transfers the requested $7,000 to his spouse’s account.

What happens if you exceed the concessional contributions cap?

Here’s an example to illustrate what happens.

In the financial year 2018-2019, Lisa had set up a salary sacrifice agreement, resulting in the following super contributions:

Upon the financial year’s conclusion, Lisa and her partner Mark consulted an investment advisor. The advisor recommended Lisa reduce her salary sacrifice to $15,000 to avoid exceeding the $25,000 concessional contributions cap for 2018-2019. Consequently, she faced the prospect of excess contributions.

A friend informed Lisa about contributions splitting, suggesting that sharing contributions with Mark might help mitigate the excess contributions made in 2018-2019.

Lisa then completes the Superannuation Contributions Splitting Application and submits it to her fund, aiming to allocate 85% of her 2018-2019 total contributions to Mark. However, Lisa’s fund clarifies:

- They cannot approve the application because she is not allowed to split $25,500 (85% of $30,000) with Mark, as the amount exceeds the $25,000 concessional contributions cap.

- They can consider a new application for a split of 83%. However, they are mandated by law to report that $30,000 was contributed on her behalf.

Lisa is advised to seek professional guidance concerning the excess contributions.

Lisa proceeds with the 83% split as recommended. Subsequently, she receives an excess concessional contributions determination for 2018-2019 from the ATO, based on her total concessional contributions of $30,000.

What super contributions cannot be split?

Any contributions that are not taxed splittable contributions or untaxed splittable contributions cannot be split with your spouse. Basically, you cannot split your contributions if these are after tax contributions.

Just so you don’t make the mistake of splitting contributions that cannot be split, the following contributions cannot be split according to the ATO:

- personal contributions that you can’t claim a deduction for

- contributions you make with a capital gains tax (CGT) cap election for small business

- contributions you make with a personal injury election

- spouse contributions to your super

- contributions made for you if you are under 18 years old (unless made by your employer)

- transfers from foreign funds

- other allocations from reserves

- rollover super benefits

- contributions that have already been split

- government co-contributions

- government low-income super tax offset contributions

- first home super saver scheme contributions

- downsizer contributions

- temporary resident contributions

- trustee contributions

- a super interest that is subject to a payment split (due to a relationship breakdown).

Super Splitting: Pros and Cons

Splitting super contributions is a strategy in Australia that allows couples to rebalance their retirement savings, potentially improving their financial security. This involves transferring one’s contributions to a spouse’s super fund, improving the receiving spouse’s super balance and creating a more equitable retirement foundation for the couple.

However, splitting super benefit contributions to improve the receiving spouse’s income upon retirement has both advantages and disadvantages that individuals should consider before incorporating it into their retirement planning.

Understanding the benefits and drawbacks of super splitting can help individuals make informed decisions that align with their unique financial circumstances and aspirations.

What are the benefits of super splitting?

The following is a list of important benefits associated with split super contributions.

Balanced Retirement Savings: Spouse contributions splitting allows you a more balanced distribution of retirement savings. This is particularly beneficial when there’s an income disparity or age difference between partners.

Tax Optimisation: Super contributions are generally taxed at a concessional rate of 15%, which is lower than most individuals’ marginal tax rates. By splitting contributions, you can take advantage of lower tax brackets, reducing their overall tax liability and potentially saving money.

Maximising Contribution Caps: Super contributions splitting can help maximise the use of concessional contribution caps. If one partner hasn’t utilised their full cap, splitting contributions from the other spouse’s super account can prevent unused cap amounts from going to waste.

Early Access to Funds: If one partner reaches their preservation age before the other, super contribution splitting can allow the couple to access some of their superannuation funds earlier. This can be particularly valuable for planning phased retirements or addressing unforeseen financial needs.

Investment Diversification: Splitting contributions can lead to a more diversified investment strategy, as the contributions are invested separately within each spouse’s account. This can help mitigate the risk of market fluctuations affecting the entire retirement savings.

Estate Planning Benefits: In the event of a spouse’s passing, the surviving partner can potentially benefit from a larger combined superannuation balance due to the contributions that were split and diversified. This can provide added financial security for the surviving partner and dependents.

Reducing Superannuation Imbalance: Uneven superannuation balances can lead to inequities in retirement income. Split contributions can help mitigate this imbalance, ensuring that both partners have a similar level of retirement savings and income.

Customised Retirement Planning: When you split your contributions, you can customise your retirement planning based on individual goals, needs, and circumstances. This personalised approach can result in a more comfortable retirement for both partners.

Collaborative Financial Management: Contribution splitting encourages open financial discussions and collaborative decision-making between partners. This can enhance financial transparency and promote effective retirement planning as a team.

Mitigating Tax Penalties: Splitting contributions can prevent exceeding contribution caps, which could otherwise result in additional tax penalties.

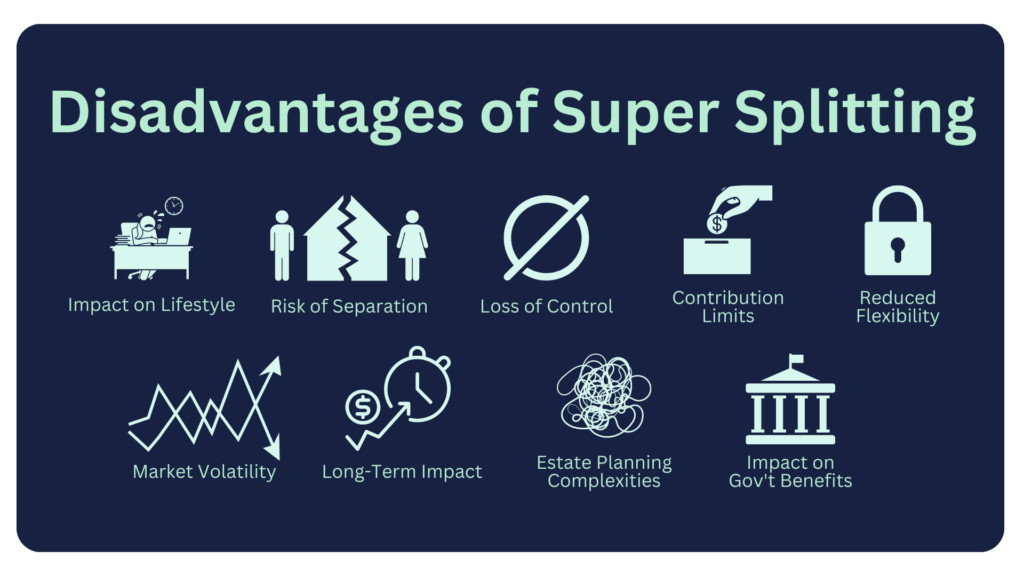

Are there any disadvantages to super splitting?

Here are some disadvantages when you split your contributions with your spouse:

Impact on Current Lifestyle: Contributions splitting involves redirecting a portion of one partner’s contributions to the spouse’s super account. This can impact the disposable income and lifestyle of the contributing partner in the short term.

Risk of Divorce or Separation: If a couple separates or divorces, contribution splitting arrangements might need to be adjusted or dissolved, potentially leading to administrative complexities and costs.

Loss of Control: Once contributions are split, the funds become part of the receiving spouse’s super account. This may result in a loss of control for the contributing partner over how the funds are invested and managed.

Contribution Limits: While splitting your super with your spouse can be beneficial for optimising contribution caps, it’s essential to monitor and manage contribution limits carefully to avoid exceeding caps, which could lead to additional tax liabilities.

Reduced Flexibility: The funds contributed through contribution splitting become subject to superannuation preservation rules, which means they cannot be accessed until certain conditions are met, such as reaching preservation age and retiring.

Market Volatility: Investments within super accounts are subject to market fluctuations. If one spouse’s super account performs significantly better than the other’s, contributions splitting might not lead to the intended balance adjustment.

Long-Term Impact: While contribution splitting aims to create balance, it might not be suitable for all couples’ long-term financial plans. Each partner’s financial needs and goals should be carefully considered before you split your contributions.

Estate Planning Complexities: In some cases, contribution splitting could create complexities in estate planning, particularly if there are changes in circumstances or beneficiaries.

Impact on Government Benefits: For those receiving government benefits or support, super splitting might affect eligibility or payment amounts. It’s important to consider these potential impacts.

It’s important to note that the advantages and disadvantages of super splitting can vary depending on individual circumstances, such as income levels, age, and financial goals.

Furthermore, super splitting involves navigating superannuation regulations and tax implications. Seeking professional advice from financial advisors or tax professionals is essential to ensure that the strategy aligns with a couple’s individual circumstances and goals.

Speak with a Money Guru Today About Your Superannuation and Get Your Money Sorted!