Budgeting is more than just having a plan to save money.

It involves using money wisely.

Jump straight to…

As John Maxwell, one of the most popular leadership experts in the world once said:

This means having a plan to save money, where to spend your money, have enough flexibility, and stay focused on your money goals.

And this is why I’ll be sharing with you these practical budgeting tips for families that can help you save money like a boss.

Let’s get started!

Creating a Family Budget: Income, Expenses and Savings

So, what is the difference between a budget and a family budget?

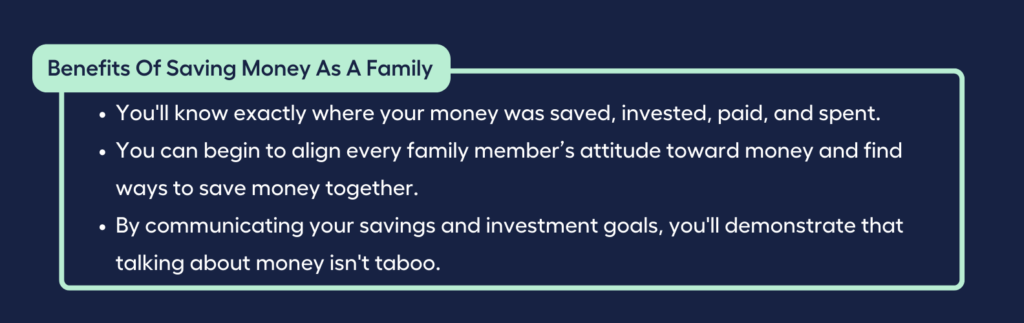

A great family budget involves everyone in the family.

The best thing about involving everyone in the family is that:

This is also important because a family budget involves the household income.

A household includes every family member who lives in the same home, including spouses and dependents.

And the household income is made up of the income of everyone in the household, even if just a portion of their income is used to support the family.

Get your family in on the plan and start saving money.

Ideal Income per Family Member

To get started, people would think that it’s best to earn more than the average earner in order to have a proper budget and save money.

That would mean you need to earn more than $91,000 annually to be categorized as an above-average income earner.

However, this study might come as a surprise for you:

This shows that a high income does not necessarily equate to a growing savings account and wealth accumulation.

More importantly, it means that anybody with a solid financial plan can save money and build wealth regardless of their financial situation.

You don’t have to wait for a pay rise and earn more money to start a budget and save money.

Know where you’re coming from by identifying the sources of your family income.

Keep track of when and how much money is coming in. If you don’t have a steady income, calculate an average amount.

Make a list of every dollar that comes in, including:

- the amount

- the source

- the frequency (weekly, fortnightly, monthly or yearly)

This money may come from your salary, government payments or benefits, or income from investments.

Make a List of Fixed and Family Expenses

Part of knowing where you’re coming from is to be aware of the family’s regular expenses.

Your regular expenses are your “needs”—the things you really must have to survive. These include fixed expenses and debt expenses.

| List of Regular Expenses | |

| Fixed Expenses include: Mortgage or rent payments telephone, gas, water bills, and electricity bills council fees home costs, such as grocery bills and food healthcare expenses and insurance transportation expenses, such as vehicle registration or bus fares family expenses, like baby products, daycare, tuition, and extracurricular activities | Debt Expenses include: personal loans repayments credit card debt payments mortgage repayments |

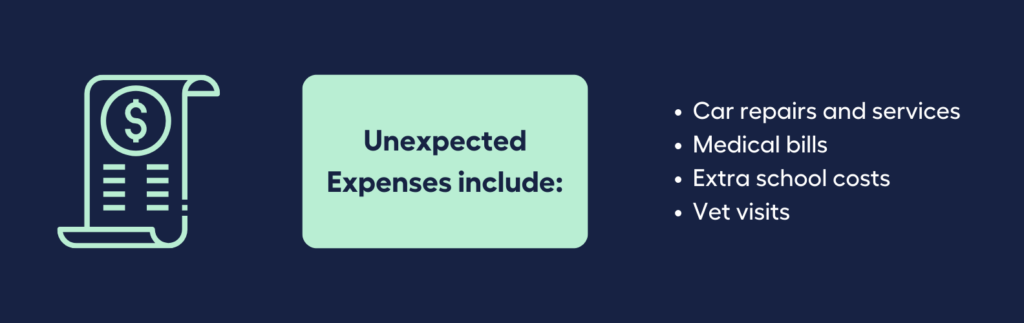

Prepare for Unexpected Expenses

When you’re on a family trip, you better be prepared for the unexpected.

The same is true for the family’s monthly budget. You don’t want to dip into your savings account when the unexpected comes up.

Include the unexpected in your monthly budget and have a separate bank account for savings and an emergency fund.

Spending Money or Saving Money – Make Room in Your Budget for Both

Your spending and saving money is the money that is left over after expenses.

Spending money is used on “wants” like entertainment, dining out, and hobbies.

Make a plan for how you wish to use your discretionary income. This will make it easier for you to track where the money goes and stay under your budget.

If you have a savings goal, you can use your budget to help you reach it.

When you are aware of how much money you have available for “wants,” you may determine how much of it you would like to save.

Regularly setting aside even a small sum can have a big impact over time.

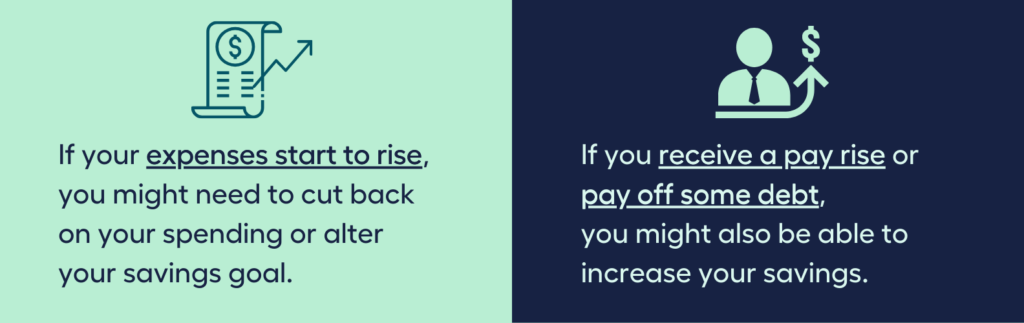

Adjust your budget as things change. Make your budget work for you and your lifestyle.

For instance:

Understand Your Spending Habits

Budgeting involves having an understanding of your present spending habits.

A habit is a persistent pattern of behavior that is regularly followed so that it nearly feels spontaneous.

You may not even be aware of your spending habit because it comes naturally and without conscious thought.

ASK yourself, do you:

- Always blow a lot of money right after receiving your pay

- Frequently spend money on things you use once and never use again

- Rarely shop around to find the best deal on big ticket items

Start by keeping track of your spending, whether you use a computer, an app, or pen and paper.

Then, based on your aims and goals, compare your existing spending to what is necessary.

A simple way of understanding your income and expenses is by using the My Money Sorted (MMS) Budget Planner calculator so you can have a better picture of your financial position.

Check how you can be the boss of your family budget using the MMS Budget Planner calculator today!

Make Clear and Realistic Savings Goals

If you’re going to handle your family budget like a boss, you better have SMART goals.

SMART is a management acronym that can help you set financial goals.

| Specific | Your savings goal must be specific, not general or ambiguous. Be specific about what you want to achieve and consider how this goal will improve your financial situation. If you don’t know what you want, you won’t get it. |

| Measurable | Make your financial goal quantifiable so you can track your progress and overall success. Express your savings goals in numbers so you know where you stand and when you’ve achieved them. |

| Achievable | Unrealistic expectations are one of the hardest obstacles to overcome. The best way to improve your financial situation is to take practical steps.If smaller steps are needed, that is acceptable. You may always start fresh with your savings goals! |

| Realistic | Consider your intended course of action while establishing your savings goals. Consider whether or not those actions are feasible in light of your existing situation. Setting impossible standards frequently results in disillusionment and giving up. |

| Time-based | Set a deadline for your family to achieve your savings goals. This will motivate you to finish what you start, stop putting things off, and hold yourself accountable. |

Example: Saving for a Home Deposit

In the coming years, you should start saving for a deposit if you intend to buy a home. Here’s how to make that dream into a SMART savings goal.

| Specific | Be as detailed as you can. You’re saving money for a deposit on a house. |

| Measurable | Determine the precise amount of your deposit. Aim for 20% of the price you anticipate paying for a property. For a $1 million house, your goal is to save a $20,000 deposit. |

| Achievable | $20,000 is a huge amount, you need to plan and set goals to achieve it. Such as putting aside about $556 every month if you wanted to purchase your home in three years time. |

| Realistic | Use a budget calculator to figure out how much you can put aside each month. Consider attainable alternatives to increase your income or reduce particular spending in your budget.If you find it impossible to save $20,000 in three years, think about extending your timeline or looking for a less expensive home. |

| Time-based | Choose a reasonable time frame for your goal based on the amount you need to save and your monthly savings goal. |

| Your S.M.A.R.T. savings goal is: I will save $20,000 in three years for a deposit on a family home. I will achieve this by putting $556 into a savings account monthly. |

Quick Saving Tips for Families

Tip #1:

Constantly remind yourself of your goals

- Constantly talk about your goals with the family. This way everybody has the family goal in their consciousness. And everybody will be on the lookout for money saving tips and ways to save money.

- Have a “Dream Board”. It’s a basic combination of images and text centered on your goals to remind you and the family of your financial goals.

- Maintain a weekly budget to keep track of your expenses.

Tip #2:

Separate accounts for spending, savings, and emergencies if you can

- Use an online savings account to grow your money faster because it’s harder to dip into your savings account unlike a transaction account.

- Automate your savings by setting up a direct debit from your the account your salary is paid into.

Tip #3:

Understand the power of compound interest

Knowing when to use compound interest will help you start saving money quicker.

- Open a high interest savings account.

A high interest savings account that charges no or few monthly fees is best. By saving money into this account, you take full advantage of compound interest.

The interest rates on a competitive savings account will be around 1% and higher. Interest rates on a transaction account will typically range from 0% to 0.5%.

- Settle your credit card bills immediately.

Compound interest works negatively with credit cards. The larger your balance grows, the more interest that will be added on top of the amount you owe.

Tip #4:

Minimize out of pocket expenses

- Use a debit card, credit card, or online payment so you keep track of your specific expenses through bank statements.

- Unless you diligently write down cash transactions and keep the receipts, you’ll lose track of your variable expenses.

Tip #5:

Find ways to reduce your bills

- Save money by cutting down on grocery shopping by planning ahead and making a shopping list and sticking to it. Buying household essentials in bulk, and buying fresh produce on specials will save you money too.

- Reduce your energy bills by heating or cooling a room in use, not the whole house. Have a laundry day and run the machine with a full load. Use energy efficient appliances and turn them off when not in use.

Tip #6:

Look for cheaper alternatives

- Instead of going to the gym, join a running group in the local area or try free online workout videos.

- Switch from paid to free streaming services if there’s one available.

- Pack a lunch for work or go on a picnic instead of always eating at a restaurant.

- Look into carpooling or ride a bike to work to save extra dollars.

- Consider holidays with no airfare involved.

Tip #7:

Shop around for better deals

- Compare premiums when it’s time to renew your car insurance and health insurance.

- Review your annual internet and phone usage. Check if you’re optimising the plans, if not, it might be better to look for a cheaper option or a different product provider to save money.

- Take advantage of special offers from online retailers.

Remember:

Creating a budget is like going on a road trip. You have one starting point and one destination, but there are many different roads to take.

Just like planning for a trip, you need a clear financial roadmap to guide your money decisions.

What if you could tap into the wisdom of an experienced financial adviser instead of taking the all too common ‘hit-and-hope’ approach?

Many people may be unaware of this…but just like you, 41% of Aussies intend to get financial advice rather than going it alone, according to an Australian Securities and Investments Commission (ASIC) report.

Find the right Finance Expert for you with the help of My Money Sorted.

When you book a call with My Money Sorted, you’ll:

✓ get a better understanding of your money matters

✓ have an idea of your money goals to help you save more

✓ be matched with the right finance expert who can help simplify your family’s journey to financial wellness

My Money Sorted is your stress-free pathway to getting ahead with your money.

Here’s what your journey will look like:

Step 1: Start off with a quick money matters session with My Money Sorted

Step 2: Get matched with a Finance Expert that’s right for your money situation

Step 3: Take the first step towards your money goals with a clear and sound roadmap prepared by a Finance Expert

It’s that easy!

Get Your Money Sorted with a Finance Expert by booking a call with My Money Sorted today!