Once upon a time, in a charming Australian regional town, there lived a wise and forward-thinking man named David.

David had worked hard throughout his life and had amassed a considerable amount of wealth, including a beautiful beachfront property and successful investments. He wanted to ensure that his legacy would be protected and passed down to his family in the best possible way.

Curious about his options, David began exploring the concept of a family trust.

What is a Family Trust?

A family trust is a legal arrangement designed to protect family assets, such as property or investments, carry on the family business, and manage wealth for the benefit of family members.

Think of it like a treasure chest that holds valuable family assets. Instead of owning these assets directly, the assets can be placed in a trust and a trusted person, called a trustee, can be appointed to manage them on behalf of the beneficiaries.

Jump straight to…

Family Trust Jargon Simplified

1. Trust Deed

A legal document that outlines the terms and conditions for a family trust.

2. The Trustee

The person(s) responsible for managing the trust and its assets. They have broad powers to handle the trust’s affairs. Like other discretionary trusts, the trustees are also responsible for deciding how much each beneficiary will receive in capital and income distribution as stipulated in the trust deed.

In a family trust, the trustees are typically the parents. Trustees have important responsibilities under the law. They must follow the rules set by the state or territory that governs trusts, as well as other relevant laws, such as tax laws.

Here’s what trustees need to know:

Personal Liability

Trustees are personally responsible for any debts that the trust incurs. This means that if the trust cannot pay its debts, the trustees may have to use their own money or assets to cover those obligations. It’s important for trustees to be aware of this potential personal liability.

Indemnification (compensation or reimbursement)

On the flip side, trustees are also entitled to be reimbursed from the trust’s assets for any liabilities they incur while properly carrying out their duties. This means that if trustees act in the best interests of the trust and follow their legal obligations, they can be compensated from the trust’s funds for any costs or losses they may face.

Tax Responsibilities

Trustees are responsible for managing the trust’s tax matters. This includes registering the trust with the tax authorities, filing tax returns on behalf of the trust, and paying any applicable taxes owed by the trust. It’s the trustee’s duty to ensure that the trust meets its tax obligations in a timely and accurate manner.

3. The Settlor

The person who transfers trust assets to the trustee for the benefit of the trust’s beneficiaries, as specified in the family trust deed. After setting up the trust, the settlor usually has no further involvement.

Putting it all together…

The trust is created when the settlor (the person establishing the trust) and trustee(s) sign the family trust deed, and the settlor gives assets to the trustee.

A trust is an entity recognised by the Australian Taxation Office (ATO), but it needs a trustee to be legally established. The trustee is the person or entity responsible for holding valuable assets on behalf of other people, called beneficiaries. It’s a relationship of trust and responsibility where the trustee takes care of the assets held for the beneficiaries’ benefit.

Are all beneficiaries of a trust required to be from the same family?

While a family trust and discretionary trust are essentially the same, with the trustee having the power to distribute income as they see fit, it is more common for the beneficiaries to be members of the same family, usually children and dependants.

However, the term “family trust” is just a commonly used name, and it doesn’t mean that the beneficiaries must all come from the same family. You are not restricted from including individuals outside your family as beneficiaries.

But here’s an important point to consider:

If you include individuals outside your family as beneficiaries, you may not be able to make a family trust election for tax purposes. This means you might miss out on certain tax concessions and benefits that you would otherwise be eligible for with a family trust election.

Additionally, if you make distributions to individuals outside your family and have made a family trust election with the Australian Taxation Office, the trustee may be required to pay tax on those distributions at the highest marginal tax rate.

So, while there is no requirement that all beneficiaries must be from the same family, it’s important to understand the implications and potential limitations when including individuals outside your family in a family trust.

Seeking advice from a tax professional can help you make informed decisions and navigate the tax implications effectively.

Get matched with the right financial experts by booking a FREE 15 min Call or send us your questions today.

Now back to our story…

David was excited about the possibilities of having a family trust and pictured his children, Liam and Emma, growing up and leading successful lives of their own.

He could safeguard the family’s assets, such as the beachfront home and investments, with a family trust, against potential threats, such as business failures or legal issues.

David felt at ease knowing that his prized possessions and years of labour will be preserved for future generations.

What happens to assets in a family trust?

According to the provisions of the trust, the trustee oversees and administers these assets and distributes trust income or capital gains to the beneficiaries as necessary.

The unique feature of a family trust is its discretionary nature. This means that, like other discretionary trusts, the trustee has the freedom to choose who receives how much from the trust’s funds or assets. They can consider each beneficiary’s needs, circumstances, and tax implications when making these decisions. The trustee can distribute the trust income or assets to different family members at different times, depending on what is most beneficial for each person.

The assets are protected to some extent by this legal arrangement and separate legal entity since they are kept apart from individual ownership and out of the reach of creditors.

Learning that a family trust provides flexibility in how assets are distributed, David liked the idea that he could stipulate in the trust deed how Emma and Liam would receive the trust income or capital gains from the assets.

He could, for instance, make sure Emma has an income each month to support her artistic aspirations while allowing Liam to put earnings back into growing the family business. This flexibility would ensure that his children’s unique needs and aspirations were met.

What assets cannot be placed in a trust?

Even though a family trust might hold a variety of assets, there are some exceptions.

Typically, personal things like clothing, furniture, and everyday possessions are excluded. Family trusts are primarily used for managing financial assets, investments, and business interests.

Who owns the money in a family trust?

The assets under a family trust are legally owned by the trustee.

However, the trust’s beneficiaries have a beneficial interest, which gives them the right to receive capital or income distributions in accordance with the terms of the trust. As the assets’ custodian, the trustee makes sure they are utilised for the beneficiaries’ benefit.

Is a family trust protected in a divorce?

A significant benefit of a family trust is its potential protection in the case of a divorce. Because the assets kept in the trust are owned by the trust rather than individuals, they may be exempt from division during divorce proceedings.

Individual circumstances, applicable legislation and the court’s discretion, however, can all influence the outcome. It would be wise to consult with legal professionals to understand specific implications for the state that you live in.

David also learned that a family trust could be a shield during times of uncertainty, such as divorce. By having assets in the trust, he could protect them from being divided in case his children faced marital difficulties. This gave him reassurance that his wealth would remain within the family, safeguarding the legacy he had worked so hard to build.

Pros & Cons of Creating a Family Trust

To help you better understand how a family trust works and whether it could be a suitable option for you, let’s explore the pros and cons of a family trust.

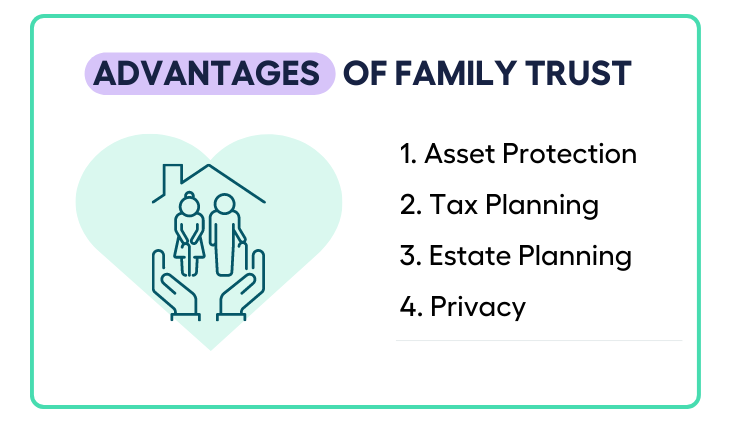

Advantages of a Family Trust

1. Asset Protection

A family trust can keep your assets safe. When you transfer ownership of your assets to the trust, they are held separately from you (including your personal assets, investment assets, and business assets), your family members, or the beneficiaries. This separation is crucial because it can potentially shield your assets from personal debts, lawsuits, or situations where you might go bankrupt. Even if you face financial difficulties, the assets within the trust remain secure and protected.

2. Tax Planning

Family trusts can offer tax planning opportunities.

How?

The trust doesn’t pay tax on income distributed to beneficiaries because distributions from a trust are treated as part of the beneficiary’s taxable income.

Therefore, the trustee can distribute income to multiple beneficiaries in proportions that make the best use of their personal tax rates. The beneficiaries then pay taxes on the income they receive. If the beneficiary has other income sources, all the income is taxed together.

For example:

If an adult beneficiary only receives income from the trust and their income is below the tax-free threshold, they may not have to pay tax on that income. If their income exceeds the threshold, they will be taxed at their personal tax rate.

Think about this:

Even if a beneficiary’s income exceeds the tax-free threshold, their tax rate may be lower because of the income already received from other sources.

There’s also a deterrent for trustees to keep trust income since undistributed trust income is taxed at the top marginal tax rate in the hands of the trustee. As a result, it serves as an incentive to distribute the trust’s income before the end of each financial year.

3. Estate Planning

A family trust is an essential part of estate planning because it allows you to manage your affairs while you are still alive. It’s a way of controlling (but not legally owning) assets during your lifetime as a mechanism to transfer assets to future generations. Trusts allow you to specify the conditions under which beneficiaries can access or utilise the assets, ensuring your wishes are carried out even after your passing.

Family Trusts and Your Will

The trust document specifies who will receive your assets, regardless of what your Will may state. In other words, the trust’s instructions regarding asset distribution take precedence over any conflicting provisions in your Will. This highlights the importance of ensuring that your trust is properly established and aligned with your intentions to ensure that your assets are distributed according to your wishes.

4. Privacy

Unlike Wills, family trusts are generally private documents, and that’s one of the reasons people choose to create them. They do not need to be made public after your passing, maintaining confidentiality regarding your financial arrangements and beneficiaries. This aspect can be valuable for those who prefer to keep their financial affairs private.

In Australia, the current approach in Trust Law is that beneficiaries don’t automatically have the right to access all trust documents. However, they can ask the court to step in and make a decision regarding the administration of the trust.

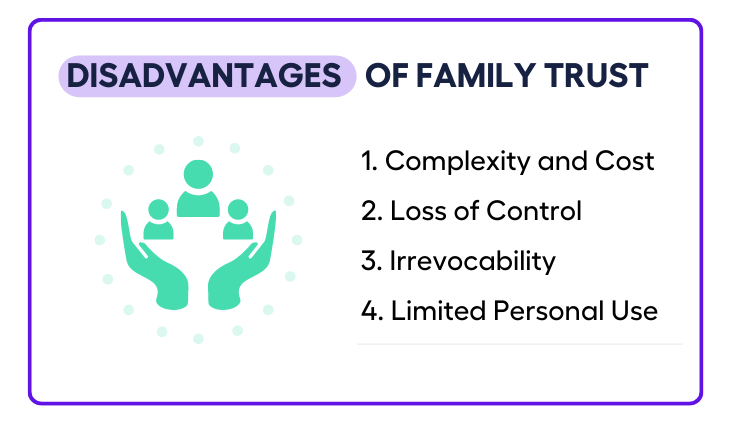

Disadvantages of a Family Trust

1. Complexity and Cost

A family trust can be difficult to set up and manage since it requires continual administrative (tax and accounting) work in addition to legal fees. The trust may need to be established and maintained with the help of professionals, such as lawyers and accountants, adding to the expense. Before moving on with a family trust, it’s crucial to compare these costs to the possible advantages.

2. Loss of Control

Control over the assets passes from the individual to the trustees chosen to run the trust when they are transferred to a family trust. Even while you can serve as the trustee, you might have to give up some of your authority over the assets. For those who wish to retain total control over their assets, this loss of direct control could be a drawback.

3. Irrevocability

A family trust is typically difficult to revoke or unwind once assets have been entrusted to it. The choice to create a family trust should be carefully thought out because it could have long-term effects. Before making any decision, it is crucial to fully understand the implications and seek competent counsel.

4. Limited Personal Use

Usually, the assets maintained in a family trust are there to benefit several family members or beneficiaries. This structure may limit access to assets or prohibit their usage for reasons other than those specified in the trust. Planning ahead is important, and it would be worth considering if the trust’s restrictions fit with your own financial objectives.

In conclusion, family trusts offer asset protection, tax planning opportunities, and estate planning benefits. However, they can be complex and costly to establish and maintain, and they require careful consideration due to the loss of control and the irrevocability involved.

By carefully evaluating the pros and cons, seeking professional advice, and assessing your specific financial situation, you can determine whether a family trust is the right choice for you and your family’s long-term financial goals.

You can decide whether a family trust is the best option for you and your family’s long-term financial goals by carefully weighing the advantages and disadvantages, getting professional advice, and analysing your particular financial circumstances.

Need help looking for Finance Experts who can help with your Estate Planning needs? Book a FREE 15 min Call or Send Us Your Questions!