Unexpectedly experiencing major health issues could leave you riding a rollercoaster of emotions. With Critical Illness Insurance you can expect the unexpected in what could be an inescapable ride!

Why should I get critical illness cover?

Having a critical illness insurance policy can give you financial and mental freedom if you were to get really ill or hurt and need extensive medical treatment.

Read on and find out all the information you need on Critical Illness Insurance, its benefits, how much it could cost and other alternatives in the financial market to help you prepare for your future healthcare needs.

Jump straight to…

- Unexpectedly experiencing major health issues could leave you riding a rollercoaster of emotions. With Critical Illness Insurance you can expect the unexpected in what could be an inescapable ride!

- What is Underwriting

- Alternatives to Critical Illness Insurance

- What Happens To Critical Illness When You Turn 65

What is Critical Illness Insurance?

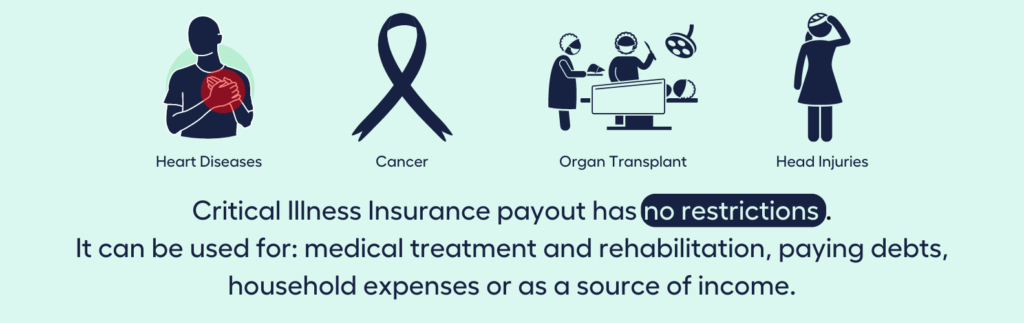

Critical Illness Insurance, also known as Trauma Insurance, is a policy that provides you with a lump sum benefit in the case of a serious health emergency. It may be possible to use this money to cover the best medical care possible, your rehabilitation, and a work schedule that allows you to concentrate on your recovery and health.

A trauma insurance policy covers these critical illnesses, injury conditions and medical emergencies:

- Terminal illnesses

- Coronary heart diseases

- Stroke

- Organ transplants

- Cancer

- Major head injuries

Benefits of Critical Illness Insurance

What kind of security do I get from a Critical Illness Insurance?

If you have a trauma insurance policy, in the event of a claim you won’t have to worry about covering the costs ofr extensive medical care and treatment associated with major medical crises.

These are common key features that you can benefit from:

- Financial support through a lump sum payment that you spend on whatever you need: living expenses, medical or rehabilitation costs, or for paying off debts.

- Broad eligibility: If you are an Australian citizen aged 16 to 55 (up to 65 for some insurers), you can apply for Critical Illness cover. Health, lifestyle and family medical history help determine your qualification for this insurance.

- Through Inflation proofing, your critical illness cover automatically increases coverage annually to stay ahead of inflation rates. Each policy anniversary, your policy cover amount increases by 5% or the change in the Consumer Price Index (CPI), whichever amount is greater, up until the policy anniversary after your 65th birthday.

- Long policy timeframes: Although each trauma insurance policy is unique, most are valid until age 70.

- The Insurance buy back allows you to reinstate the Life Cover Amount 12 months after full payment of Critical Illness claim. Some insurers allow this, and some allow this for life cover only. Some allow you to be covered for everything except the illness or condition that caused your original claim – i.e cancer. That would then be excluded from a future claim.

Are there other features of Critical Illness Insurance that I can benefit from?

To increase the benefits of your policy, these additional features can be added:

- Wider coverage range: Increasing your premiums broaden the range of covered conditions and may now include organ failure, HIV contracted through employment, intensive care or sensory loss.

- Death benefit: You may be awarded a benefit payout in case of death within 14 days of suffering a critical condition.

- Child support benefit: There is additional coverage available for your children if you have any.

What Is Covered

Critical illness insurance can pay for costs that traditional insurance does not cover. However, your policy may have different coverage limits.

If you are critically ill, your Trauma Insurance may help you to pay for these living expenses while you are recovering:

- Medical bills

- Household bills

- Credit card debt

- Mortgage payments

- Other general living costs like transportation, child care, food, tuition fees, etc.

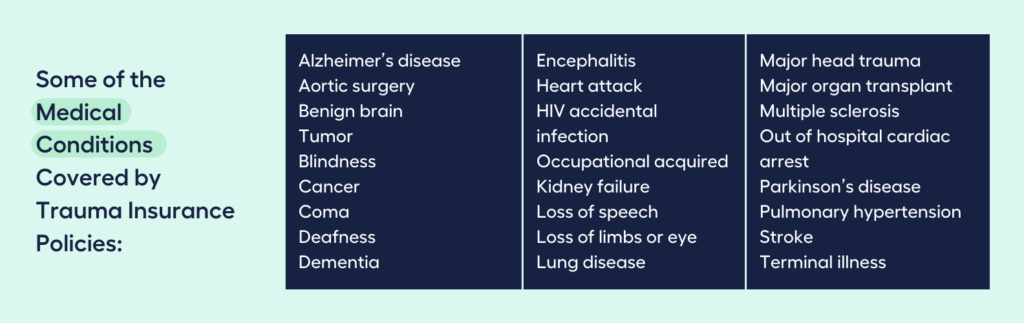

How do I know if my medical condition qualifies as a trauma event?

Trauma insurance policies generally cover more than 50 medical conditions. Below are some of the specific conditions covered.

This benefit is typically only paid out in the event that you get sick and are likely to recover. And because of this, many people decide to combine their critical illness and life insurance policies into a single policy.

Some of the main requirements for a payout include:

- You can receive full or partial payout if your diagnosed medical condition is listed in the product disclosure statement (PDS) of your policy.

- Your diagnosis occurs after 90 days from when you first purchased your policy.

- You survive the illness at least two (2) weeks from when you were diagnosed

What’s Not Covered

What circumstances won’t my critical illness insurance be liable for?

No Critical Illness Insurance benefits will be paid if:

- Your trauma event does not meet the requisite level of severity as cited in the product disclosure statement (PDS)

- Your serious event resulted from an intentional, self-inflicted act

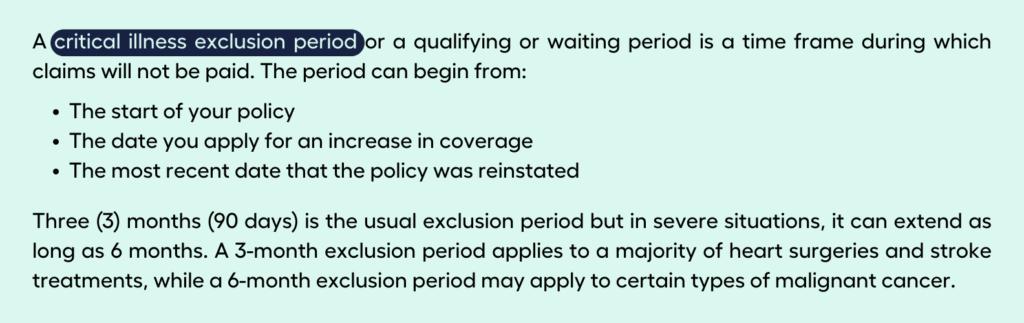

- Your condition or the symptom of your condition occurred during the first three (3) months from when the policy plan started, cover was increased, or cover was reinstated

- Your claim results from a special condition. If applicable, the special condition will be shown in the Policy Schedule.

Does Critical Illness Cover Have Any Waiting Periods?

When does my Critical Illness cover begin?

The “commencement date” is indicated on your Policy Schedule, and it is the day when your application is accepted. Your coverage starts on that day.

There are exclusion periods for some Critical Illnesses. Before any claim is paid, it is compared to a specified definition.

Payouts will not be made if your claim arises directly or indirectly before any one of the Critical Illness events cited occurred or was diagnosed, or the signs or symptoms leading to the diagnosis became apparent or would have become apparent to you:

- within three (3) months after the Plan start date;

- within three (3) months after the date of an approved applied-for increase, but only in respect of the increase portion; or

- within three (3) months after the most recent date that the policy was reinstated.

Is anyone eligible for cover?

Whilst the majority of people may be eligible for trauma insurance cover, there are some exceptions and exclusions that make it difficult for some individuals to obtain affordable coverage. A person with a pre-existing medical condition may not be eligible for coverage at all or may need to meet additional requirements.

You can apply for critical illness insurance if you’re between the ages of 16 and 65. Each insurer will determine your eligibility by asking certain questions. In addition to being asked about your health, way of life, and family’s medical history, you may or may not be required to submit to a medical examination.

Need help to assess your eligibility for critical insurance cover?

Check out all your insurance options with the help of an MMS Finance Expert!

I want to see all my options with the help of a Finance Expert

Book a FREE Call TodayWhat is Underwriting

How can I be sure that my insurance plan’s premiums and cover terms are appropriate for my medical situation, lifestyle and occupation?

Prior to issuing a policy, you will go through a process called underwriting which is a process of assessing insurance risk. Through this, your insurer can assess if insurance can be provided to you and on what terms.

Your qualification is evaluated through a series of questions about your occupation, medical history and the various activities you engage in. Underwriting is designed to ensure that premiums and cover terms for your insurance plan meet your needs and situation.

Who Needs Critical Illness Insurance?

Why Critical Illness Insurance May Be Important

Why should I consider Critical Illness Insurance as valuable?

You may be at the peak of health at the moment but even the healthiest people occasionally develop diseases that they have little possibility of preventing. And regardless of the life insured’s capacity for employment, benefits for critical illness are paid.

Hence, you are free to use the money any way you see fit, whether it be to pay off debt, get expert or alternative medical care, or transform your way of life (such as changing your work schedule while you undergo rehabilitation).

Individuals who are concerned about large out-of-pocket costs when medical emergencies arise may consider purchasing a Trauma Policy cover as a significant financial decision.

A major selling point of this type of insurance is being able to use the funds for a variety of purposes such as:

- to cover the cost of essential healthcare services that might not otherwise be offered

- to cover medical expenses that aren’t covered by a standard insurance

- to cover daily costs of living so the seriously ill can devote their time and energy on getting better rather than working to pay their bills

- transportation costs, such as those associated with going to and from treatment facilities, modifying automobiles to accommodate scooters or wheelchairs, and setting up lifts in homes for seriously ill patients who are no longer able to climb stairs

- Patients who are terminally ill or who simply require a peaceful environment to recover might utilise the money to go on a trip with friends or family

What Are the Pros and Cons of Critical Illness Insurance?

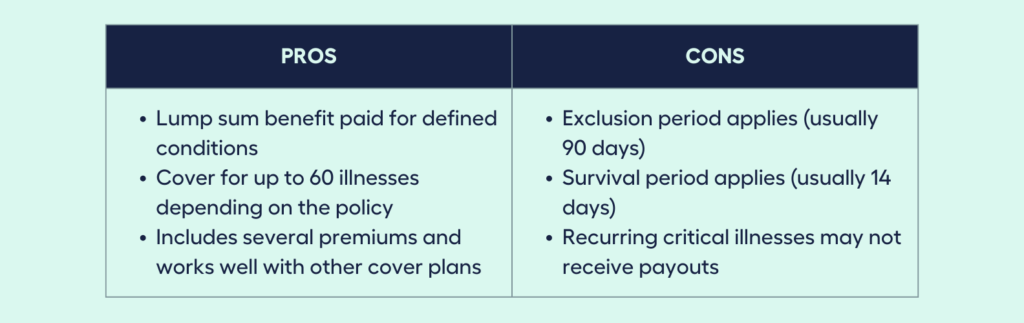

Pros of Critical Illness Insurance

A wide range of medical disorders are covered by this type of insurance. When you are diagnosed with a condition covered by the insurance, a lump sum of money is provided which you can utilise for any purpose, including non-medical costs such as home loan repayments, travel or vacation trips while you are in the recovery stage.

Critical Illness Insurance can include several premiums and may work well with other cover plans that you may already have. Comparing the premiums to those of a standard health insurance policy, they are low and inexpensive.

Cons of Critical Illness Insurance

Commonly excluded in Critical Illness Insurance are chronic illnesses and some types of cancer. Recurring critical illnesses, such as a second stroke or heart attack, may also not be compensated.

Furthermore, when the insured reaches a certain age, coverage may either be terminated or be scaled back.

And because certain critical illness policies have stringent restrictions, it is crucial to understand the specific conditions under which a policy covers a condition.Compared to other insurance types, there may be a waiting period before the benefits can be used, an exclusion, and higher rates.

These are the typical waiting periods: exclusion period (usually 90 days) and survival period (usually 14 days).

How Do I Buy Critical Illness Insurance?

Critical Illness Insurance is available as a standalone policy and as an additional benefit under a term life insurance policy.

You can purchase it on your own, through your workplace or employer, or as an addition to your personal life insurance policy.

How Much Does It Cost

Since each person is unique, your insurance should be as well. Based on the features of the policy, prices may vary. The cost of insurance depends on your age, gender, lifestyle, and medical history.

Some insurers allow you to tailor your cover amount and select the best suitable options for you. Should you decide to buy trauma insurance, seek financial advice from an appropriately qualified financial adviser before deciding on the appropriate coverage suitable for you.

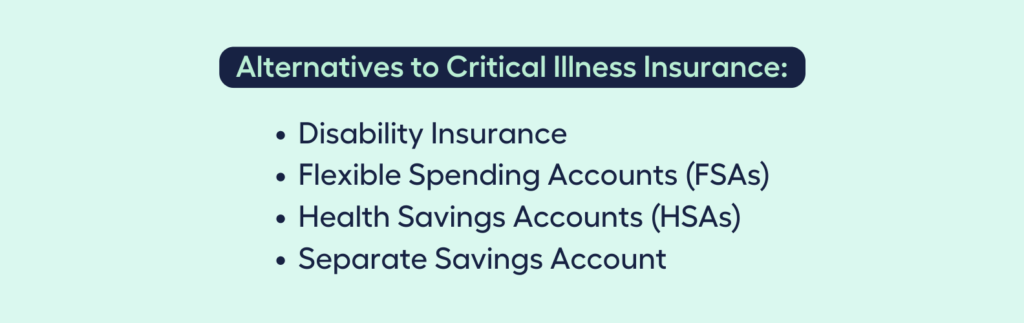

Alternatives to Critical Illness Insurance

What if I find Critical Illness Insurance too limiting?

There are other types of insurance that do not have strict limitations as pointed out by some insurance brokers.

Disability insurance, for instance, offers financial support when you are unable to work due to a medical condition, and it is not just for specific diseases. This is a particularly wise choice for somebody whose standard of living would suffer significantly from a prolonged absence from work.

If you have a high deductible health plan you can also invest in flexible spending accounts (FSAs) or health savings accounts (HSAs), both of which provide tax advantages when used for qualified costs.

Additionally, you can create a separate savings account to pay for non-medical expenses that might occur, say, if you were diagnosed with cancer and had to take time off work.

What Happens To Critical Illness When You Turn 65

If you fall ill and are unable to work, Critical Illness Insurance may help to reduce some of your financial anxiety. It offers some flexibility because you can choose how to use the funds received to meet a range of potential needs.

However, this kind of insurance coverage has drawbacks because when you reach a certain age, your coverage may either be terminated or scaled back.

Seniors need to be extra cautious while considering these policies. Some insurance policies may have payout restrictions that prevent people above a specific age (like 75) from receiving benefits, or they may include “age reduction schedules,” that lower your potential insurance payout as you age.

After reading all you need to know about critical illness insurance, are you leaning towards getting one or any of its alternatives?

Still not sure where to start, or want help securing the right insurance faster?

That’s okay!

Many people may be unaware of this…but just like you, 41% of Aussies intend to get financial advice rather than going it alone, according to an Australian Securities and Investments Commission (ASIC) report.

You can reach out to My Money Sorted to guide you for free before you seek professional advice from an insurance expert!

When you book a call with My Money Sorted, you’ll:

✓ get a better understanding of your money matters

✓ have an idea of your money goals

✓ be matched with the right insurance expert who can help simplify your search for an insurance policy that fits your needs

My Money Sorted is your stress-free pathway to getting ahead with your money. Here’s what your journey will look like:

Step 1: Start off with a quick money matters session with My Money Sorted

Step 2: Get matched with a Insurance Expert that’s right for your money situation

Step 3: Take the first step towards getting the protection you need with a clear and sound roadmap prepared by an Insurance Expert

It’s that easy!