Have you ever been turned down for a loan or a credit card?

Or perhaps you were approved, but with a high-interest rate that left you paying more than you bargained for?

If so, it could be because of your credit score.

Your credit score is an important number that reflects your reliability as a borrower and can impact your ability to get approved for credit, as well as the interest rates you receive.

But don’t worry, improving your credit score could be within your reach.

In this article, we’ll discuss what a credit score is, the factors that may contribute to your credit score, and most importantly, how you can improve it. By following these simple steps, you could be on your way to a better credit score and a healthier financial future.

Jump straight to…

Credit Score vs Credit History

Let’s start by understanding the difference between credit score and credit history.

Your credit history is a record of your past credit activities, such as loans, credit cards, and payments. Your credit score, on the other hand, is a number that reflects your creditworthiness based on your credit history.

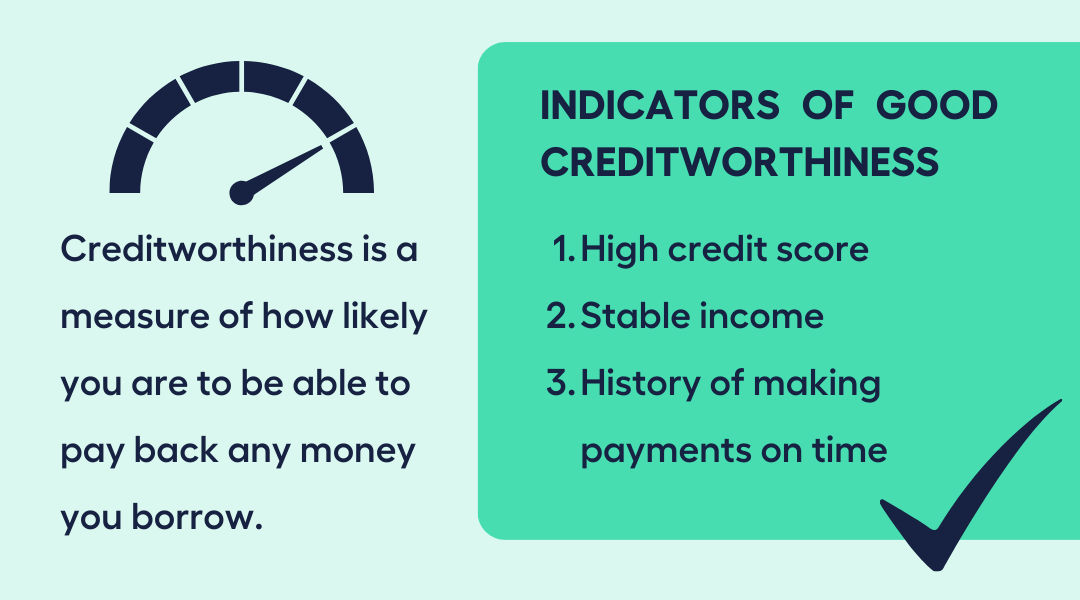

Creditworthiness is a term you may have heard thrown around when it comes to getting approved for loans or credit cards.

But what does it actually mean?

Creditworthiness

Put simply, creditworthiness is a measure of how likely you are to be able to pay back any money you borrow.

Lenders use this assessment to determine whether or not to approve your application for credit, and what interest rate to offer you.

Your creditworthiness is based on a number of factors, such as:

- your credit history,

- income,

- and current debts.

Lenders will also look at your employment history and other financial obligations to determine if you have the ability to make payments on time.

Having good creditworthiness is important if you want to access credit at a reasonable interest rate.

A high credit score, a stable income, and a history of making payments on time are all indicators of good creditworthiness.

In short, creditworthiness is a way for lenders to determine whether or not you’re a reliable borrower. By maintaining a good credit history and managing your finances responsibly, you can increase your creditworthiness and improve your chances of being approved for credit.

Credit Score

Your credit score is a number that shows how reliable you are with borrowing money.

It’s one of the things that lenders look at when deciding whether to give you a loan or not. The score usually goes from 0 to either 1,000 or 1,200.

Your credit score is a number that can go up or down depending on how you manage your credit.

- For example, if you borrow more money or change the way you pay back your debts, your credit score can change.

To work out your credit score, the lender will look at your financial history. So it’s really important to make sure your credit score is healthy.

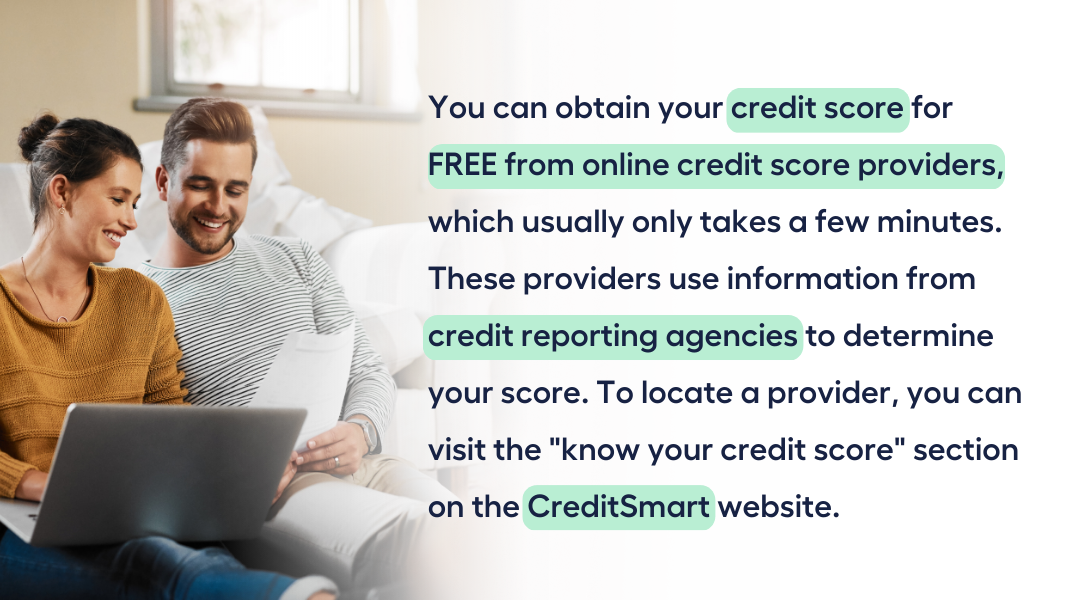

You can obtain your credit score for FREE from online credit score providers, which usually only takes a few minutes. These providers use information from credit reporting agencies to determine your score. To locate a provider, you can visit the “know your credit score” section on the CreditSmart website.

Do note that when you sign up for a provider, you typically need to agree to their privacy policy, which allows them to use your personal information for marketing purposes. However, you have the option to opt-out of this after you have signed up.

- Be cautious of any provider that asks for payment or your credit card information.

Credit Report

Speaking of credit reporting agencies, whenever you apply for credit or a loan, a credit report is created about you. You are entitled to receive a free copy of your credit report every 3 months and it’s recommended that you obtain a copy at least once a year.

Your credit report contains your credit rating which places your credit score in a specific category such as low, fair, good, very good or excellent. It’s like a behind-the-scenes look at how your credit score was calculated.

This score will give lenders an idea of how good you are with money and whether you’re likely to pay back your debts on time.

These details are included in your credit report:

1. Personal Information

Your personal information used for identification purposes, such as your name, gender, date of birth, driver’s licence number, employer, current and previous addresses.

2. Credit Rating

Your credit score’s category, such as low, fair, good, very good or excellent. Additionally, your credit score may also be included, although not all credit reporting agencies provide this information.

3. Credit Products

For every credit product that you have held within the last 24 months, you may be asked to provide the following details:

- Type of credit product (e.g. credit card, store card, home loan, personal loan, business loan)

- Credit provider

- Credit limit

- Dates when the account was opened and closed

- Name of any joint applicant, if applicable

4. Repayment History

For each credit product that you have held within the past 24 months, you may be asked to provide the following details:

- Repayment amount

- Due dates for payments

- Frequency of payments and whether or not you made them on time

- Any missed payments (i.e. payments not made within 14 days of the due date), and if and when they were made

5. Financial Hardship Information

If you’ve made a hardship arrangement with your bank or credit card company to make smaller payments because you’re having a tough time financially, that might show up on your credit report. But the only info it will have is how long the arrangement is for. If the arrangement is still going on, it’ll also show the month it started. After a year, the listing will be taken off your credit report.

However, if you’ve made a similar arrangement with a buy-now-pay-later company, phone company, internet company, or utility provider, that won’t show up on your credit report at all.

6. Defaults on utility bills, credit cards, and loans

If you don’t pay a debt to your service provider, like your phone or utility bill, they might report it to a credit agency. This is called a ‘default’ and it can stay on your credit report for up to five or seven years, depending on the situation.

But before they can do that, they have to let you know first. They can only report a default if you owe $150 or more, they’ve tried to contact you but couldn’t, and it’s been at least 60 days since the bill was due.

If you do end up with a default on your credit report, it’s not good news. But if you pay off the debt later, your report will show that you’ve paid it, even though the default will still be there.

7. Credit Applications

If you’ve applied for credit in the past, your credit report will show:

- How many times you’ve applied for credit

- The total amount of credit you’ve borrowed

- If you’ve ever co-signed or guaranteed a loan for someone else.

8. Bankruptcy and Debt Agreements

Have you filed for bankruptcy, entered into debt agreements or personal insolvency agreements, or been subject to court judgments under your name?

If so, your credit report will show this for at least 5 years.

9. Credit Report Requests

Any enquiries that credit providers have made about your credit report.

Typically, you can access your credit report online within one to two days. However, it’s also possible that you may have to wait up to 10 days to receive your report via email or mail.

To obtain your free credit report, you can contact

The 3 Credit Reporting Agencies in Australia:

1. Experian

2. Equifax

3. illion

These credit reporting agencies all use a different scoring system because they look at different factors when calculating your credit score, but the scores from all three tend to be similar in the end.

When you apply for a loan, credit card, or even a mobile phone plan, your lender will typically check your credit score and ask for a copy of your credit report.

- That’s why it’s a smart move to keep tabs on both your credit score and your credit report regularly.

Credit History

Credit history is a record of how you’ve managed credit and debt in the past. It shows how much credit you’ve had, how much you’ve used, and whether you’ve paid it back on time.

Your credit history includes information like your:

- credit accounts,

- payment history,

- and any outstanding debts.

It helps lenders and other financial institutions assess your creditworthiness and decide whether to lend you money or extend credit to you in the future.

A good credit history means that you’ve managed your credit and debt responsibly, while a bad credit history indicates that you may be a risky borrower.

What is a Good Credit Score?

A good credit score in Australia is between 540 and 661 or higher.

Depending on the credit reporting agency, credit scores can range from 0 to 1,200 or 0 to 1,000.

- A score of 661 or higher is considered good on a 1,200 scale, with scores above 853 being excellent.

- On a 1,000 scale, a score above 540 is considered good, while a score above 690 is excellent.

5 Ways to Improve Your Credit Score

If you’re looking to improve your credit score, there are a few simple and effective strategies that you can implement. By understanding the factors that impact your credit score and making smart choices when it comes to your finances, you may be able to boost your score and gain access to better credit options.

So let’s dive in and explore some of the top ways to improve your credit score!

1.Check Your Credit Report

Let’s tackle the most important thing first:

Check your credit report (and your credit score).

It’s important to know your credit score if you want to improve it, and then take a look at your credit report to see where you stand. If everything looks good, that’s great!

But if you spot any errors, it’s time to take action.

Here are a few examples of mistakes that could be dragging down your credit score:

- wrong personal info

- missed payments that you actually made

- debts you were never told about

- credit inquiries you didn’t authorise

To correct these errors, reach out to the credit agency that issued the report or the credit provider responsible for the mistake.

- Just make sure you have some ID and evidence to back up your claim.

Once the errors are fixed, your credit score could start to climb!

2. Automatic Debits to Pay Bills

Setting up automatic debits to pay your bills can be a game-changer for your credit score.

Here’s why:

Your payment history is one of the biggest factors that affects your score. Late payments can really hurt you!

But when you have automatic debits set up, you don’t have to worry about missing a payment or being late that could negatively impact your credit score.

Your bills will be paid on time every month without you having to do a thing. And that’s a great way to show lenders and credit agencies that you’re responsible with your money. Plus, you’ll avoid any pesky late fees or penalties.

It’s a win-win! So take a few minutes to set up automatic payments for your bills and watch your credit score start to climb.

Worried about overdrafts which occur when there’s not enough funds in your bank account to cover a transaction?

Setting up automatic debits to come out of your account the day after pay day is a smart move that can help you stay on top of your finances. By timing your payments this way, you’ll know exactly how much money you have left to work with after your bills are paid.

3. Sort Your Personal Finances: Reduce Debt

Reducing your debt by paying down high-interest debt or consolidating loans is another way to improve your credit score.

Keep in mind that your credit score is a reflection of your creditworthiness – in other words, how likely you are to pay back money you borrow. It shows lenders that you’re responsible with your credit and that you’re not overextending yourself.

When lenders see that you’re a good risk, they’re more likely to approve you for credit in the future, whether it’s a credit card, personal loan, or mortgage.

4. Don’t Close Old Accounts

Closing an old credit card account can harm your credit score by shortening your credit history.

- The length of your credit history is a factor that affects your credit score, and having a longer credit history can be seen as a positive thing. So, if you close an old account that you’ve had for a long time, it could lower your score.

Closing an account can also remove some of your positive payment history.

- Your payment history is a factor that affects your credit score, and having a history of making on-time payments is a positive thing. If you close an account that you’ve been making on-time payments on, it could remove some of that positive history from your credit report.

5. Limit How Often You Ask For Credit

Applying for credit too often can hurt your credit score. This is because when you want to borrow money or get a credit card, the lender will ask to see your credit report.

- It is called a hard inquiry and it can have a negative impact on your report.

That’s why it’s important to:

- Avoid applying for many different credit products at once

- Apply for only one credit product from one provider

- Double-check that you meet the eligibility requirements and that you’ve filled out the application correctly before submitting it.

Improving your credit score takes time and effort, but it’s worth it in the long run.

With a good credit score, you’ll have access to better credit options and lower interest rates.

Want more financial tips and insights? Subscribe to our Newsletter for more great ways to get your money sorted straight into your inbox.

Learn More About Your Financial Options – Book a FREE 15min Call or Send Us Your Questions!

I want to see all my options with the help of a Finance Expert

Call Our Team TodaySOURCES:

https://moneysmart.gov.au/managing-debt/credit-scores-and-credit-reports

https://www.creditsmart.org.au/know-your-credit-score/

https://www.creditcheck.illion.com.au/

https://www.experian.com.au/consumer/order-credit-report

https://moneysmart.gov.au/managing-debt/credit-repair#improve

https://www.equifax.com.au/personal/products/credit-and-identity-products

https://moneysmart.gov.au/banking/direct-debits

finder.com.au/good-credit-score

finder.com.au/improve-your-credit-score#2