You’re financially providing for your dependents now – but what about when you become terminally ill or pass away? Without your income, how would they cope with their financial needs?

Let me tell you how.

Death cover can give you peace of mind as it provides coverage for your family’s financial future even in your absence. This article provides all the information you need on death insurance cover.

What Is Death Insurance?

Death insurance, also called life cover, is a type of insurance that pays a lump sum amount of money to your beneficiaries after you pass away.

How Does It Work?

Death insurance financially protects your loved ones once you pass away. It helps relieve the financial burden for your family members suffering from the loss.

The death policy gives your beneficiaries a lump sum payment after your death and a partial payment if you are diagnosed with a terminal illness with less than 12 months to live.

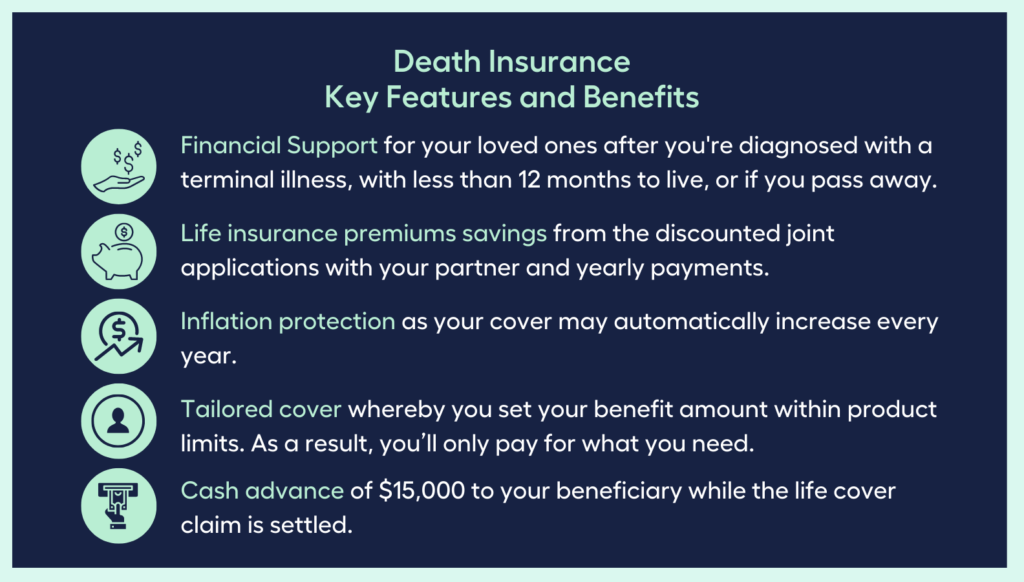

Key Features and Benefits

Here are the advantages of having death insurance:

- Financial support for your loved ones after you’re diagnosed with a terminal illness, with less than 12 months to live, or if you pass away.

- Life insurance premiums savings from the discounted joint applications with your partner and yearly payments.

- Inflation protection as your cover may automatically increase every year.

- Tailored cover whereby you set your benefit amount within product limits. As a result, you’ll only pay for what you need.

- Cash advance of $15,000 to your beneficiary while the life cover claim is settled.

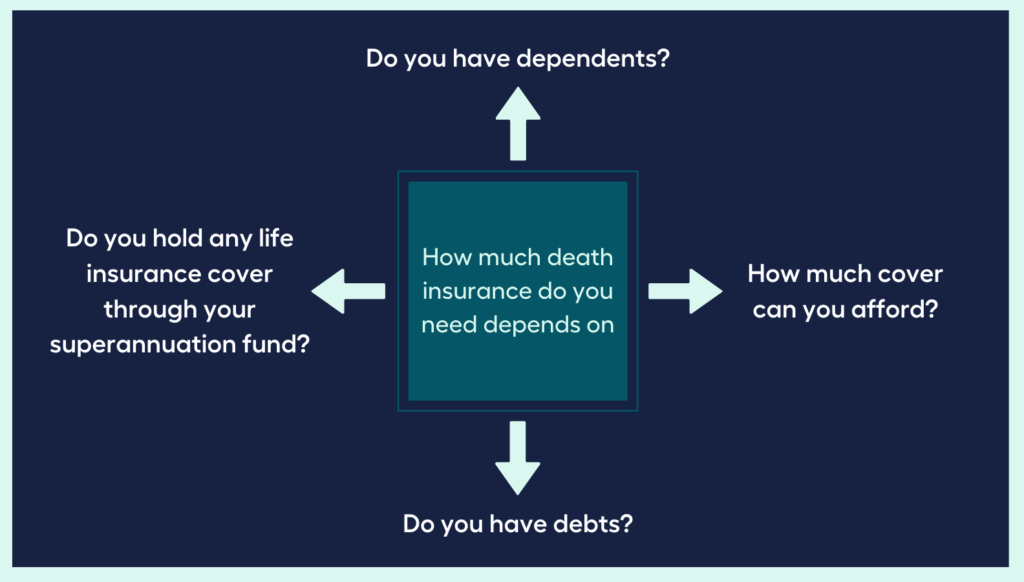

How Much Death Insurance Do I Need?

How much death or life insurance you need will depend on your individual circumstances. Some of the general considerations include:

- How much cover you can afford

- Whether or not you have dependents

- Whether or not you have debts such as mortgage or credit card

- If you hold any life insurance cover through your superannuation fund

Who Gets Your Insurance Benefit?

You can decide who gets your life insurance benefit by:

- Making a non-binding nomination – your insurer will consider your wishes when determining your benefit payout recipient

- Making a binding nomination to be highly certain

What Type of Expenses Am I Covered For?

If thinking about your family’s future financial security in your absence keeps you awake at night, you can have peace of mind knowing that a death policy cover gives you these:

- Rent or mortgage settlements

- Legal expenses

- Home maintenance costs

- Living expenses

- Children’s education fees

- Home maintenance costs

- Funeral expenses

- Estate settlement costs

What Forms of Death Cover Are Available?

There are two main types of death cover, namely:

- Term life insurance

- Funeral cover

1. Term Life Insurance

Term Life Insurance, also called term life cover, helps cover you and your loved ones in years to come. It can be changed to match your changing financial needs and obligations as you enter different life stages.

This policy is more flexible and detailed compared to the funeral cover. It offers a wide range of benefits and payout conditions to fit your financial needs.

2. Funeral Cover

With a funeral insurance policy, your beneficiary can take out a specific coverage amount for the funeral expenses, such as the administrative costs, mortuary fees, and the funeral itself.

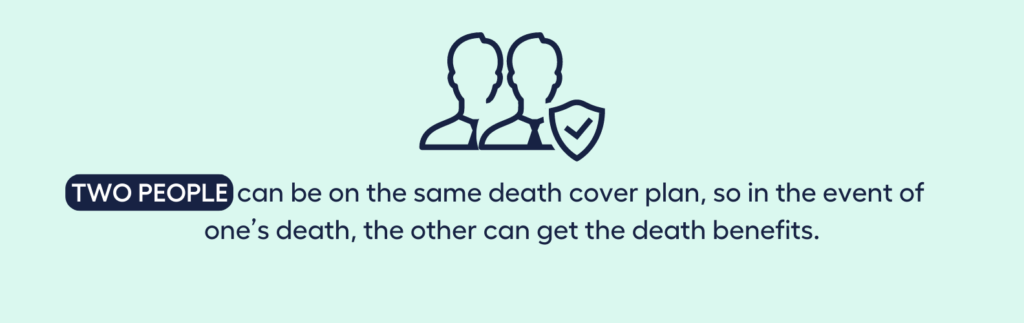

The funeral cover allows you to have two people on the same plan such that, if one passes away, the other can get the death benefits.

Not quite sure which Death Cover is the right one for you?

Check out all your insurance options with the help of an MMS Finance Expert!

I want to see all my options with the help of a Finance Expert

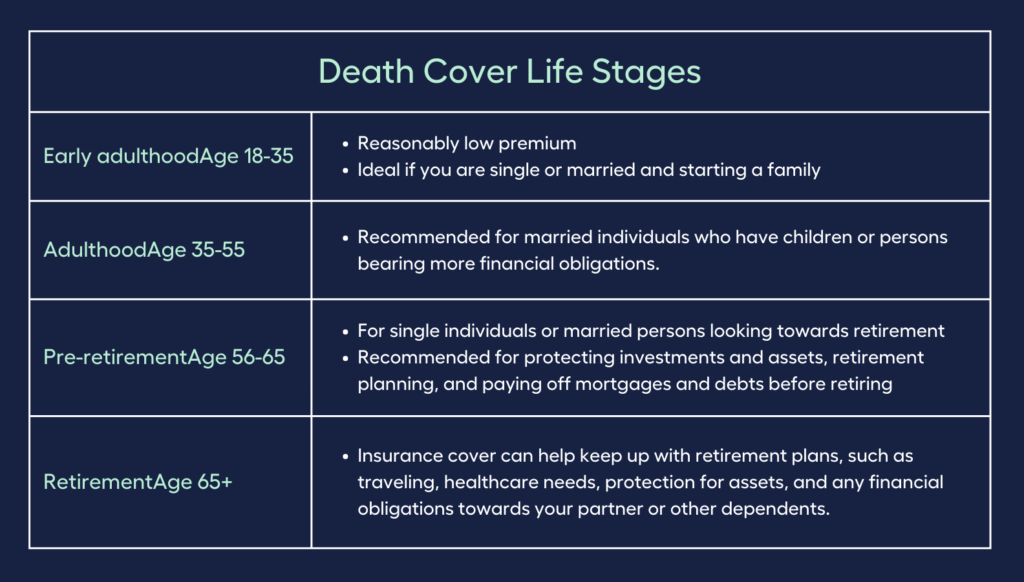

Book a FREE Call TodayDeath Cover for Different Life Stages

There are four different life stages that the death plan covers. They include:

- Early adulthood, age 18-35

- Adulthood, age 35-55

- Pre-retirement, age 55-65

- Retirement, age 65+

And for each life stage, a death plan offers different inclusions which addresses the needs of that age group.

Here are the available death plan cover for different life stages:

Can Death Cover Pay for Accidents and Injuries?

Yes. Accidental death insurance can cover both fatal and survivable accidents and injuries. However, only the term life plan can cover the latter.

Your Occupation Makes a Difference to Your Cover

To know what type of cover is right for you, let’s start with the three occupational classes:

- General

- Office

- Professional

Each category reflects the risk level related to the various roles and occupations. You can adjust your occupational category through an application. This will determine how much you pay for your cover.

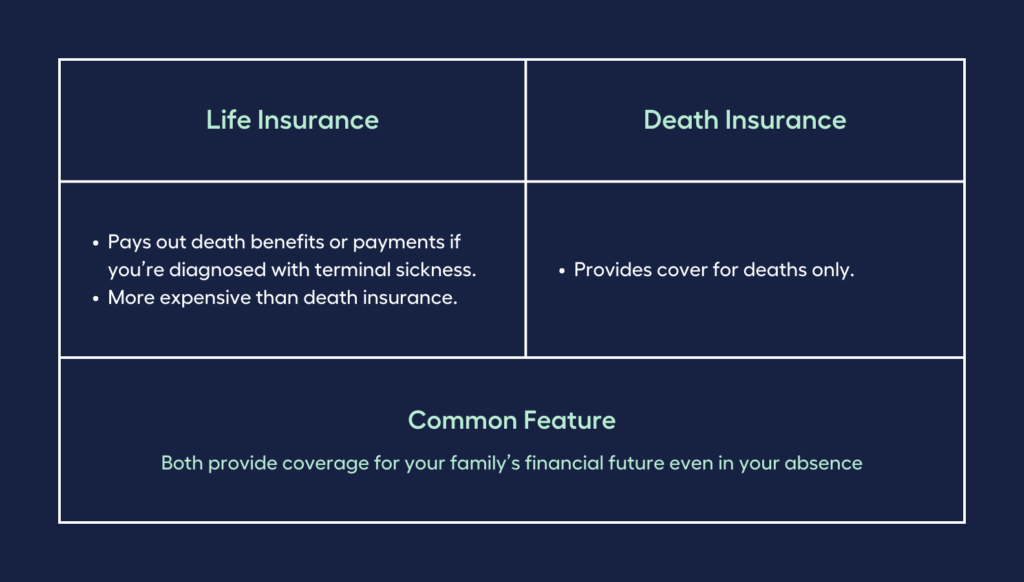

What Is the Difference Between Life Insurance and Death Insurance?

Insurance will always be your protection against a possible eventuality.

But between life insurance (term life cover) and death insurance, which one will most adequately cover your family’s future needs?

Let’s compare them.

A life insurance policy pays out death benefits or payments if you’re diagnosed with terminal sickness. Therefore, it is more expensive than death insurance which only provides cover for deaths.

How Much Does Death Insurance Cost?

You have to consider these factors that determine the cost of a death policy:

- Age

- Gender

- Occupation

- Medical history

- Health factors

- Income

- Employment arrangements

How Do I Apply For Death Policy?

[You have to fill out and complete an insurance application form to apply for a death plan. Also, make sure that the questions 1-10 in the ‘Personal Details’ sections do not apply to you. ]

You can have an idea of the coverage you require at a price you can afford if you know how the death insurance application process works.

Typically, the process entails:

- Filling out and completing an insurance application form

- Consenting to a paramedical examination

- Providing your and your immediate family members’ medical histories

These steps may be followed during the paramedical exam:

- Take your medical history (medical conditions, surgeries, prescription medications being taken)

- Enquire about your immediate family’s medical history

- Check your: blood pressure, heartbeat, height, and weight

- Draw a blood sample

- Get a urine sample

- Ask about lifestyle behaviours that can pose harm to your health (exercise routine, smoking, drinking, recreational drug use, frequent travel, high-risk hobbies such as skydiving)

- Additional tests, such as EKG, chest x-ray, or treadmill test, may be required depending on: your age, the type of policy you want, and the amount of coverage you’re applying for

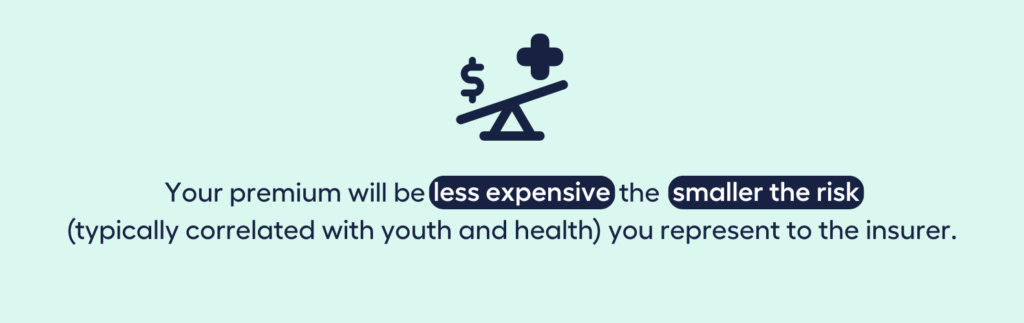

The insurance underwriter will then review your application and medical exam results to assess the financial risk you represent to the insurer that will determine your insurance coverage.

Take note that your premium will be less expensive the smaller the risk (typically correlated with youth and health) you represent to the insurer.

When Won’t A Benefit Be Paid?

A death benefit won’t be paid in the first 24 months of starting, restarting, or increasing your cover if you:

- Commit suicide

- Are disabled as a result of an intentional injury

Am I Eligible for This?

The death plan eligibility falls in the following categories:

- Age

- Gender

- Type of coverage

- Job type

- Arrangement with your employers

Make sure to go through the insurance guide in the relevant product disclosure statement for a detailed explanation.

In conclusion, everyone is different and everybody’s needs are unique. Obtaining advice from a financial adviser can help you make sense of your current financial situation and ensure you get the most appropriate death policy cover in place for your needs.

Now that you know the basics of death insurance, how confident are you that your family’s future financial security is covered if you were to pass away?

It’s not yet too late!

Still not sure where to start, or want help securing the right insurance faster?

That’s okay!

Many people may be unaware of this…but just like you, 41% of Aussies intend to get financial advice rather than going it alone, according to an Australian Securities and Investments Commission (ASIC) report.

You can reach out to My Money Sorted to guide you for free before you seek professional advice from an insurance expert!

When you book a call with My Money Sorted, you’ll:

✓ get a better understanding of your money matters

✓ have an idea of your money goals

✓ be matched with the right insurance expert who can help simplify your search for an insurance policy that fits your needs

My Money Sorted is your stress-free pathway to getting ahead with your money. Here’s what your journey will look like:

Step 1: Start off with a quick money matters session with My Money Sorted

Step 2: Get matched with a Insurance Expert that’s right for your money situation

Step 3: Take the first step towards getting the protection you need with a clear and sound roadmap prepared by an Insurance Expert

It’s that easy!